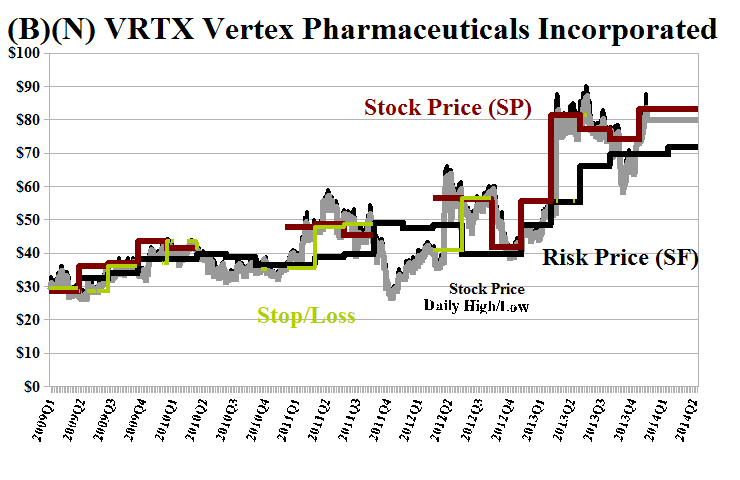

(B)(N) VRTX Vertex Pharmaceuticals Incorporated

Pharmaceuticals

Drama. Pharmaceuticals were hot last year and some analysts are kicking themselves for not seeing the future sooner (The Street, January 27, 2014, Vertex Has the Potential to Go Vertical). Understandable. But we can’t live like that. It makes us sick. Every day a new rumour. Every day a new clinical trial. Every day a new FDA assessment, and so forth.

Drugs

And at the end of the day – if there is one because this industry promises a lot more than it delivers – the smaller companies and laboratories will be taken over by the larger ones who can produce and market the product if the product is “big” enough.

In the meantime, the companies are funded by speculative equity capital and convertible preferred shares – it’s doubtful that anyone will lend them money because there’s not much inventory or fixed assets or income – and they seldom pay a dividend and don’t have any earnings to speak of. So why worry about them? Please see Exhibit 1 below.

EPS $1.80, you say?

Irrelevant, we say.

But the earnings reports for some of the pharmas (Amgen, Biogen, Vertex, Celgene and Alexion) are on parade this week and from an investor point of view – we want our money to be safe and obtain a hopeful but not necessarily guaranteed return above the rate of inflation – these reports are irrelevant and all we can do is weather the stock price storms that are likely to occur and see if there aren’t some new buying opportunities at lower prices as some investors sulk off, their hopes, desires and proscriptions unfulfilled, for now.

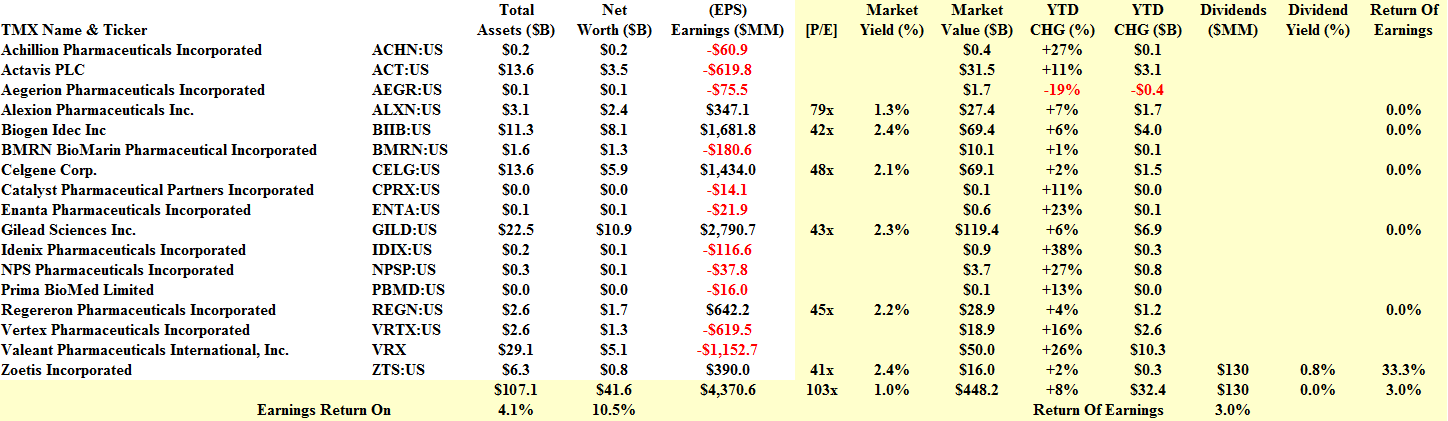

Exhibit 1: Small Pharma – Fundamentals – January 2014

Small Pharma – Fundamentals – January 2014

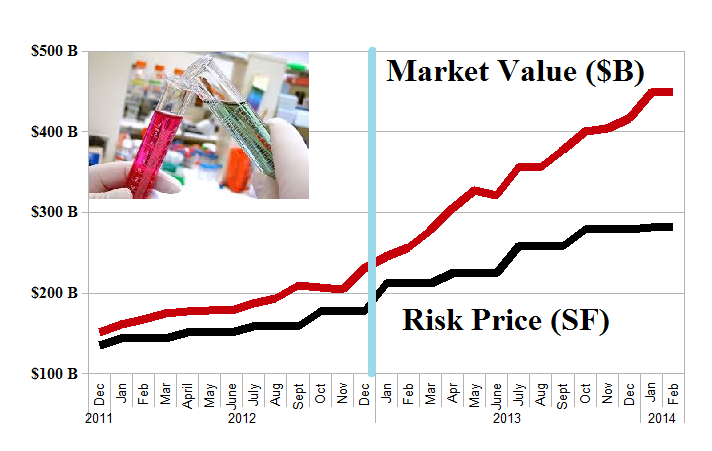

Exhibit 2: (B)(N) The “Undervalued” Small Pharma – January 2014

The Undervalued Small Pharma – January 2014

The reason that these companies are “undervalued” is not because they can be bought at low prices – they can’t because they’re up +30% last year and already +8% this year. Or that the aggregate [P/E]-multiple is low – it isn’t low at 103×.

The reason that they’re “undervalued” is that the demand for the stocks exceeds their supply and that the investors who are buying and holding these stocks at these prices – for whatever reason, hope or desire – are refusing to sell them for less. At least for the moment.

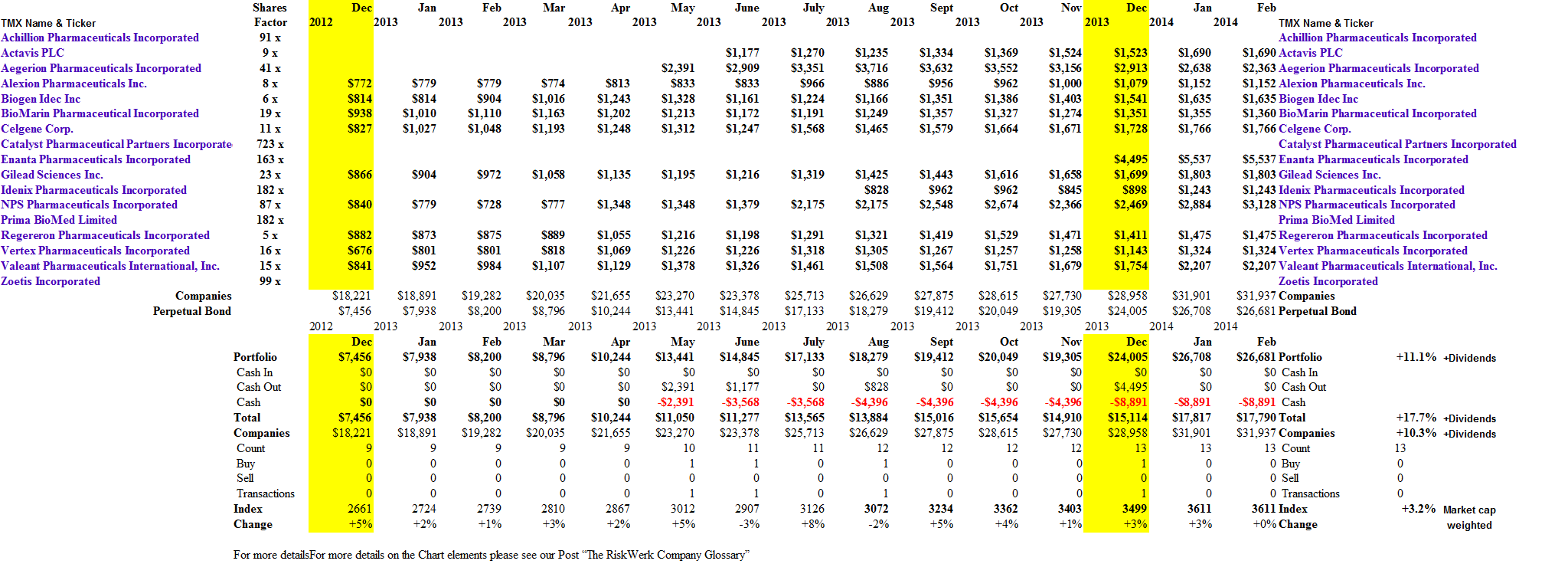

Based on the chart above, we could think about owning them all – like a “gene” pool – and just wait and take some profits when we need some “liquidity”. However, only thirteen of these seventeen companies are currently in the Perpetual Bond™ and that portfolio has returned +18% so far this year, and we’re still in January. Moreover, our estimate of the downside in the portfolio due to the demonstrated volatility of the stock prices is minus (14%) in the next quarter. Please click on the links “(B)(N) Small Pharma – Prices & Portfolio” and “Portfolio & Cash Flow Summary” for more details.

Today’s poster child, Vertex Pharmaceuticals, is a relatively simple example of the “dynamic verticality” of this market. Other things can happen such as “going to ground”.

Exhibit 3: (B)(N) VRTX Vertex Pharmaceuticals Incorporated – Risk Price Chart

(B)(N) VRTX Vertex Pharmaceuticals Incorporated – January 2014

Vertex Pharmaceuticals discovers, develops and commercializes small molecule drugs for the treatment of serious diseases.

(Please Click on the Chart to make it larger if required.)

From the Company: Vertex Pharmaceuticals Incorporated engages in discovering, developing, manufacturing, and commercializing small molecule drugs for patients with serious diseases. Its products include telaprevir for the treatment of adults with genotype 1 hepatitis C virus (HCV) infection, which is marketed in the United States and Canada under the INCIVEK brand name; and ivacaftor for the treatment of cystic fibrosis that is marketed in the United States, Canada, and Europe under the KALYDECO brand name. The company, through its collaboration agreement with Janssen Pharmaceutica, N.V., also markets telaprevir in Europe and other countries in Janssen’s territories under the INCIVO brand name, as well as in Japan under TELAVIC brand name. It is also developing drug candidates for the treatment of cystic fibrosis, including VX-809, which is in Phase III clinical trial and VX-661 that is in Phase II clinical trial; and drug candidates for the treatment of HCV infection, such as VX-135 (ALS-2200), which is in Phase II clinical trial and VX-222 that is in Phase II clinical trial. In addition, the company develops VX-509, which is in Phase II clinical trial for the treatment of autoimmune disease; and VX-787 that is in Phase II clinical trial for the treatment of influenza. Vertex Pharmaceuticals Incorporated was founded in 1989, has 2,200 employees and is headquartered in Cambridge, Massachusetts.

For more information on the chart elements and additional references to the theory, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}