(P&I) The World’s Biggest Pension Plan

![]() Essay. Japan’s Government Pension Investment Fund (GPIF) is the world’s biggest pension plan with assets of $1.2 trillion under its management.

Essay. Japan’s Government Pension Investment Fund (GPIF) is the world’s biggest pension plan with assets of $1.2 trillion under its management.

But it’s not alone in “big” numbers – “big” depends on what we need it for – because there is also the world’s biggest sovereign wealth plan, Norges Bank Investment Management (NBIM), which owns about 1.3% of the world’s stocks, mostly in Europe, and is, apparently, “struggling to meet a real return target of 4%”, even though it has about four hundred employees who are working on the problem (Bloomberg, July 30, 2014, Norway Says $890 Billion Fund Likely to Follow EU Sanctions).

In contrast, GPIF has only about one hundred employees, and only seven of those are said to be “investment professionals” which, to us, means only “one” thing – safe, liquid, and hopeful – and, in any case, the final decision on investments is reserved for GPIF President Takahiro Mitani, and the health ministry, and the fund is barred from buying stocks directly (BusinessWeek, August 5, 2104, GPIF Needs Overhaul Before Asset Changes, Shiozaki Says).

Figure 1: GPIF Returns & Assets

In aggregate, since 2001, the fund has earned about ¥35 trillion on assets (on average) of about ¥100 trillion, which is about 2.2% per year; please see Figure 1 on the right.

However, the fund is going through a phase of investment angst (ibid, BusinessWeek) and, with changes in governance, might have to engage in “risky behavior” for which there are plenty of examples.

For example, NBIM above, but in the “minor leagues”, the California Public Employees’ Retirement System (CalPers) which has just $300 billion in assets (although it’s still the “biggest” in its class), and it has had some problems in the past with avant garde “risky behavior” for which it is a pioneer (P&I, August 4, 2014, Poor returns forcing CalPERS to cut cord on health-care fund and The Wall Street Journal, July 23, 2014, Calpers Pulls Back From Hedge Funds) and returned just 1% in 2012, and “lost” nearly $100 billion in 2008-2009 (Forbes, July 16, 2012, CALPERS Returns 1% For Fiscal Year) but is set to “return” 18% this year (Bloomberg, July 14, 2014, Calpers Earned 18% as Stocks Buoy Returns).

Figure 2: The Funded CalPERS

However, it’s not encouraging (to us), nor even plausible, that these funds are, somehow, magically, going to be actuarially “good” for the next fifty or seventy-five years if they’re not good now – after twenty years – and can’t explain what their least real return will be this year; please see Figure 2 on the right.

Moreover, these plans, and many more like them – if not all of them – are “The World’s Biggest Investors” – they are the market – and need to be “active investors” if they’re, somehow, going to “beat the market”.

But they are the market – mutual funds, hedge funds, “activist investors”, and so forth, are disparate and trivial in this context – so, their policy of “beggar thy neighbor” has to be one that comes around, and goes around, and they are all hanging on the cliff, now, for what “comes around” in the next three months, six months, a year, or two years, or so it seems. We don’t know.

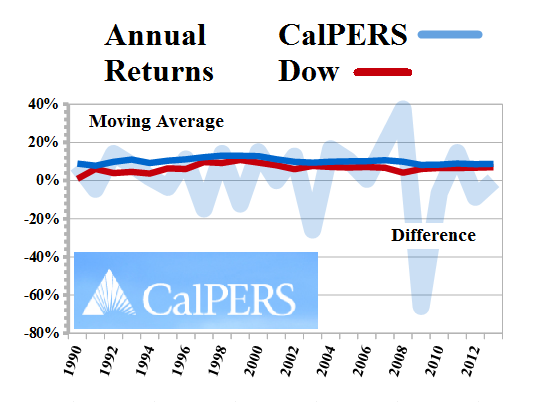

Figure 3: CalPers Returns & the Dow Jones Industrial Companies

In contrast to GPIF and NBIM, CalPers has over 3,000 employees, and over 30,000 who are retired and drawing a retirement pension, thirteen board members, and spends about $2 billion, every year, to manage these funds, and we find that to be very disturbing; please see Figure 3 on the right.

In twenty years of investment management, CalPERS (blue line) has returned the Dow Jones Industrial Average (red line), but the “shadow” shows the difference (net) between CalPERS annual returns against the Dow.

For more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.