(B)(N) IPO Investment Mechanics@RiskWerk

Deal Book. Institutional investors are lining up to buy the Twitter IPO this week and the deal should close tomorrow at which point everybody goes home and the stock is free floating in investor portfolios (Reuters, November 5, 2013, Twitter boosts IPO range amid strong investor demand).

Bottom Of The Food Chain

The math is compelling. The demand is such that the offering price has floated upwards to between $23 and $25 per share and the expectation is that all 70 million shares will be placed as well as an additional 10.5 million shares that are available in the overallotment granted to the underwriters and their brokers who do not pay the full price but get it at a discount in addition to their usual fees which are typically 10% to 15% of the deal (apparently $300 million or more in $2 billion).

The institutional investors – who would mostly be mutual funds and ETFs – are also happy because they will be able to charge a management fee, can tweet everybody that they have it, and have successfully passed on the risk to the fund owners which is we, the hapless investors at the bottom of the food chain.

Exhibit 1: (B)(N) Company “A” – Risk Price Chart

We don’t have any reason to think that the stock price of Twitter will in any way resemble the stock price experience of Company “A” over there, on the right.

But Company “A” also started at $25 or so, raised $2 billion, and had a similar command of well-regarded investment bankers, broker/dealers and investment analysts.

And it had a good, or at least colourful and plausible idea, but failed to convert that into earnings and dividends. It’s now selling for less than a dollar and the debt is more than twice as big as the shareholders equity. It could be bought for a song, so to speak, by somebody who has some money and an idea on how the company might make some money.

The “price of risk” for an IPO is the IPO price because that price should meet the standard of “the least stock price at which the company is likeable” (Goetze 2006) – we expect that our money will be safe – 100% capital safety – and that we might receive a hopeful but not necessarily guaranteed return above the rate of inflation.

In many cases the investment banks will intervene to ensure that until their inventory, if any, has been sold off. Nevertheless, we always wait to see what the market says and we’d also like to see a few more balance sheets in real time.

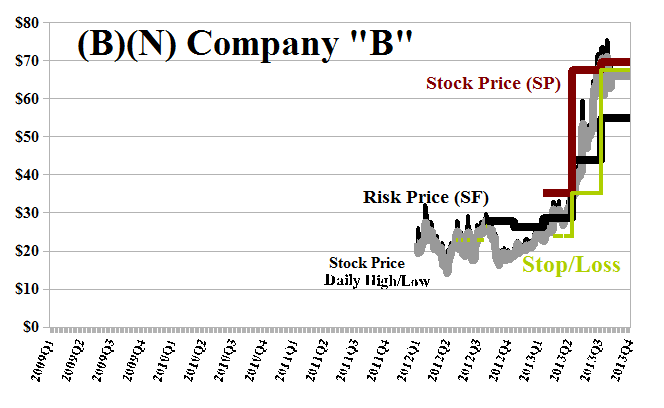

What investors really have in mind – especially if they’re queuing up to buy the stock – is more like Company “B” in Exhibit 2 below.

Exhibit 2: (B)(N) Company “B” – Risk Price Chart

(B)(N) Company “B”

The stock price “bobbled” a little once the IPO excitement died down, and after a while the company began to produce some earnings but did not pay a dividend because it fancied that the money was better in their hands than our pockets, and if we needed money, we could sell some of the stock.

We didn’t buy in until the price of risk was confirmed by a general interest. After all, we can’t sell the stock at a higher price unless there is such a buyer and we won’t sell the stock unless we need money, want to take some profits, or are stopped out on volatility in which case we might buy it back at a lower price but still above the price of risk. By that time, there would also be an options market and we can buy puts from our profits to protect our prices for the rest.

MAUs Are “The New Earnings”

Courtesy: SEC Form S-1 Twitter

At the present time, Twitter is likely to be in the “bobble phase” but $1.4 billion (estimated net after paying off some debts) won’t last long while they’re losing $150 million per year on 220 million active users with a growth projection that looks more like an “expense” than profit at the present time.

And IBM is also wondering about the status of some of its patents in this matter (Reuters, November 4, 2013, In patent showdown, IBM’s arsenal dwarfs Twitter’s).

We also note that the investment bankers and broker/dealers who are sponsoring the issue aren’t taking any risks which we don’t begrudge them because neither are we. (N)@RiskWerk.

For more information on the Chart elements and additional references, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.