(B)(N) SVM Silvercorp Metals Incorporated

What is a “free good”?

Drama. “Since becoming a central banker, I have learned to mumble with great incoherence. If I seem unduly clear to you, you must have misunderstood what I said.” – attributed to Mr. Alan Greenspan speaking to a Senate Committee in 1987 (Guardian Weekly, November 4, 2005)

With that caveat in mind and the inherent incomprehensibility of anything that can be said in economics, we say that stocks that are trading at prices above the “price of risk” create an “economic free good” with the meaning that those prices have not been “earned” with the same integrity that the price of risk has been earned.

To say that “the price of risk has been earned” means (exactly) that our money invested in the purchase of the stock at that price, the price of risk, is as good as cash and better than “money” because there is reason to believe that the stock price and other values such as dividends, will tend to hold their value and might even increase in value at a rate that is no worse than the rate of inflation.

We are also entitled to say – that is, we can prove it – that a stock that is trading above the price of risk is “undervalued” with the meaning that there is “an excess of demand over supply” at that price because the investors who are willing to buy or hold the stock at prices above the price of risk have reason to believe that those prices will be earned and they are, therefore, reluctant to sell it at a lower price.

Maybe it’s just a valuation failure?

To which we must add the caveat emptor because there are many reasons that a stock may be driven to prices above the price of risk and “future value” as an unrealized “price of risk” might not have that much to do with it if all we have is “valuation” and “enthusiasm”.

We’ve had to confront this issue because Silvercorp Metals Incorporated suffered a “valuation failure” in 2011 and has never recovered and neither did the Sino-Forest Corporation in 2012 (Reuters, December 19, 2013, Silvercorp short seller accused of fraud by Canadian regulator and The Financial Post, December 5, 2013, OSC hearing to test fraud allegations against Sino-Forest delayed).

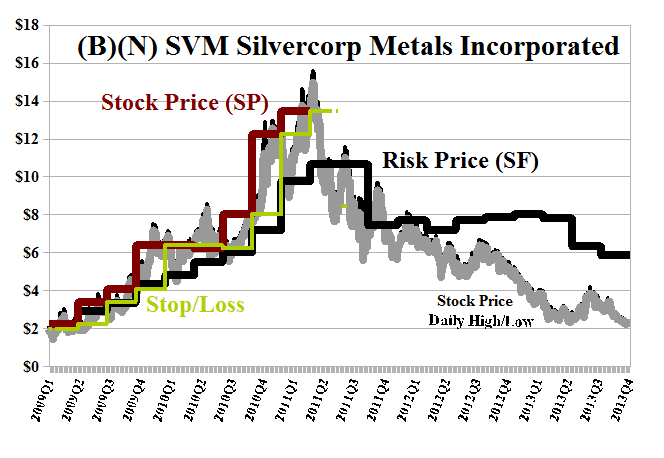

However, by simply knowing and respecting the price of risk, we were able to buy and hold Silvercorp Metals between $2 in 2009 and $13.50 in early 2011, but were stopped out by the alleged “valuation failure” and did not pray for a better outcome as many investors did as the market value of the company plunged from $2.3 billion to $1.5 billion three months later to $1 billion in early 2012 and the current $500 million.

Exhibit 1: (B)(N) SVM Silvercorp Metals Incorporated – Risk Price Chart

(B)(N) SVM Silvercorp Metals Incorporated

Investors who did not know the “price of risk” learned that the “cost of risk” was $1.8 billion or more than three times the current “market value” of the company.

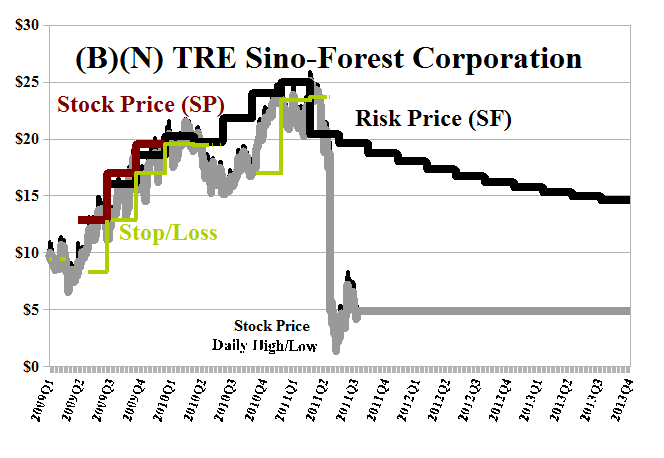

Similarly (with reference to the Exhibit below) in the case of Sino-Forest but the “cost of risk” was higher at $5 billion.

(B)(N) TRE Sino-Forest Corporation

The price of risk continues to decline simply respecting the current nominal $5 stock price even though the company is not trading.

However, based on what we know, an investor who buys the stock at $5 should have a reason to believe that the stock is “worth” $15 at the present time if, for example, the “valuation failure” turns out not to be correct.

From the last published balance sheet, the company has total assets of $6 billion, debt of $2.5 billion and a shareholders equity of $3.5 billion with 250 million common shares outstanding that traded at $25 and then, $5.

For more information and additional references to the theory, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.