(P&I) The Process – Option Pricing

Figure 1: Black-Scholes Option Pricing Formula

Essay. Although the assumptions don’t deny it, and even make it possible through “frictionless” transactions in any amount, it is not possible to buy the whole company (S) at the strike price (K) with enough call options at the purchase price (C).

For example, General Electric (GE) is trading at $26 today and has 10.028 billion common shares outstanding, which implies a current market value of $258.6 billion; we can buy the January 17, 2015 call option with strike price $24 (K) for $2.16 (C) today and be assured that for $2,400 then and $216 now, we can buy 100 shares of GE on January 17, 2015, no matter at what price they’re trading, and if it’s above $24, we could sell the options and not even buy the stock.

Similarly, we can buy the January 17, 2015 put option with strike price $24 (K) for $0.62 (P) today and be assured that no matter what the price of GE then, we are sure to get no less than $24 per share then; and, again, the put option can be sold if GE is trading for less than $24 then.

The Volatility Game

Hence, although put and call options can be useful to investors – that is, those who are concerned about capital safety, liquidity, and a hopeful return above the rate of inflation – options are especially attractive to gamblers and the leverage makes them even more attractive, and the pseudo-scientific option pricing formula (please see Figure 1 above) makes them look to be something more than just a lottery ticket.

And they are (more) because they’re a fixed price for rights in the context of uncertain prices due to “volatility”.

In order for us to understand “option pricing”, we need to have a better idea of what it is that we’re buying; for example, if it’s not an “investment” – safe, liquid, and hopeful – there’s no reason for us to buy it, and we certainly don’t need “volatility protection” because we already have it – for free and “volatility” is an opportunity, not a hazard – by simply buying and holding only (B)-class companies that are trading at prices at or above the price of risk; please see, for example, our recent Post on “(B)(N) What’s A Girl To Do?“.

Moreover, we also know that a company that has a net worth (shareholders equity) of (N), today, by the books, actually has a shareholders equity of (N*), which could be more or less than (N), and in order to get it, or lose it, the company just has to keep on doing what it’s doing, day-in, day-out, Monday through Friday; please see The Theory of the Firm.

What we don’t know is when the company will be “worth” (N*), and even then, we don’t know what the market will be willing to pay for it because there is no connection between stock prices and the shareholders equity.

However, we do know that we can’t expect to buy it for less than its market value ($267 billion in the case of GE), even should it suffer some misfortune in the stock market such as $200 billion; nor can we expect to buy it for a 30% or 50% premium ($350 billion or $400 billion) because the earnings are just $12 billion a year, and its already returning 72% ($8.8 billion) of those earnings to the shareholders as dividends, so the yield on such an investment would be quite meagre at around 3% per year even if we owned all of the earnings.

Moreover, the stock price has no influence on the earnings – the company will keep on producing regardless of the stock price – but a variation in earnings, even quarterly, might affect the stock price, for good or ill, because many investors place a high premium on yield and fancy that they know something about the company’s future based on the most recent earnings report; please see our recent Post “(P&I) Dividend Risk and Dividend Yield” for more information.

But investors are, on balance and in aggregate, very confused, or conflicted, in what they expect from dividend safety and dividend yield, and what they are willing to pay for either; please see Exhibit 1 below (and for more details, the aforementioned Post).

Exhibit 1: S&P 500 NYSE Dividend Risk and Dividend Yield

S&P NYSE Dividend Risk and Dividend Yields

From the chart, it would appear that a change in the “dividend risk”, 1 + log(Dividends/Earnings), has an unpredictable, effectively “random”, effect on the “dividend yield”, Dividends/Stock Price; that is, increasing the dividend payout rate, might not move the stock price upwards, nor will decreasing it tend to move the stock price downwards, with the objective of maintaining a constant, or consistent, dividend yield.

Fama & French, 1988

That result is in accord with the literature on the subject, that increasing the dividend payout rate has a “random effect” on stock prices in the short-term, but could have a lasting effect in the long-term that will tend to “level-out” the yields, and that policy may be effected by a portfolio policy of “sell on the left and buy on the right”; please see our Post “(P&I) Dividend Risk and Dividend Yield” for more information.

Compensation!

We could think, then, about being compensated for the market failure to do the right thing, that is, to bid-up the stock prices of companies with increasing dividend risk (and, therefore, higher payout rates), and write-down the stock prices of companies with decreasing dividend risk.

The former would be a long-dated in-the-money call option, and the latter, a long-dated in-the-money put option, both of which tend to be “cheap”, but how cheap is cheap enough?

Because “volatility” is no guide, as might be noted in the nearly four-fold difference in today’s price for the call and put options on GE at the same price and date six months from now, although we could pay a premium of $2.78 per share ($2.16 plus $0.62) today to guarantee a stock price of $24, for us, then; please see above.

Our goal, then, is that if we are satisfied with today’s yield, Dividends(S)/S, at the stock price and market value, S, what price, K, do we need in order that Dividends(K)/K = Dividends(S)/S as “dividends” varies with the dividend risk, Risk(S) = 1 + log(Dividends(S)/Earnings(S)) and, hence, the payout rate with respect to earnings?

The equation requires that log(S/K) = log(Dividends(S)) – log(Dividends(K)) = Risk(S) – Risk(K) + log(Earnings(S)/Earnings(K)) where, we note again, that S and K are the market values of the company, and S/K is then the ratio of stock prices if the number of shares outstanding is constant, and the prominence of that ratio as log(S/K) assures that we’re in the same game as Figure 1 above.

Dividing both sides of this equation by S-K, we have to conclude that dlog(S)/dS = dRisk(S)/dS + dlog(Earnings(S))/dS at S=K, for any K, and, by re-arranging the terms, that dRisk(S)/dS = -d[log(Earnings(S)/S)]/dS at S=K, and we’re concerned now with all of the earnings, Earnings(S), and not just the Dividends(S).

Figure 2: Do what you will, but pay us.

But that’s an ownership right. In other words, we want, as compensation, that the market should pay us our share of (N*) which is the “worth of the firm” relative to (N), which is the shareholders equity and ownership of the firm.

Which means that we want the market to pay us, now, our share of the Coase Dividend, which they have failed to recognize by not bidding-up the stock of a (hard-working) company with an increasing dividend risk and payout rate, Risk(S), or by not writing-down the stock of a company with a decreasing dividend risk and payout rate, Risk(S), in order that our dividend yield might remain the same, in all seasons, regardless of the market’s deliberations today, because the company will keep on producing regardless of the stock price, to which we are exposed but over which we have no control.

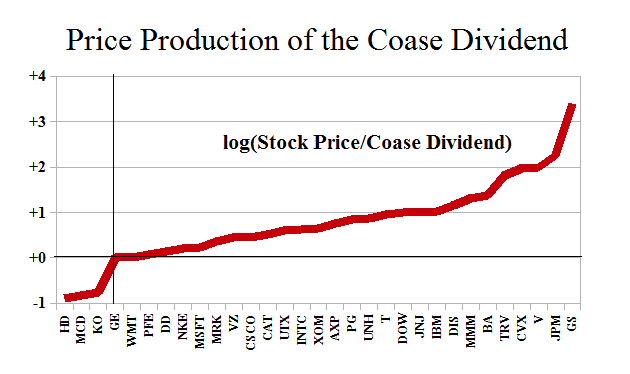

Figure 3: Price Production of the Coase Dividend

For example, the Coase Dividend of the General Electric Company is $10 billion for which the market is willing to pay – by demonstration – $26.57 for $1 of the Coase Dividend which calculates the “balance sheet worth of the trading connections” and, therefore, the balance sheet worth of the company’s enterprise, which has to do with producing and selling their products, day-in and day-out, regardless of the stock price.

We can certainly protect out interest in the Coase Dividend by buying a “collar”, but we need to know when it needs “protection”, and at what price, because options are priced on “volatility” and not risk and, so, despite all odds, might lock-in a current stock price for no reason at all because nobody knows why a stock price is what it is.

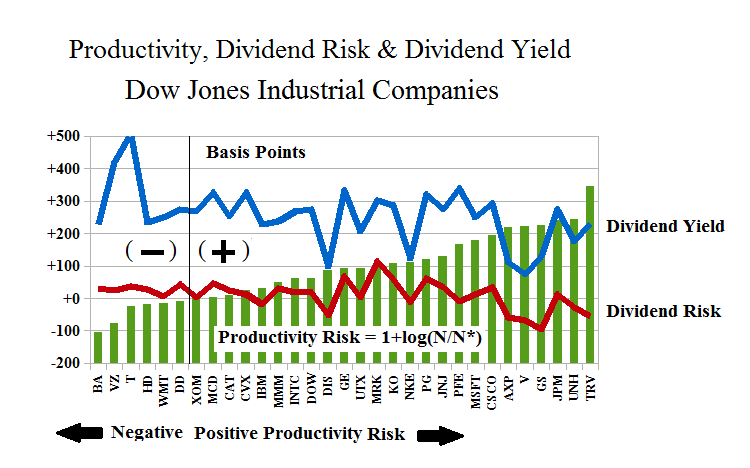

Exhibit 2: The Dow Industrials – Productivity Risk, Dividend Risk and Dividend Yield

Figure 2.1: Dow Industrials Dividend Risk and Dividend Yield |

Figure 2.2: Dow Industrials Productivity Risk, Dividend Risk & Dividend Yield |

Figure 2.1 shows the rising Dividend Yields even as Dividend Risk is rising, where Dividend Risk = 1 + log(Dividends/Earnings), and we think of the earnings as “producing” the dividends; negative dividend risk means that the dividends are a smaller portion (less than 36.8%) of the earnings, and therefore “easier to produce”, whereas positive dividend risk means that the dividend payout is in excess of 36.8% of the earnings and, therefore, “harder to produce” and maintain the Dividend Yield, which will be higher if the stock price is too low.

In Figure 2.2, we have defined “Productivity Risk” = 1 + log(N/N*), so that negative productivity risk means that N*>N and, in fact, N*>e×N, where e is the exponential, e=2.71828 … and 1/e=0.368 … defines the “break-point” between “easier on the left” and “harder on the right”, and we are thinking of N*>N as “preserving N”, and not so much as enhancing it, which it may also do and which we also expect.

Both the Dividend Yield (blue line) and the Dividend Risk (red line) are drifting downwards as the Productivity Risk (green) is increasing; however, the chart suggests that the Walt Disney Company (DIS), Nike (NKE), American Express (AXP), Visa (V), and Goldman Sachs (GS), are all “overvalued” (on the right, in this case, because of the change in orientation) and likely to attract price declines and, hence, they suggest that we buy “put options” as a defence; on the other hand, Verizon (VZ) and AT&T (T), on the left, are grossly “undervalued” by the same standards, and suggest a “call option”.

The Options Trap

Because investors price options on the basis of “volatility (σ)” (please see Figure 1 above), they have no idea of what a company is really “worth” and by that we mean only that our investment in the stock needs to demonstrate the three words – safe, liquid, and hopeful – but we have no control over what the investors will do, and, therefore, no control over how they will price the stock.

But, nevertheless, we know how to pursue our goals – safe, liquid, and hopeful – in any market, if we pursue the likelihood of continued high dividend returns, either because the company tends to return a high percentage of its earnings, or the dividend yields are mis-priced, in our view – that is, they are too high because the stock price is too low (as in the case of Verizon and AT&T), or too low because the stock price is too high, as in the aforementioned cases, and which is due to a lack of consistency confounded by investors who are, in aggregate and on balance, confused and conflicted.

And the high dividend returns are worth pursuing because in all of these cases, these companies have far deeper pockets and far greater resilience, “toughness” in a word, than the investors who are playing the “volatility game” have any idea of.

As a result, we can “price” options in an entirely different way; for example, we think that Verizon and AT&T are “undervalued” (for the reasons above) and, therefore, we can buy the long-dated January 17, 2015 Verizon call at $55 for $0.52 today, and almost surely be in-the-money by then; similarly, for AT&T at $37 for $0.57 today and, again, almost surely be in-the-money by then, so that, in both cases, we not only get the benefit of reliable dividends, but also the benefit of a gain (almost surely) on the options prices which will tend to level-out our yield as a combination of dividends and capital gains on the option prices.

Moreover, since both companies are (B)-class at the present time, we have no concern for the downside because that’s handled by our stop/loss or sell-point below the current stock price, and that’s free.

Tough Companies (Options by Modality)

The reason that Verizon is “undervalued”, and “tough”, is that the “worth” of a company’s process, in-process, is decided by its modality, α=R/P, where (R) is “what is owed to the company” and (P) are its “total liabilities” or “what the company owes”, and all of these companies have modalities that are in excess of α=1, with the only exceptions being Boeing (BA 0.68), Wal-Mart (WMT 0.75), and Home Depot (HD 0.84), although Caterpillar (CAT 1.02), Goldman Sachs (GS 1.08) and JP Morgan Chase (JPM 1.08), are close; all of the others have modalities in excess of α>1.1 and more than half are in excess of α>1.5, and Verizon has a modality of α=1.34; please click on the link for the fundamentals “Dow Jones Industrial Companies – Fundamentals“.

Figure 4: Options By Modality

The reason that these companies are “tough” is that although they might look like “Volkswagens” to summary investors who are daily concerned with externalities that might affect these companies, all of these companies with modality α>1 (Company C), have a “bargaining power” that is well in excess of the basics which keep them in business; please see the chart on the right.

The chart shows the end-of-process conditions for a company to be in-process with that modality, and to stay in-process with the same modality after delivering its product and being paid for it; whereas as the “operational conditions” affecting the payables sets, a(N) for the producer and a(M) from the customer, are “tight” and show only a small relative variation over the entire range of modalities, the negotiable receivables sets, b(N) for the producer and b(M) for the customer, are “explosive” at high modalities (red line) and show that the producer, with a high modality (Company C), has a lot of flexibility in negotiating the price and, therefore, the profit of their product.

All-weather Delivery. Courtesy: Rapunzel

Of course, it’s not a free-hand because the producer will have competition from companies with a similar modality, but it also demonstrates the “pricing power” of companies with a market dominance, or unique product, and the deep-pockets to go with it.

And the price of options on their stock is zero, unless we’re willing to buy them to (almost surely) protect a dividend yield for which investors, otherwise, flee to the comfort of higher-yielding bonds (if they are available).

For more information and additional guides to the theory, please see our Posts “(P&I) The Process – The 1st Real Dollar” which shows how a “currency” gets its value from the “subsistence economy” at the Company D modality, and “(P&I) The Process – The Guns of August” which explains how that modality actually “works”.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}