(B)(N) Technology Angst

Gandalf the White

Courtesy: Evenstar

Drama. Whenever we turn on our laptop computer, we know that in the next five seconds until the keyboard is given back to us and the network is connected, more computations have been done than were ever done in the entire 19th century and the twenty centuries before that.

With that sense of awe and lack of comprehension, we need to respect the projections of Mr. John T. Chambers, the CEO of Cisco Systems Incorporated, when he says “You are going to see a brutal, brutal consolidation of the IT industry where out of the top five players, only two or three of us will be meaningful in as quick as five years” (Business Insider, May 20, 2014, Cisco CEO: ‘Brutal’ Times Are Coming For The Tech Industry).

But we don’t know which two and even Gandalf (the magician) might have to die, so we lined them up in a portfolio, and that can’t be all bad. And in our search for enlightenment, we also added Intel Corporation which serves them all. However, we found what we always seem to find in industries that are competing only with themselves – they will build it and the customers will come, eventually. Perhaps that’s what Mr. Chambers means – they don’t have enough customers yet and there might not ever be enough because collaboration tools sounds more like entertainment than a product that would be essential to enhance productivity or profitability.

As noted by the other “Ring Masters”, change is always effected by only one person.

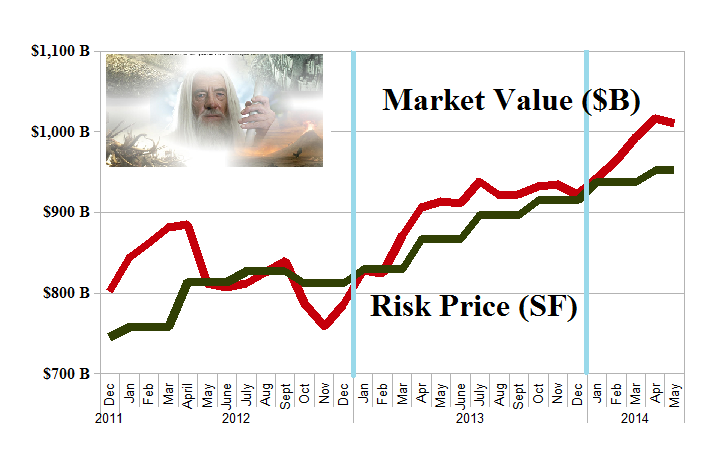

Please see Exhibit 1 below for the modern fundamentals and our synopsis of what currently is.

Figure 1: The Disconnected and The Unconnected

Courtesy: CiscoLive!

Milan 2014

Mr. Chambers also predicted that most of his competitors in this industry will fall in the next five years (please see the chart on the left) and we have concluded that their customers must “needs be driven” towards the “greater Cloud and The Great Ring Fence” that will envelop us all (Reuters, May 21, 2014, EBay asks 145 million users to change passwords after cyber attack).

Again, we’re not really sure about that either because these companies demonstrate the common struggles of mortals to excel, and sometimes they are known to prevail against all odds and deeper pockets and a compelling vision that might not think of everything at the right price. Please see Exhibit 2 below for what we think but don’t know.

Exhibit 1: Technology Angst – Fundamentals – May 2014

Technology Angst – Fundamentals – May 2014

(B)(N) Technology Angst – Risk Price Chart – May 2014

As an investment portfolio, this is not too bad, and these companies might be able work on the next vision and still make money now.

Last year, they earned $70 billion and returned 36% of it to the shareholders for a payout of $25 billion and an aggregate yield of 2.5%; please see Exhibit 1 above.

To make earnings, they’re also turning over their inventory 4× a year or every three months which is interesting because the nature of this business is not fruits & vegetables.

In contrast, what Mr. Chambers deems to be his competition is more like “bread-boarders”; that is, they make, sell and install these products for smaller businesses which might gain some competitive advantages by using some collaborative technologies if they’re not too expensive. But it seems to be a hard-scrabble business and their next customer might be their last and we might be the last to know. Please see Exhibit 2 below.

Exhibit 2: Against All Odds – Fundamentals – May 2014

Against All Odds – Fundamentals – May 2014

(B)(N) Against All Odds – Risk Price Chart – May 2014

It took us one ring to find them (please see Figure 1 above and the chart on the left), but Arista Networks is privately-owned and Avaya Incorporated is funded by private equity capital and Huawei Enterprise is headquartered in Shenzhen, South China and publishes its balance sheets and stock prices in CNY6.0569 = USD1.00 and although we use their equipment, we’re not motivated to deal with the exchange problem every day; too much can happen before we hear about it and our stop/loss is not effective as such because the company itself is affected inversely to a change in the exchange rate which affects the stock price right away.

Technology Angst

Having said that, we still need to wonder why the other companies have a stock price at all. Please see Exhibit 2 above for the fundamentals.

And please click on the links below (and again to make them larger if required) for more details; we’ve also used terms from the Theory of Firm and The Process which might make for some good summer-time reading that can’t be found anywhere else and can only be bought with a portfolio.

“(B)(N) Technology Angst – Prices & Portfolio – May 2014“, “(B)(N) Technology Angst – Portfolio & Cash Flow Summary – May 2014“, “(B)(N) Against All Odds – Prices & Portfolio – May 2014” and “(B)(N) Against All Odds – Portfolio & Cash Flow Summary – May 2014“.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}

{kind=link}

{kind=link}