(B)(N) COV Covidien PLC & The Retail Price

Drama. They say that Covidien PLC is “fully-valued” and it sounds ominous and full of meaning as if to pay more for it now would be criminal or deviant (The Street, February 17, 2014, Covidien Looks Fully Valued). Should we take profits, then, and short the stock, too? Or should we just be happy that we’re “fully-valued” and check our stop/loss in case of surprise, collect our dividends and maybe buy more at the retail price, the “full price” that everybody likes, and see what happens next?

Drama. They say that Covidien PLC is “fully-valued” and it sounds ominous and full of meaning as if to pay more for it now would be criminal or deviant (The Street, February 17, 2014, Covidien Looks Fully Valued). Should we take profits, then, and short the stock, too? Or should we just be happy that we’re “fully-valued” and check our stop/loss in case of surprise, collect our dividends and maybe buy more at the retail price, the “full price” that everybody likes, and see what happens next?

For example, “fully-valued” suggests to us that the company is running on all cylinders, knows where it’s going and can pay its dividends and basically, that it’s a fair stock to own that’s “fairly-valued“. But does it have an overdrive – “fully-valued” suggests not – and what’s that got to do with the stock price? There are lots of stocks that have “no value” to shareholders – they don’t pay dividends and they’re “owned” by the bank and bondsman, dare they pull the plug – but they still have a stock price which could be anything that somebody wants to pay for it. And that sounds effective too.

Exhibit 1: Covidien & The Retail Prices – Fundamentals – February 2014

Covidien & The Retail Prices – Fundamentals – February 2014

Covidien & The Retail Prices – Fundamentals – February 2014

And indeed, with reference to the fundamentals, Covidien PLC is almost spot-on its industry at a 5% market yield (the inverse of the demonstrated [P/E] at 20×) and a 2% dividend, give or take a decimal and we suppose that they could return more of their earnings or buy-in some of their stock?

The industry also returned 50% of its earnings and delivered a 16% return on the shareholders equity which – one must admit -few investors know how to get on their own money. Those who presciently bought in early last year, raked in +28% and $84 billion on the industry and they’ve almost all been in the Perpetual Bond™ since December 2012 and that took down +35% plus dividends and is up +14% so far this year (partially on the back of Given Imaging which just got bought up by Covidien). Please see Exhibit 2 and 3 below.

But there’s more to the story. All of these companies are still “undervalued” because the demand for them at these prices exceeds the supply, and knowing that sooner is better than later.

Exhibit 2: Covidien & The Retail Prices – Prices & Portfolio – February 2014

Covidien & The Retail Prices – Prices & Portfolio – February 2014

Exhibit 3: Covidien & The Retail Prices – Portfolio & Cash Flow Summary – February 2014

Covidien & The Retail Prices – Portfolio & Cash Flow Summary – February 2014

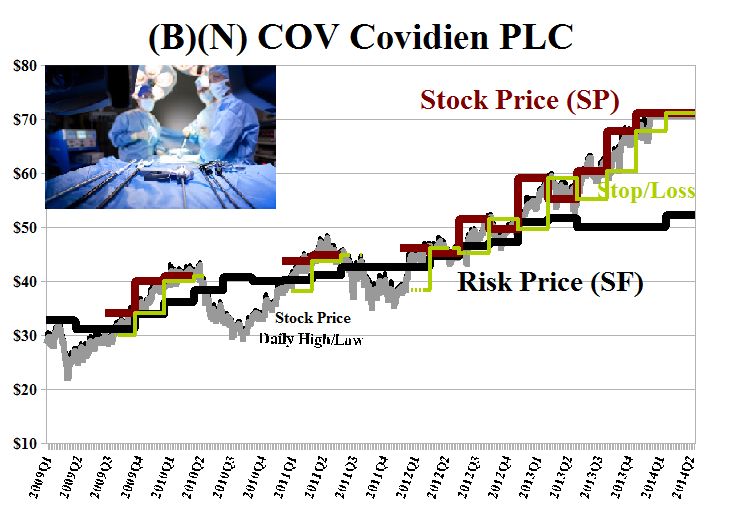

Exhibit 4: (B)(N) Covidien PLC – Risk Price Chart

(B)(N) Covidien PLC – Risk Price Chart – February 2014

Covidien PLC is engaged in the development, manufacture and sale of healthcare products for use in clinical and home settings. It operates its businesses through three segments: Medical Devices and Medical Supplies.

(Please Click on the Chart to make it larger if required.)

From the Company: Covidien plc develops, manufactures, and sells healthcare products for use in clinical and home settings worldwide. The companys Medical Devices segment develops, manufactures, and sells endomechanical instruments, such as laparoscopic instruments, surgical staplers, and interventional lung solutions; energy devices, including vessel sealing, electrosurgical, and ablation products and related capital equipment; and soft tissue repair products comprising sutures, mesh, biosurgery products, and hernia mechanical devices. This segment also offers vascular products, such as compression, dialysis, venous insufficiency, thrombectomy, neurovascular, and peripheral vascular products; oximetry and monitoring products, including sensors, monitors, and temperature management products; and airway and ventilation products comprising airway, ventilator, breathing systems, and inhalation therapy products. Its products are used primarily by hospitals and ambulatory care centers, as well as alternate site healthcare providers, such as physician offices. The companys Medical Supplies segment develops, manufactures, and distributes nursing care products comprising incontinence, wound care, enteral feeding, urology, and suction products; medical surgical products, such as operating room supply products related accessories, electrodes, thermometry, and chart paper product lines; SharpSafety products, including needles, syringes, and sharps disposal products; and original equipment manufacturer products. Its products are used primarily in hospitals, surgi-centers, and alternate care facilities, such as homecare and long-term care facilities. The company markets its products through direct sales force and third-party distributors. Covidien plc has 38,500 employees and is based in Dublin, Ireland.

For more information on the chart elements and additional references to the theory, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.