(B)(N) GM General Motors Corporation

GM USA in Detroit, Michigan

Drama. GM is under pressure again and it seems that everyone and anyone who has an interest in political gain-saying is trying to scrape the paint, even though governments have no idea of how to balance their own budget nor even why they would; in economic terms, a balanced budget is a vote for unemployment and slow or no growth, so let’s turn to the law (Reuters, May 22, 2014, Canada keen to find out if GM Canada delayed recalls, breaking law).

The government also has more than 220,000 employees, which is what GM has, but we don’t know how much they made per desk or what dividends they paid. On the other hand, GM paid out $2 billion in dividends for a return of earnings of over 100% and a dividend yield of 3.4% last year, which is a lot better than the government bond yield of 1-year 1% and 1% below the rate of inflation. Nor did anybody return their earnings. Are we too “monetary” or should we be more appreciative of all the “good stories” coming out of Ottawa about “breaking laws” and Senate investigations?

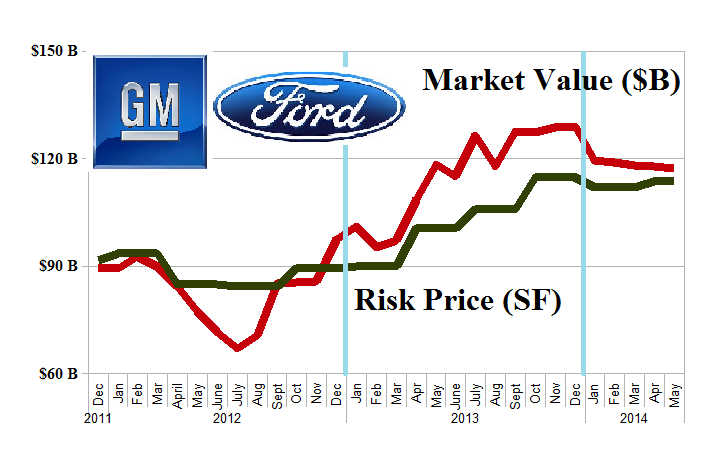

But the good news here is that auto-making in Detroit is on the good road to recovery despite the political sand-traps; please see Exhibit 1 below for the new fundamentals and Ford too.

Exhibit 1: The New Auto America – Fundamentals – May 2014

The New Auto America – Fundamentals – May 2014

(B)(N) The New Auto America – Risk Price Chart – May 2014

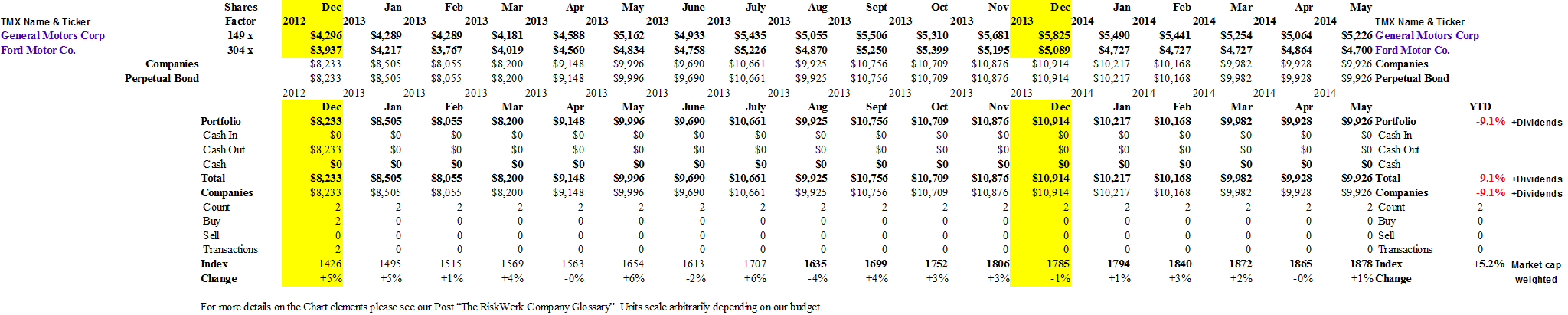

Managing this portfolio was a no-brainer last year; both companies were in the Perpetual Bond™ all of the time (please see Exhibit 2 below) and on an equal weighted-by-value basis and no margin account, the portfolio returned +33% although it’s off minus (-9%) so far this year and our estimate of the downside in the next quarter is minus (-4%); please click on the link (and again to make it larger if required) “(B)(N) The New Auto America – Portfolio & Cash Flow Summary – May 2014” for more details.

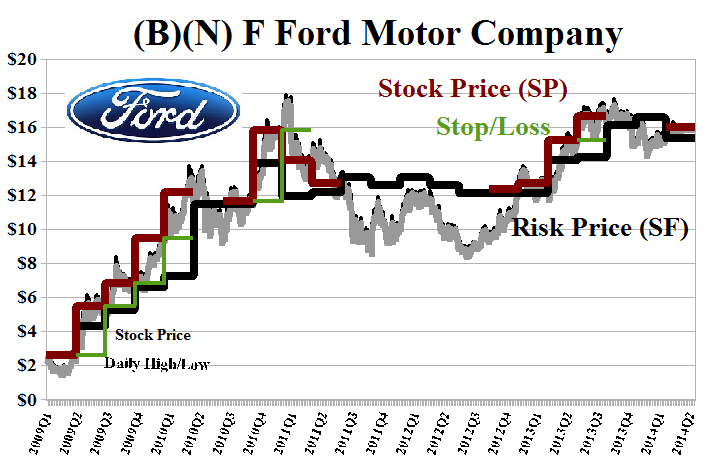

Although it’s important to manage the stop/loss and take profits if the market is giving us the money, we will still buy them back if they’re trading above the price of risk and for no other reason than that; please see Exhibit 3 and 4 below.

If you understood that, we mis-spoke. Mr. Greenspan 1987

The fundamentals are a little bit more complicated and depend on the Theory of the Firm and we need to distinguish between two relatively new concepts; one is the Coase Dividend which we also call the “value of the enterprise” (the underlined) and the other is N* which we may sensibly call the “enterprise value” (but not to confuse it with a similar term from accounting) but we can also call it the “value of the enterprise” (the not underlined) but it should not be confused with the “value of the enterprise”.

The latter is the Coase Dividend and it is the balance sheet worth of the trading connections in the sense of Coase and, therefore, it is the “value of the enterprise” which is something that we prove in the Theory of the Firm.

With reference to Exhibit 1, investors are willing to pay $28 for $1 of the Coase Dividend in the case of General Motors, but only $19 for $1 of the Coase Dividend in the case of Ford; neither value is particularly astounding or off the scale (for off the scale please our recent Post “(B)(N) Valeant Pharmaceuticals International Incorporated” and the reasons for it) but each price measures or values the same thing and it is monetized in the same way for both companies by working the trading connections which are their suppliers and employees, their creditors and debt-holders, their customers and sales networks, and all of the contractual relations and routine that they have established in that network, all of which is necessary to build, sell and deliver their products in excess of mere raw materials and idle plants or inventory waiting to be sold.

The “worth” of said “working”, which we call GW* in Exhibit 1, is $2 billion in the case of General Motors and $3.2 billion in the case of Ford (which is also carrying a lot more debt than General Motors, both absolutely and relative to its net worth) and that result is reflected in the “value of the enterprise” (N*) which is $50 billion in the case of General Motors and $77.3 billion in the case of Ford (please see Exhibit 1), and those values can be compared with the current net worth of the firms, $42.2 billion for General Motors and $26.8 billion for Ford; in plain terms, (GM) $42.2 billion to $50 billion, and (Ford) $26.8 billion to $77.3 billion, and all that they have to do is do what they’re doing now, day-after-day, Monday through Friday.

None of this, of course, tells us what the future will be or what investors might be willing to pay for it or some other future that they might imagine, now, but we might say that Ford has more traction than GM at the present time and that, therefore, the price of GM might be a little high, or the price of Ford might be a little low, and the price of risk helps us to make that distinction and determine what investors are willing to pay for it now, regardless of what other future they might imagine.

Exhibit 2: (B)(N) The New Auto America – Prices & Portfolio – May 2014

(B)(N) The New Auto America – Prices & Portfolio – May 2014

Exhibit 3: (B)(N) GM General Motors Company – Risk Price Chart – May 2014

(B)(N) GM General Motors Company

General Motors Company designs, builds and sell cars, trucks and automobile parts. The Company also provides automotive financing services through General Motors Financial Company Incorporated.

From the Company: General Motors Company (GM) designs, manufactures, and markets cars, crossovers, trucks, and automobile parts worldwide. The company markets its vehicles primarily under the Buick, Cadillac, Chevrolet, GMC, Opel, Holden, and Vauxhall brand names, as well as under the Alpheon, Jiefang, Baojun, and Wuling brand names. It also sells cars and trucks to dealers for consumer retail sales, as well as to fleet customers, including daily rental car companies, commercial fleet customers, leasing companies, and governments. In addition, the company offers connected safety, security and mobility solutions, and information technology services. The company, through its subsidiary, General Motors Financial Company, Inc. provides automotive financing services and lease products through GM dealerships in connection with the sale of used and new automobiles that target customers with sub-prime and prime credit bureau scores. The company was founded in 1908, has 220,000 employees and is based in Detroit, Michigan.

Exhibit 4: (B)(N) F Ford Motor Company – Risk Price Chart – May 2014

(B)(N) F Ford Motor Company

Ford Motor Company is a producer of cars and trucks. Its business is divided into two segments: Automotive and Financial Services.

From the Company: Ford Motor Company develops, manufactures, distributes, and services vehicles, parts, and accessories worldwide. The company operates through two sectors, Automotive and Financial Services. The Automotive sector offers vehicles primarily under the Ford and Lincoln brand names. It markets cars, utilities, trucks, service parts, and accessories through distributors and dealers in North America, South America, Europe, Turkey, Russia, and the Asia Pacific region. This sector also sells vehicles to dealers for sale to fleet customers, including commercial fleet customers, daily rental car companies, and governments, as well as provides maintenance and repair services. The Financial Services sector offers various automotive financing products to and through automotive dealers. This sector provides financing products, which include retail installment sale contracts for new and used vehicles; leases for new vehicles to retail customers, government entities, daily rental car companies, and fleet customers; wholesale financing that comprise loans to dealers to finance the purchase of vehicle inventory; loans to dealers to finance working capital, purchase dealership real estate, and other dealer vehicle program financing; and other financing products, as well as provides insurance services. Ford Motor Company was founded in 1903, has 180,000 employees and is based in Dearborn, Michigan.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}