(B)(N) The American Food Group

Drama. The Kellogg Company surprised investors with an announcement that it’s preparing for lower sales and tighter margins and that it’s planning to trim its workforce by 7% over the next several years (The Associated Press, November 4, 2013, Kellogg plans to trim 7 per cent of workforce as part of cost-cutting program). The profits on morning foods and snacks appear to be paper-thin (please see Exhibit 1 below) and it’s possible that we have reached a point of saturation – too much food, too much variety, too much competition for either a limited budget (sales) or an unlimited diet (variety and taste) that doesn’t sell well abroad and is a problem at home.

The Morning Food

For example, the entire industry earned profits (before taxes) of $5.3 billion in the past year which is about 1/20th of the profits returned by “Big Oil” – deemed a “scarce” resource with limited “variety” and “taste” – and only half the rate when compared to the assets at work or the shareholders equity.

And the results do not compare well with the international experience of just two companies, Nestlé SA and Danone, which combined are as large as all seven of the American group and compete in the same markets and supermarkets. Please see Exhibit 2 and 3 below.

Exhibit 1: The American Food Group – Fundamentals – November 2013

The American Food Group – Fundamentals – November 2013

Exhibit 2: Big Oil Fundamentals – November 2013

Big Oil Fundamentals

Exhibit 3: International – Fundamentals – November 2013

International – Fundamentals – November 2013

(Please Click on the Chart to make it larger if required.)

International Markets Might Be Different

We also need to consider that the Kellogg’s Company has been in business for more than 100 years and it’s possible that there might be more belt-tightening in the industry in respect of international markets which, quite naturally, do not have an open door with respect to food products (The Globe and Mail, October 18, 2013, Canada, EU unveil ‘historic’ free-trade agreement).

All of the companies have been eligible for the Perpetual Bond™ this year – limiting our discretion to Conagra Foods which dropped out in July on “surprise” (please see below) – and the portfolio return of +34% (plus dividends) was obtained by prudently leveraging the investment with the margin account and our usual stop/loss or bought puts in place. Simply buying and holding all the companies gave the market return of +24%. Please see Exhibit 4, 5 and 6 below.

Exhibit 4: (B)(N) The American Food Group – Prices & Portfolio – November 2013

The American Food Group – Prices & Portfolio – November 2013

Exhibit 5: (B)(N) The American Food Group – Portfolio & Cash Flow Summary – November 2013

The American Food Group – Portfolio & Cash Flow Summary – November 2013

(Please Click on the Chart to make it larger and again if required.)

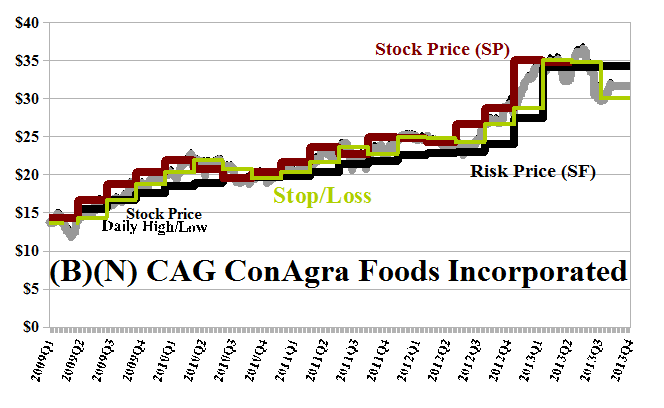

ConAgra Foods Incorporated has been in the Perpetual Bond™ continuously since much lower prices of $15 in 2009 but had a number of problems earlier this year of which failing profits on increased sales was only one (Omaha World-Herald, September 20, 2013, ConAgra reports 46% drop in quarterly profit).

The company will pay a dividend of $422 million to its shareholders this year for a current yield of 3.1% but our estimate of the downside risk in the stock price due to the demonstrated volatility is still minus ($2.50) per share and it’s trading below the price of risk at the present time.

Exhibit 6: (B)(N) CAG ConAgra Foods Incorporated – Risk Price Chart

(B)(N) CAG ConAgra Foods Limited

ConAgra Foods Incorporated is a packaged food company, supplying frozen potato and sweet potato products, as well as other vegetable, spice, and grain products to a variety of restaurants, food service operators and commercial customers.

(Please Click on the Chart to make it larger if required.)

From the Company: ConAgra Foods Incorporated operates as a food company primarily in North America. The company operates through four segments: Consumer Foods, Commercial Foods, Ralcorp Food Group, and Ralcorp Frozen Bakery Products. The Consumer Foods segment provides branded, private brand, and customized food products in various categories, such as meals, entrées, condiments, sides, snacks, and desserts, which are sold in various retail and foodservice channels. This segments principal brands include Alexia, ACT II, Banquet, Blue Bonnet, Chef Boyardee, DAVID, Egg Beaters, Healthy Choice, Hebrew National, Hunts, Marie Callenders, Odoms Tennessee Pride, Orville Redenbachers, PAM, Peter Pan, Reddi-wip, Slim Jim, Snack Pack, Swiss Miss, Van Camps, and Wesson. The Commercial Foods segment offers commercially branded foods and ingredients that are sold primarily to foodservice, food manufacturing, and industrial customers. It provides specialty potato products, milled grain ingredients, vegetable products, seasonings, blends, and flavors under the ConAgra Mills, Lamb Weston, and Spicetec Flavors & Seasonings brand names. The Ralcorp Food Group segment principally offers private brand food products that are sold in various retail and foodservice channels. Its products consist of cereal products; snacks, sauces, and spreads; and pasta. The Ralcorp Frozen Bakery Products segment primarily offers private brand frozen bakery products that are sold in various retail and foodservice channels. This segment’s primary products comprise frozen griddle products, including pancakes, waffles, and French toast; frozen biscuits and other frozen pre-baked products, such as breads and rolls; and frozen and refrigerated dough products. ConAgra Foods, Inc. was founded in 1919, has 35,000 employees and is headquartered in Omaha, Nebraska.

For more information on the Chart elements and additional references, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.