(P&I) Extreme Economics – Linear Growth

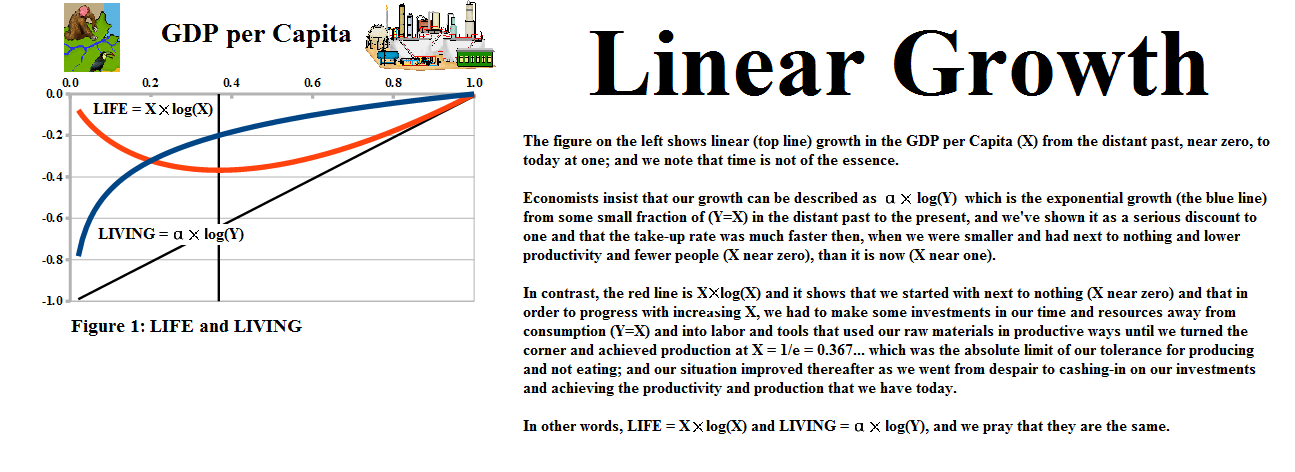

Figure 1: Life and Living

Essay. We should not expect exponential growth in the GDP per capita – that’s impossible even though it’s the standard model for economists and for politicians who want to point their finger and lay the blame on the current government for not achieving it (The Huffington Post Canada, January 29, 2016, Canadian Economy Expands In November, But Half Of Industries Have Shrunk In Past Year).

For example, if Y is the GDP per capita and we expect an exponential growth in Y, year after year, or even quarter after quarter, and time is marked by X, then that equation would look something like α×log(Y) = X where α>0 is some positive number (a large one at this scale) and X plays the role of consumption somehow improving over time with the growth of the GDP per capita and we all get to eat this Y.

However, a more accurate (read correct) linear growth model that we might consider is α×log(Y) = X×log(X) which slows down the worth or importance of “time” quite considerably, but doesn’t banish it either because we expect that things, namely Y (living) and X (life and living it up in time or due course), will get better as time goes by; please see Figure 1 above for an explanation of exactly how that works.

And we didn’t pluck this conjecture out of the air (Bloomberg, January 19, 2016, Economics Might Be Very Wrong About Growth) because the ECB economists and several Nobel Laureates are saying exactly that – we don’t know anything much about growth and least of all, do our policy makers who are much more concerned with personal growth.

But we’ve already worked this out in the Theory of the Firm (Goetze 2006) in which economic enterprise is described by the sets of payables (a) and the receivables (b) that we create in process (The Process) and their likelihood, a=p(a) and b=p(b), in the context of a balance sheet – we don’t get anything for free and we have to work for a living – as the E-conditions:

(E1) α×log a = b×log(b) and (E2) α×log b = a×log(a) (*)

(E1) α×log a = b×log(b) and (E2) α×log b = a×log(a) (*)

and it turns-out that the inter-temporal constant, α>0, is exactly the entropy of the process that is described by working-out our payables and receivables into cash (food, so to speak) over time.

Note: Despite the notation, the sets (a) and (b) are never the same across both equations except at the end of process when a=p(a)=1 and b=p(b)=1.

For more information on these concepts and their applications please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

For more information on the current Canadian market, please see our Posts “(B)(N) Extreme Economics – A Stock Chart, a Ruler, and a Good Eye” and “(B)(N) Extreme Economics – Plan Zero (Buy Canadian)“.

And for more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.