(B)(N) The Other West Side Story

The West Side Story

Courtesy: Robert E. Griffith and Harold Prince 1957 Producers

Drama. We didn’t have to go far to find “emerging markets” in North America; there’s one in the NASDAQ and there’s another even larger one in the S&P TSX; and yet another still larger in the S&P 500 for an aggregate market value of $560 billion which is up +9% so far this year but it took all of last year to get that number ($46 billion and +9.7%); and naturally, we wonder if they can’t lose it too in a “New York Minute”?

These companies provide a real challenge to “value investors” (which we’re not) who are hoping to buy companies like this – mired in debt and “under-performing” – at “deep-discount” prices and maybe sell them when other investors like them too; that’s also hard to understand unless it’s like a renovations business.

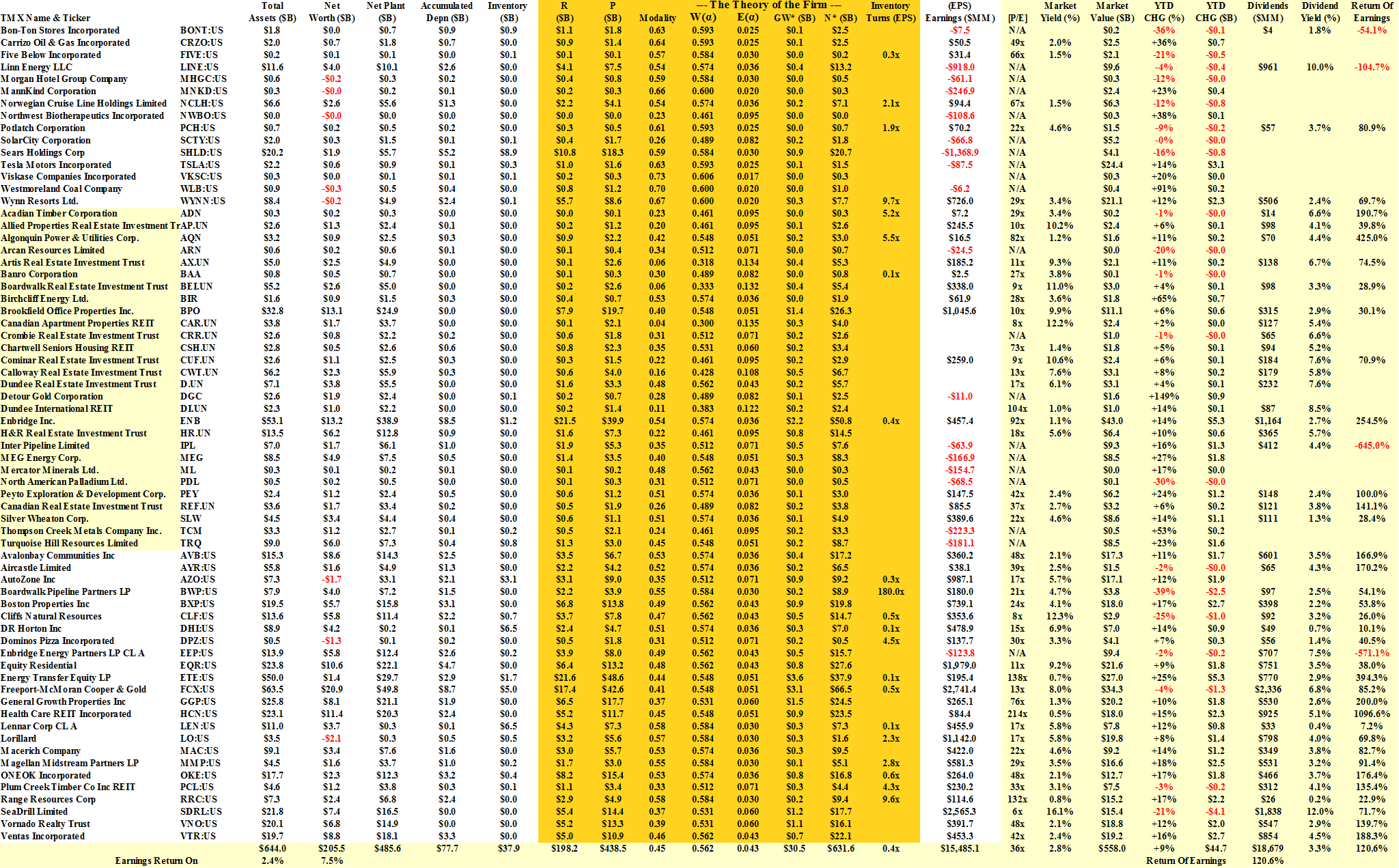

The “fundamentals” are also other-worldly because these companies, in aggregate, have twice as much debt as their net worth and they still paid (or bled) $18.6 billion in dividends last year which is 120% of their earnings and gave investors a 3.3% dividend yield plus a market price gain of 9.7%; and they are trading now at a [P/E]-multiple of 36× earnings which is a 2.8% yield on the stock price – all the while the rest of the New York-world was worth about $20 trillion and up over 20% last year; some investors eschew the subway and like to walk on principle, we guess.

We combined all three of these markets into one with a net modality of α=0.45 which puts them within spitting-distance of the Company A modality of α<1/e=0.368… and many of them, of course, are running at a much lower rate; however, that’s close enough to “emerging markets” as a Company A and that modality is also typical of new firms freshly-funded; please see our Posts on The Process and The Theory of Firm for more details. Of the sixty-seven companies in this portfolio, only thirty-six of them are in the Perpetual Bond™ and that portfolio is up +32% in the last three months and selling is not on our mind; the market will tell us when to sell when they hit our stop/losses and “value” has nothing to do with that.

Exhibit 1: The Other West Side Story – Fundamentals – April 2014

The Other West Side Story – Fundamentals – April 2014

(B)(N) The Other West Side Story – Risk Price Chart – April 2014

We can see from the Risk Price Chart on the left that the “basement-dwellers” have had their day; but will the “sunshine” blind-them to where they are which is just on the threshold of the “price of risk“?

Will they know that they bought these companies when they were “overvalued” and will they now sell them just as they have become “undervalued” and are trading at or above the price of risk?

Do they know that the potential for these companies if they just keep on doing what they’re doing is for a net worth (N*) of $632 billion which is 3× the current net worth (N) of $206 billion; and do they know that they are paying only $18 ($558 billion/$30 billion) for $1 of the Coase Dividend whereas in the other New York they are paying $25 for the same thing which is the societal standard of risk aversion and bargaining practice which we all share?

(B)(N) The Other West Side Story in the S&P TSX – Risk Price Chart – April 2014

Probably not and they don’t understand portfolios either and though they might shoot the odd buffalo now and then, they have no chance to get the herd.

The NASDAQ and S&P 500 charts are similar to the one above but the S&P TSX chart is altogether different; please see the chart on the left.

In Canada, they’re only paying $15 ($133 billion/$9 billion) for their Coase Dividend and the expected growth in net worth is from the current $75 billion (N) to $133 billion (N*) and all that these companies have to do is to keep on existing Monday to Friday every day; but that says nothing at all about the stock price which is still “overvalued” (and trading at [P/E] 57× earnings as well) and these companies returned 170% ($4 billion) of their earnings last year ($2.3 billion) for a dividend yield of 3%. Possibly they will do it again this year if they could just borrow more money or float more stock?

Go West you say?

Please Click on the link (and again to make it larger if required) for more of the details on “The Other West Side Story S&P TSX – Fundamentals – April 2014“.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the societal norms of risk aversion and bargaining practice.

And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}