(B)(N) Heard On The Street

Shanghai

Drama. China is encouraging investors to “take more risk” and invest in the equity markets, most typically in the Shanghai Stock Exchange in one of the largest (by population) and busiest, and most strategically placed, cities in the world (Bloomberg, September 3, 2014, China’s State Media Join Brokerages Saying Buy Equities); please see also our recent Post on a similar initiative to “take more risk” in Japan “(P&I) The Tanaka Index“.

However, in our well-known view – which is not popular on Wall Street – there is no “risk” in the equity markets – only volatility and uncertainty – most of which is brought to the market by the investors themselves, and inflicted on each other, because they don’t know what they want.

What are you doing to protect our capital?

But the word “guaranteed” does not just roll-off the lips of investment advisers anywhere – we need to ask for it – and if we don’t get it, then we need to do it ourselves – 100% capital safety, 100% liquidity, and a hopeful but not necessarily guaranteed return above the rate of inflation – those are the words that move us.

Moreover, these markets are actively seeking foreign investment, but we can’t go there if all that we’re offered is ETFs and mutual funds – which have less assurance than unsecured debt and promissory notes – and there is a shroud of secrecy in balance sheets and prices, so that we don’t know anything more than what we’re told, and absent the word guarantee, we can be certain that their goals are not the same as ours (Reuters, August 31, 2014, Passive funds an active threat for Europe’s fund managers).

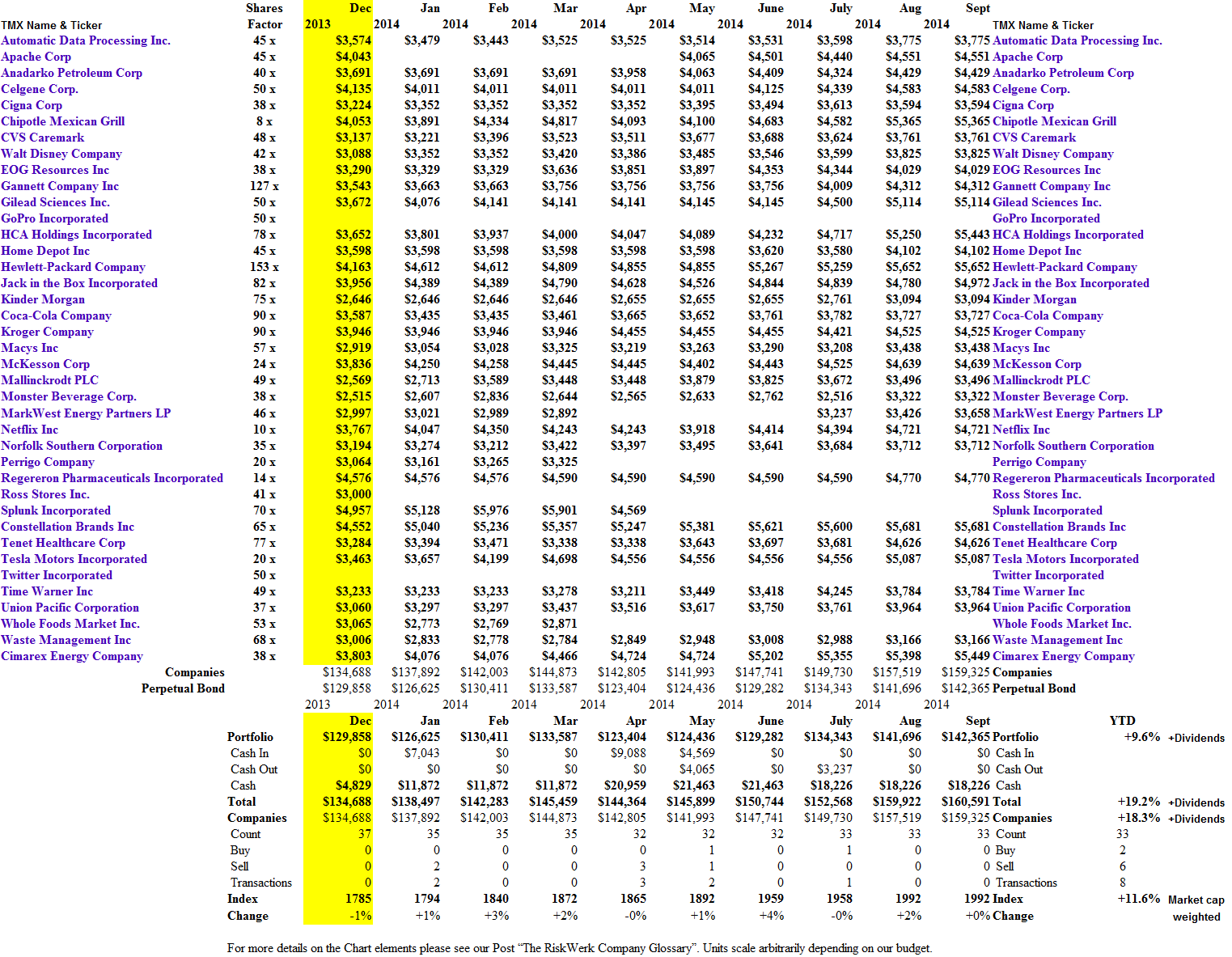

In contrast, Mr. Cramer of The Street has put-up a portfolio of thirty-nine stocks (The Street, September 2, 2014, Cramer: What’s Working, What’s Not) that might help investors to finish out the year – and it is a year of global crises and uncertainty in so many places.

The portfolio is a cross-section of All-American companies in a variety of timely industries (ibid, The Street), with full disclosure, but we should not forget that the market is a democratic system, too, and we won’t know who is going to get into the office in December until the money is counted; please see Exhibit 1 below for the Fundamentals.

Exhibit 1: (B)(N) Heard On The Street – Fundamentals – September 2014

(B)(N) Heard On The Street – Fundamentals

Figure 1.1: (B)(N) Heard On The Street – Risk Price Chart

This portfolio has some history and it was up +42.3% last year, and it is up another +17.6% this year, on a market-value basis; these companies also earned $63.8 billion (net) and returned 35.2% of those earnings to the shareholders for a dividend payout of $22.4 billion and an aggregate dividend yield of 1.3%; please see Exhibit 1 above for further details.

If we had bought the portfolio in January on an equal-weighted by market value basis, we’d be up +18.3% so far this year, and if we had run it as a Perpetual Bond™, we’d be up another +1% to +19.2% so far this year; please click on the links “(B)(N) Heard On The Street – Prices & Portfolio and Cash Flow Summary” for further details.

There is no safety in the “numbers”.

But, in any case, the stop/loss is important – essential, we would say – and we always have in-place sell prices below the current stock price and above the price of risk for the (B)-class companies, which are the only ones that we will buy and hold until the “market” sells us out.

In other words, we don’t take any risks, and we don’t have to find buyers for our properties – houses, apartments, retail stores, et cetera – and we don’t have maintenance costs or rental headaches, and we don’t get the bond yield (2%) or the margin call. Investors who use leverage, however, whether on properties (mortgages) or stocks, with no sense or control of the downside, are just gambling, for which casinos and lottery-tickets will cost a lot less.

We also divided the portfolio into the dividend-paying and non-dividend-paying stocks and, indeed, the return on the shareholders equity is 9.8% in the dividend-paying stocks, and 32.5% in the non-dividend-paying stocks – the so-called “growth class” in which investors can only make money if they sell their stocks to other investors – the “newbies”; please see Exhibit 1 above.

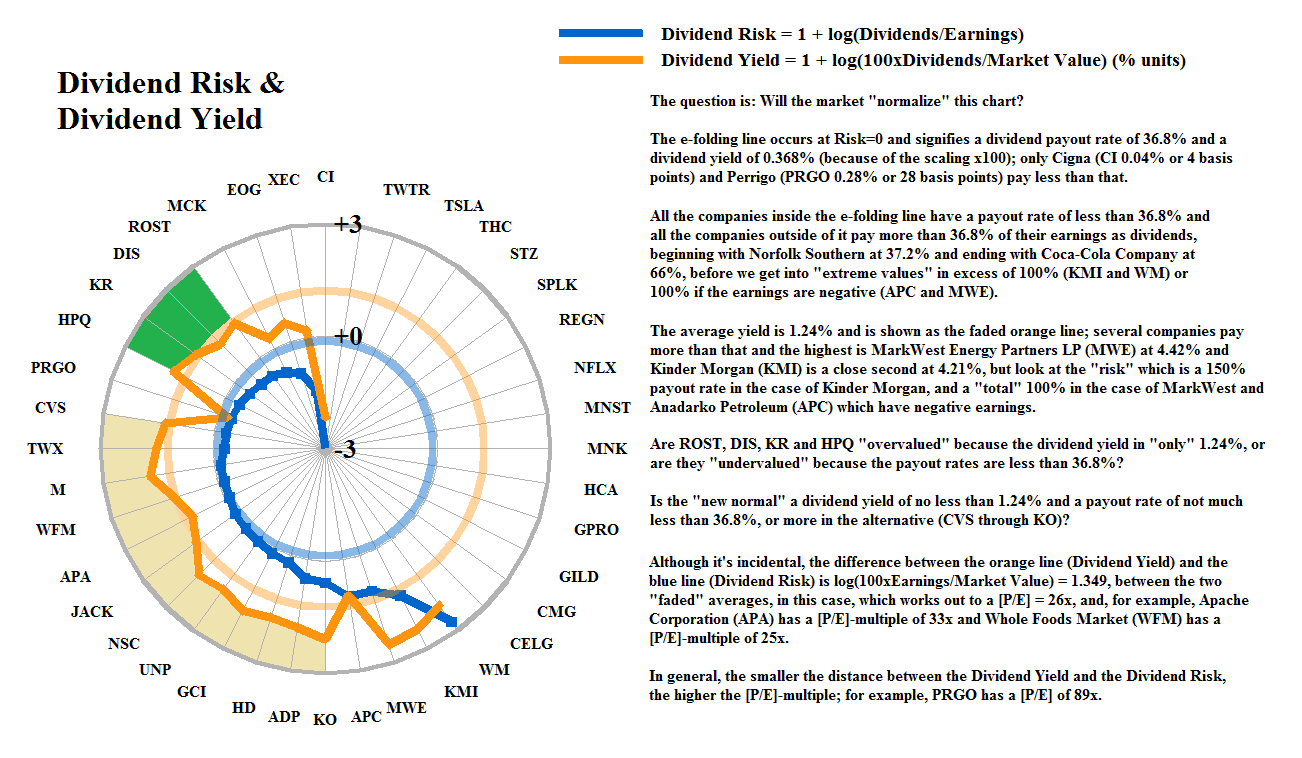

Other salient facts are that investors are willing to pay $23 for $1 of the Coase Dividend in the dividend-paying stocks, but 4× as much ($101) for $1 of the Coase Dividend in the non-dividend-paying stocks, reflecting their more speculative nature; their inventory productivity (+1.17) is also much higher, but their fixed assets productivity (-0.70) is only half that of the dividend-paying stocks (-1.51), reflecting a substantially under-utilized production capacity in the dividend-paying companies; for more information on these concepts, please see our recent Post “(B)(N) Through The Looking-Glass“.

Figure 1.2: Dividend Risk & Dividend Yield

To get some insight into what might happen in the next three months, we co-related the “dividend risk” to the “dividend yield”; please see Figure 1.2 on the left.

We ask the questions (please see the chart, and click on it to make it larger as required), but we don’t have any answers because “investors” will have the vote, and they will vote with their money during the next several months.

Travel much?

The best that we can do, as investors and risk managers, is to manage our “risk” – the real risk – safe, liquid, and hopeful – so that no matter how they vote, we won’t have to leave the country.

For more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}