(B)(N) CLF Cliffs Natural Resources Incorporated

Yes! We can do it!

Casablanca Capital LP

Deal Book. Yet another newly-vested shareholder wants to “maximize shareholder value” (for everybody, we suppose) by buying a small interest (5.2% or about $150 million) in what has been called the “worst performing stock” in the S&P 500 last year and doing a little makeover that will (they think) boost the stock price by more than 100% from the current $20 to $50 and into the “best performing stock” of 2014 or 2015 (The New York Times, January 28, 2014, Casablanca Capital Urges Changes at Cliffs Natural Resources).

Bloom Lake, QC

Courtesy: Cliffs Natural Resources Incorporated

Voilà, that was easy. Just think about it and it’s done! And, indeed, it is hard to imagine that Cliffs Natural Resources could spend $6.4 billion in acquisition ($4.9 billion) and development ($1.5 billion) costs on Bloom Lake, QC when Rio Tinto’s share of Iron Ore Canada is right next door and with a train and harbor and everything and is on the block and begging for less than $4 billion.

Has there been a “strategic” error or are we seeing the making and dissolution of a world class iron ore behemoth north-east of the “Plains of Abraham” QC? And to add to its woes, the “Ring of Fire” project in northern Ontario has also dimmed since last year and Casablanca Capital LP is urging the creation and spin-off of “Cliffs International” and a retrenchment in US assets “Cliffs USA” which will be a new Master Limited Partnership (MLP) with new shareholders who will reap the benefits from the current shareholders until the next IPO.

All of this pales in the face of the loss of $10 billion in “shareholder value” since 2011, from $13 billion to $3 billion in less than three years. Who will pay those shareholders for their losses or does that “shareholder value” no longer matter? Please Exhibit 1 below.

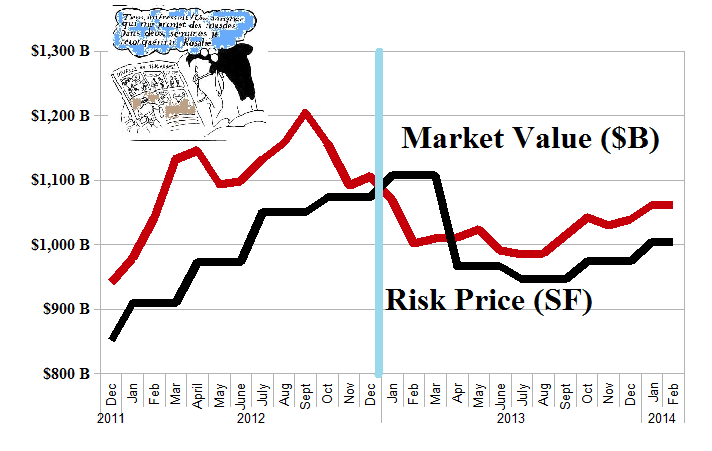

Exhibit 1: (B)(N) CLF Cliffs Natural Resources Incorporated – Risk Price Chart

(B)(N) CLF Cliffs Natural Resources Incorporated – January 2014

Investors who did not know, or even consider, the “price of risk” paid the “cost of it” and (from the chart on the left) there were buyers at every price from $90 all the way down to the current $20, and there are buyers now and no doubt looking for still more “heads and shoulders” and “dead cat bounces”. OK.

(Please Click on the Chart to make it larger if required.)

Moreover, Cliffs Natural Resources is not alone at the bottom and FirstEnergy Corporation ($14 billion), Peabody Energy Corporation ($5 billion) and Newmont Mining Corporation ($12 billion) could probably also use an energetic “facelift”. In fact, there are more than thirty companies in the S&P 500 that failed to improve “shareholder value” last year. Possibly, they just need some “counselling” and we can send them on their way for a better new year? Please see Exhibit 2 below.

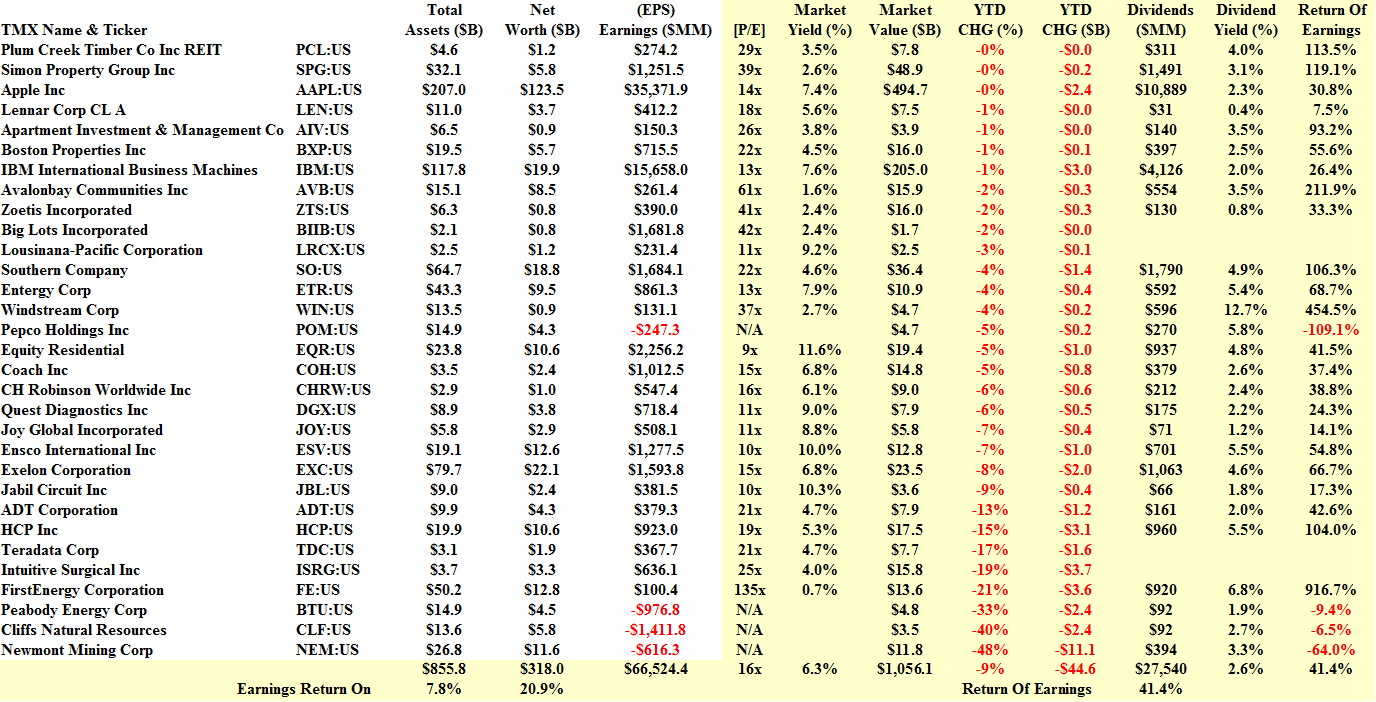

Exhibit 2: S&P 500 “Losers” – Fundamentals – January 2014

S&P 500 Losers – Fundamentals – January 2014

The S&P 500 Undervalued Losers – January 2014

These thirty-one companies suffered a “reversal of fortune” and lost $45 billion of “shareholder value” last year but, despite all of that, paid $27.5 billion in dividends to their shareholders for an aggregate yield of 2.6% and returned 41% of their earnings, such as they were – a lousy $66.5 billion and a paltry 20% return on the shareholders equity and a miserable aggregate 6% on the market value.

Don’t worry. We’ve got it covered.

Some, such as Apple Incorporated, are already in remedial care. We were spared the worst of this conflagration but still ten of the thirty-one are in the Perpetual Bond™ right now and our estimate of the downside risk is minus (7%) but we can probably deal with it without any help. Please see Exhibit 3 below.

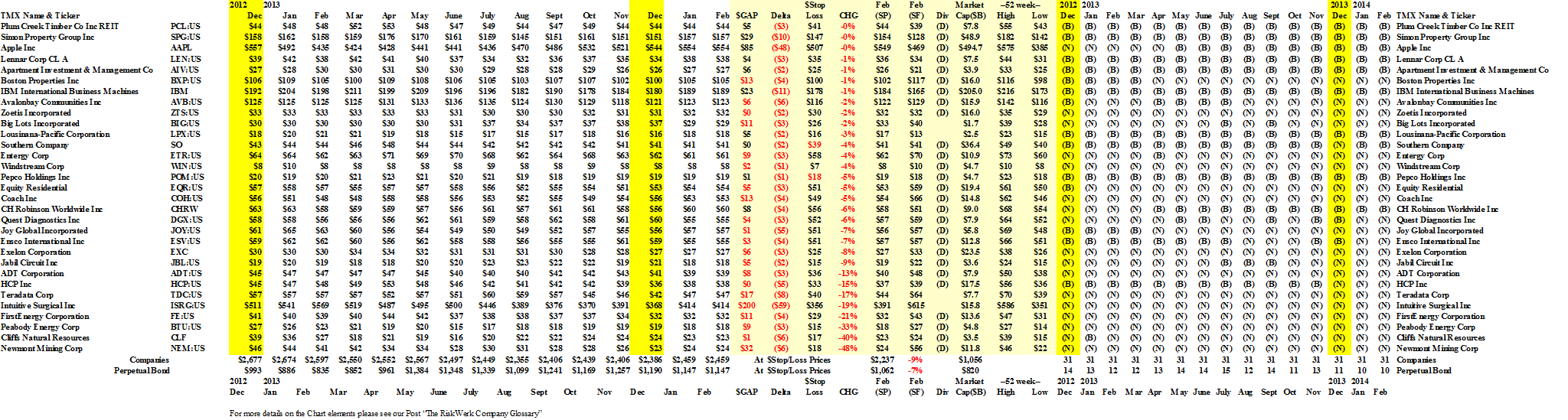

Exhibit 3: The S&P 500 Losers – Prices & Portfolio – January 2014

The S&P 500 Undervalued Losers – Prices & Portfolio – January 2014

(Please Click on the Chart to make it larger and again if required.)

For more information on the chart elements and additional references to the theory, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.