(B)(N) RSTI Rofin-Sinar Technologies Incorporated

The Power of Light

Courtesy: Rofin-Sinar Technologies

Deal Book. We’ve decided that Rofin-Sinar Technologies (which is headquartered in Plymouth, Michigan and makes industrial cutting-edge lasers from milliwatts to kilowatts) is “fairly valued” at the current prices meaning exactly that there is neither an excess demand for the stock at these prices (putting upwards pressure on opportunistic bid-prices) nor an excess supply (putting downwards pressure on negotiable prices with anxious sellers) (The Street, March 14, 2014, Rofin-Sinar, a Cheap Tech Name or Value Trap?).

That is quite a different reason for deciding “value” because we don’t assume that “good values” in terms of the balance sheet, dividends and earnings will push or pull the stock price in any particular direction; if investors decide to bid-up the stock, then it is “undervalued” at the current prices but if they decide to walk away from it, it is “overvalued” at the current prices. And that’s what investors need to know now and at any time because we don’t need to guess the future – it’s already here.

In our view, “bargain hunters” on “value in low-priced stocks” in the stock market have a “thieves mentality” which – we hasten to add – is not the case with “value investors” who are putting-up their money – a lot of it – in order to buy a substantial interest in a struggling company with more potential than is currently appreciated by the stock market.

Nor are we judgemental or do we blame “bargain hunters” for their aspirations because self-delusion is Darwinian in the stock market and a better choice is proactive and puts our money to work now rather than waiting for work later because any relation is possible and routine between stock prices and alleged “good value” and said value might not arrive before dinner-time; so, they’re really taking a chance and we ought to appreciate that.

But if we’re looking for “hidden value” in a company, it’s material for us to look at the industry and see how it’s doing in terms of inventory, plant & equipment, customers and so forth, and whether there might be opportunities for mergers and acquisitions or consolidations; after all, if the institutions start buying or selling these stocks, there’s nothing that “good value” can do for us and the stock of Rofin-Sinar is more than 90% owned by institutions including mutual funds, pension funds and insurance companies, even though the stock doesn’t pay a dividend and there might be some other problems that we’ll discuss below (Exhibit 4); however, for starters, please see Exhibit 1 below for the lighter fundamentals.

Exhibit 1: The Power of Light – Fundamentals – March 2014

The Power of Light – Fundamentals – March 2014

(B)(N) The Power of Light – Risk Price Chart – March 2014

In aggregate these eight cutting-edge and very high technology companies in scientific measurement and instrumentation are “undervalued” at the current prices but that doesn’t mean that we should bid them up or that they’re going to get still higher prices.

It does mean, however, that the current owners of these stocks are unwilling or have no need to sell them at these prices despite nearly no dividends and a return of earnings of less than 16% which is only half the going rate although, magically, they’re up +27% and $15 billion last year but have levelled out recently.

Other things that are noteworthy in the fundamentals are that the total debt is only half the net worth (the total debt is the total assets less the net worth) and that the “inventory turns to make earnings” in aggregate are about 1.4×per year or every 8 months (the ratio of earnings to inventory) with the exception of Rofin-Sinar (0.1× or ten years) and Coherent Incorporated (0.4× or two years) and these latter might have a “sales” problem whereas the Keyence Corporation is selling out every two months (5.2× a year) to make earnings.

Moreover, in aggregate, the industry has the modality α = 3.16 > 1 (please see The Process for more information on “modality”) of a “cartel” which is not based on power relationships but rather on a deep embedding in plant & equipment, skills and bespoke products that can’t be bought curbside or at Wal-Mart; on the other hand, their market doesn’t need a “new one” every few months nor is there only one supplier as far as we can tell, although Rofin-Sinar provides an awesome power.

Six of them are currently in the Perpetual Bond™ and our estimate of the downside risk in the portfolio due to the demonstrated volatility is minus (9%) in the next quarter. Please see Exhibit 2 and 3 below for more details.

Exhibit 2: (B)(N) The Power of Light – Prices & Portfolio – March 2014

(B)(N) The Power of Light – Prices & Portfolio – March 2014

Exhibit 3: (B)(N) The Power of Light – Portfolio & Cash Flow Summary – March 2014

(B)(N) The Power of Light – Portfolio & Cash Flow Summary – March 2014

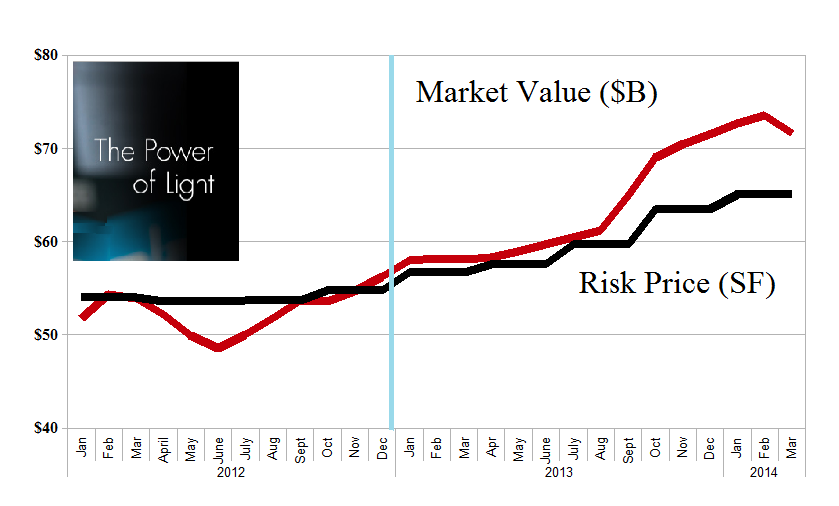

Exhibit 4: (B)(N) RSTI Rofin-Sinar Technologies Incorporated – Risk Price Chart – March 2014

(B)(N) RSTI Rofin-Sinar Technologies Incorporated

Investors are obviously uncertain about the “value” of Rofin-Sinar and there seems to be lots of opportunity for “volatility-players” and day-traders.

It’s currently trading at $23 and below the price of risk, the Risk Price (SF) at $26 and our estimate of the downside in the stock price due to the demonstrated volatility is minus ($2) in a “buyers market”.

Please see Exhibit 2 above for more details.

And for more information on “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.