(B)(N) AC.B Air Canada

Courtesy: Air Canada

Drama. Air Canada is complaining that it doesn’t have enough passengers to justify the freight and so the passengers that it has will have to pay more “until the US straightens out its dollar” because “there’s no free lunch”, they say (CBC, March 8, 2014, Air Canada may hike fares, fees due to low dollar).

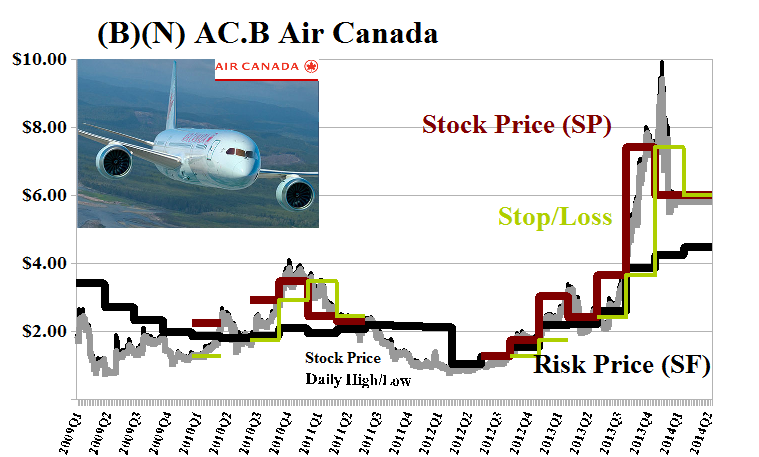

We have patronized the airline before (in November 2013) and nothing has changed except that the stock has caught a down-draft and is trading at $6 and off from the rather lofty $9.50 just two months ago but still substantially up from $1 just two years ago. Please see Exhibit 4 below.

There are at least fifty chartered, more or less regional, airlines in Canada but only three of them are traded in the stock market and although there could be some penny stocks around, these three are more in the “dollar class” ($5 billion with aggregate debts of 3× that amount) and both Transport Canada and the Dow Transports have been off the charts last year. But we’re naturally wondering if the “free ride” is over too and what that means for the price of risk. Please see the fundamentals below.

Exhibit 1: Canada Air – Fundamentals – March 2014

Canada Air – Funadamentals – March 2014

(B)(N) Canada Air – Risk Price Chart – March 2014

Chorus Aviation is a dividend-paying holding company that owns Jazz Aviation LP and that’s what it did with a 98% return of earnings last year and an 11.8% dividend yield. Air Canada doesn’t pay dividends and investors need to fend for themselves although the company bought-in about 20 million of its own shares last year which, in our view, is a lot of sandwiches better spent on the customers. Go figure.

All three of them are in the Perpetual Bond™ which is up +80% last year but we’ve caught some flak recently and our estimate of the downside in the portfolio due to the demonstrated volatility of the stock prices is as much as minus (14%) in the next quarter and we’re tightening up our stop/loss positions on the possibility of a real short order. Please see Exhibit 2 and 3 below.

Exhibit 2: (B)(N) Canada Air – Prices & Portfolio – March 2014

(B)(N) Canada Air – Prices & Portfolio – March 2014

Exhibit 3: (B)(N) Canada Air – Portfolio & Cash Flow Summary – March 2014

(B)(N) Canada Air – Portfolio & Cash Flow Summary – March 2014

(Please Click on the Chart to make it larger and again if required.)

Exhibit 4: (B)(N) AC.B Air Canada – Risk Price Chart

(B)(N) AC-B Air Canada – March 2014

The action in this non-dividend paying “short-order cook” is a volatility feast for the day-traders.

Our stop/loss was triggered at $7.50 and it’s still trading above the price of risk at $4.80 and rising but we can wait on the tarmac with the other passengers before buying it back. There’s no rush just to fasten our seat-belts again and it would be nice if they produced their financial reports on something other than an airline schedule.

(Please Click on the Chart to make it larger if required.)

For more information on “risk management” and additional references to the theory, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.