(B)(N) PFE Pfizer Corporation

How much do you think?

Deal Book. Pfizer Corporation is making overtures to AstraZeneca PLC shareholders and offering them cash plus some of its stock in exchange for all of theirs; investors are supposed to say, Well OK if that’s what you want – your money is as good as ours. But is it?

If the offer is for all cash ($104 billion with a 30% “premium” or “incentive”) to buy us out, then we could re-invest the money or buy Pfizer stock at the market price if we were so inclined; but even if the offer is for some cash and the balance is in Pfizer stock, we could still sell or keep the Pfizer stock or even buy more of it for the same result.

Please, sir, I want some more – Charles Dickens 1838 Oliver Twist

As investors then we have only two questions about this deal; is the +30% premium enough; that is, is there a reason that we might ask for more?

And secondly, if we hold the Pfizer stock, is it as likely to retain its value as the AstraZeneca stock that we paid for the Pfizer stock; and even more ambitiously, is the Pfizer stock more or less as likely to increase in value (as more or less as likely) than the AstraZeneca stock that we gave up to pay for it?

Governments, of course, have other issues including who pays the tax and the societal benefits of such a deal (Reuters, May 1, 2014, Pfizer’s designs on AstraZeneca stir tax envy among rivals and April 30, 2014, UK lawmakers plan to probe Pfizer pursuit of AstraZeneca).

The “fair price” for these companies is the price of risk because that is the price at which we can expect to get our money back when we need it – 100% capital safety – and have reason to hope for but not guarantee a return that exceeds the rate of inflation which, if we don’t get it, is just another way of losing our money. Another way of saying that is that our money as cash is not as good as is our money invested in the stocks.

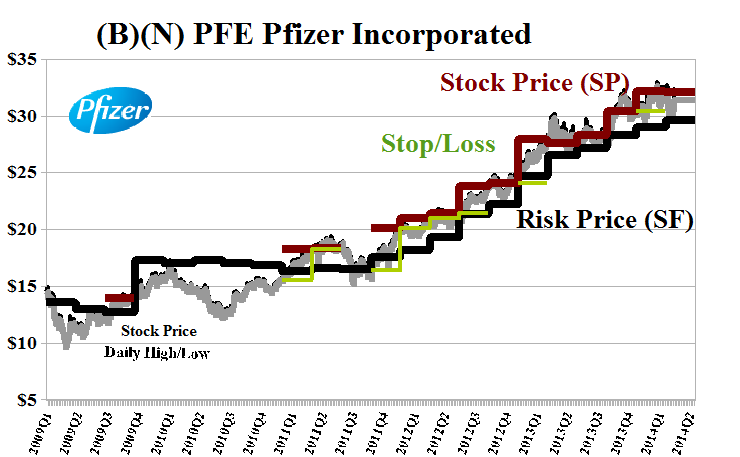

However, investors are currently willing to buy and hold these stocks at a premium above the price of risk which is currently +15% in the case of AstraZeneca and +2% in the case of Pfizer; please see Exhibit 1 below and the charts in Exhibit 4 and 5.

There are many reasons that investors will buy the price of risk forward but certainly one of them is that they expect that they will not receive less in the future and that other investors will buy their stock at that or a better price then; and for the case at hand, undoubtedly the Pfizer Corporation believes that under its stewardship the company will not only obtain the “worth” that is represented in the stock price now which exceeds the price of risk by +15% but at least 30% more.

And we use the term “worth” in this context not as the price of the stock (which will be off the market) but as the “worth” of the enterprise which is encompassed by the firm AstraZeneca and such worth is calculated by the Coase Dividend; please see our recent Post The Process Extreme Alpha for more information and examples of the Coase Dividend.

The Coase Dividend of the two companies combined is their sum, at least at the outset, and if it is to be improved then that will depend on the new management of the combined firm including the possibility of (so-called) synergistic benefits which we are able to measure as a change in the Coase Dividend; moreover, if the deal closes, then the price of risk is the price at which the deal closes and that is also the stock price on that day but might be something different the very next day.

And in that context of deals and mergers and acquisitions, we note that the Pfizer Corporation is still carrying $40 billion in “goodwill” which is about 25% of its total assets and more than 50% of its net worth and we wonder how its doing with working that out.

In order for this deal to be a good deal for the Pfizer Corporation as well as the AstraZeneca shareholders who acquire Pfizer stock, the deal needs to raise the price of risk (not lower it) and that has implications for the premium and also how much cash and how much stock is in the deal; please see Exhibit 1 and 2 below.

The +30% deal costs $103.8 billion and preserves the price of risk at 40% cash and the balance in Pfizer stock; and the +50% deal costs $119.7 billion and does the same at 50% cash and the balance in Pfizer stock; and, as might be expected, the more stock there is in the deal, the lower is the price of risk; moreover, the higher the premium, the more cash there has to be in the deal to make it good.

Exhibit 1: Pfizer Buys AstraZeneca with a +30% Premium on the stock price

+30% Deal

Exhibit 2: Pfizer Buys AstraZeneca with a +50% Premium on the stock price

+50% Deal

We note that the price of the Coase Dividend is not affected by the price of the deal; the reason is that the deal, no matter what the price, is buying only the combined Coase Dividend ($9.8 B) and the combined value of the two companies at their price of risk ($258.9 B) before the deal neither of which are affected by the price that these investors are willing to pay for them.

Exhibit 3: Pfizer Corporation and AstraZeneca PLC – Fundamentals – May 2014

Pfizer Corporation and AstraZeneca Fundamentals – May 2014

Exhibit 4: (B)(N) AZN AstraZeneca PLC ADS – Risk Price Chart – May 2014

(B)(N) AZN AstraZeneca PLC ADS – May 2014

AstraZeneca PLC a biopharmaceutical company focusing on six Therapy Areas: Cardiovascular, Gastrointestinal, Infection, Neuroscience, Oncology and Respiratory & Inflammation. It owns and operates R&D, production and marketing facilities worldwide.

From the Company: AstraZeneca PLC is engaged in the discovery, development, and commercialization of medicines for cardiovascular and metabolic disease; oncology; respiratory, inflammation, and autoimmunity; and infection, neuroscience, and gastrointestinal disease areas worldwide. Its principal products include Crestor for the treatment of dyslipidaemia and hypercholesterolemia; Seloken/Toprol-XL for control of hypertension and for use in heart failure and angina; Iressa for non-small cell lung cancer; Faslodex for breast cancer in post-menopausal women; and Zoladex for prostate cancer, breast cancer, and certain benign gynaecological disorders. The company’s principal products also comprise Pulmicort for treating asthma and chronic obstructive pulmonary disease (COPD); Symbicort for maintenance treatment of asthma and COPD; Nexium for treatment of acid-related diseases; Seroquel XR for the treatment of schizophrenia, bipolar disorder, major depressive disorder, and generalised anxiety disorder; and Synagis for the prevention of serious lower respiratory tract disease caused by respiratory syncytial virus in paediatric patients. In addition, it has 99 pipeline projects, which include 85 in clinical development and 14 either approved, launched, or filed. The company markets its products to primary care and specialist doctors through distributors or local representative offices. AstraZeneca PLC has collaboration agreements with Amgen, Inc. and FibroGen, Inc. The company was formerly known as Zeneca Group PLC and changed its name to AstraZeneca PLC in April 1999. AstraZeneca PLC was founded in 1992, has 52,000 employees and is headquartered in London, the United Kingdom.

Exhibit 5: (B)(N) PFE Pfizer Incorporated – Risk Price Chart – May 2014

(B)(N) PFE Pfizer Corporation – May 2014

Pfizer Incorporated is a research-based biopharmaceutical company. The Company has five operating segments: Primary Care; Specialty Care and Oncology; Established Products and Emerging Markets; Animal Health; and Consumer Healthcare.

From the Company: Pfizer Incorporated, a biopharmaceutical company, discovers, develops, manufactures, and sells healthcare products worldwide. Its product portfolio includes medicines and vaccines, as well as various consumer healthcare products. The companys Primary Care segment offers prescription pharmaceutical products primarily prescribed by primary-care physicians for various therapeutic and disease areas comprising Alzheimers disease, cardiovascular, erectile dysfunction, genitourinary, major depressive disorder, pain, respiratory, and smoking cessation. Its Specialty Care and Oncology segment provides prescription pharmaceutical products for anti-infectives, endocrine disorders, hemophilia, inflammation, ophthalmology, pulmonary arterial hypertension, specialty neuroscience, and vaccines, as well as oncology and oncology-related illnesses. The companys Established Products and Emerging Markets segment offers prescription pharmaceutical products that had lost patent protection or marketing exclusivity in certain countries and/or regions, as well as sold in emerging markets, including Asia, Latin America, the Middle East, Eastern Europe, Africa, Turkey, and Central Europe. Its Consumer Healthcare segment provides non-prescription products in a range of therapeutic categories, such as dietary supplements, pain management, respiratory, and personal care. The company primarily offers biopharmaceutical products, including Lyrica, the Prevnar family of products, Enbrel, Celebrex, Lipitor, Viagra, Zyvox, Norvasc, Sutent, and the Premarin family of products; and consumer healthcare products under the Advil, Caltrate, Centrum, ChapStick, Emergen-C, Preparation H, and Robitussin brands. It sells its products to wholesalers, distributors, retailers, hospitals, clinics, government agencies, pharmacies, individual provider offices, and grocery and convenience stores. Pfizer Incorporated was founded in 1849, has 78,000 employees and is headquartered in New York, New York.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.