The S&P TSX “Patient Money” Portfolio

Drama. The investment firm, Raymond James, has suggested that the SNC-Lavalin Group might be a buying opportunity for “patient money” because the stock price is low ($40 today and down from $60 two years ago), the dividend yield is about 2.3%, and it seems to be overcoming many of its recent problems (The Canadian Press, August 27, 2013, SNC-Lavalin’s low share price buying opportunity for patient investors: analysts).

Moreover, the analyst points out that SNC-Lavalin has a thriving infrastructure and concessions business with investments in such “assets” as Toronto’s Highway 407 toll road, the AltaLink transmission lines in Alberta, and the Montreal super hospital, which (he thinks) should limit a further slide in the stock price sufficiently that “patient investors will be amply rewarded for buying it at current levels” (ibid, The Canadian Press, notwithstanding the past, Quebec Bureau, December 19, 2012, Montreal’s super hospital suffering from deficit, scandals).

Despite all of that, other analysts both agree and disagree but are basically of the opinion that it is “simply not tenable” that SNC-Lavalin’s shares continue trading at a substantial discount to its peers and that “nothing lasts forever, even the bad times” (ibid, The Canadian Press).

The Cheque

(-5%) This Year

Indeed, but before we reach for our chequebook, we need to consider that nothing that the company has done, left undone, or not done, or owns, in the past year (and even two years) has been able to drive the stock price convincingly above the price of risk (please see Exhibit 1 below).

And that in the S&P TSX portfolio of companies, there are currently more than fifty companies with market values in excess of $2 billion that are similarly challenged, and trading below their price of risk, and their aggregate return (before dividends) is minus (-5%) so far this year (please see Exhibit 2 and 3 below).

The Fruits

+50% This Year

Which return can be fruitfully compared to a simple buy and hold portfolio of forty companies that are in the Perpetual Bond™ and have returned a staggering +50% (plus dividends) so far this year, and will not return less than that for the rest of it (with reasonable care).

And this portfolio is obviously patient, but not in need of yet further convalescence.

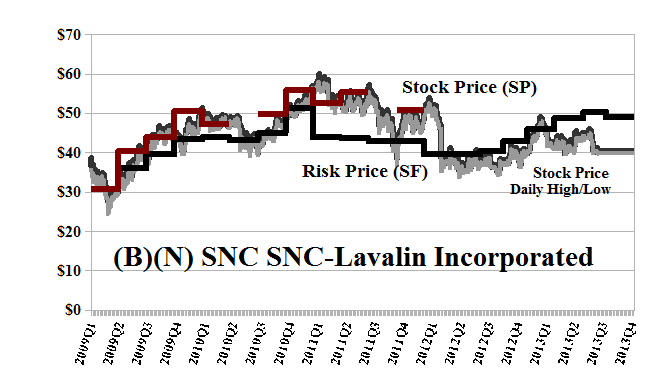

Exhibit 1: (B)(N) SNC-Lavalin Group Incorporated – Risk Price Chart

(B)(N) SNC SNC-Lavalin Group Incorporated – August 2013

SNC-Lavalin Group is an engineering and construction group and a major player in the ownership of infrastructure, and in the provision of operations and maintenance services.

(Please Click on the Chart to make it larger if required.)

The stock is trading today at $40 but has a downside of minus ($4) per share due to the demonstrated volatility. We would neither be surprised nor grateful for any price between $36 and $44, and it’s trading below the current Risk Price (SF) of $46 in the “trading zone of investor uncertainty“.

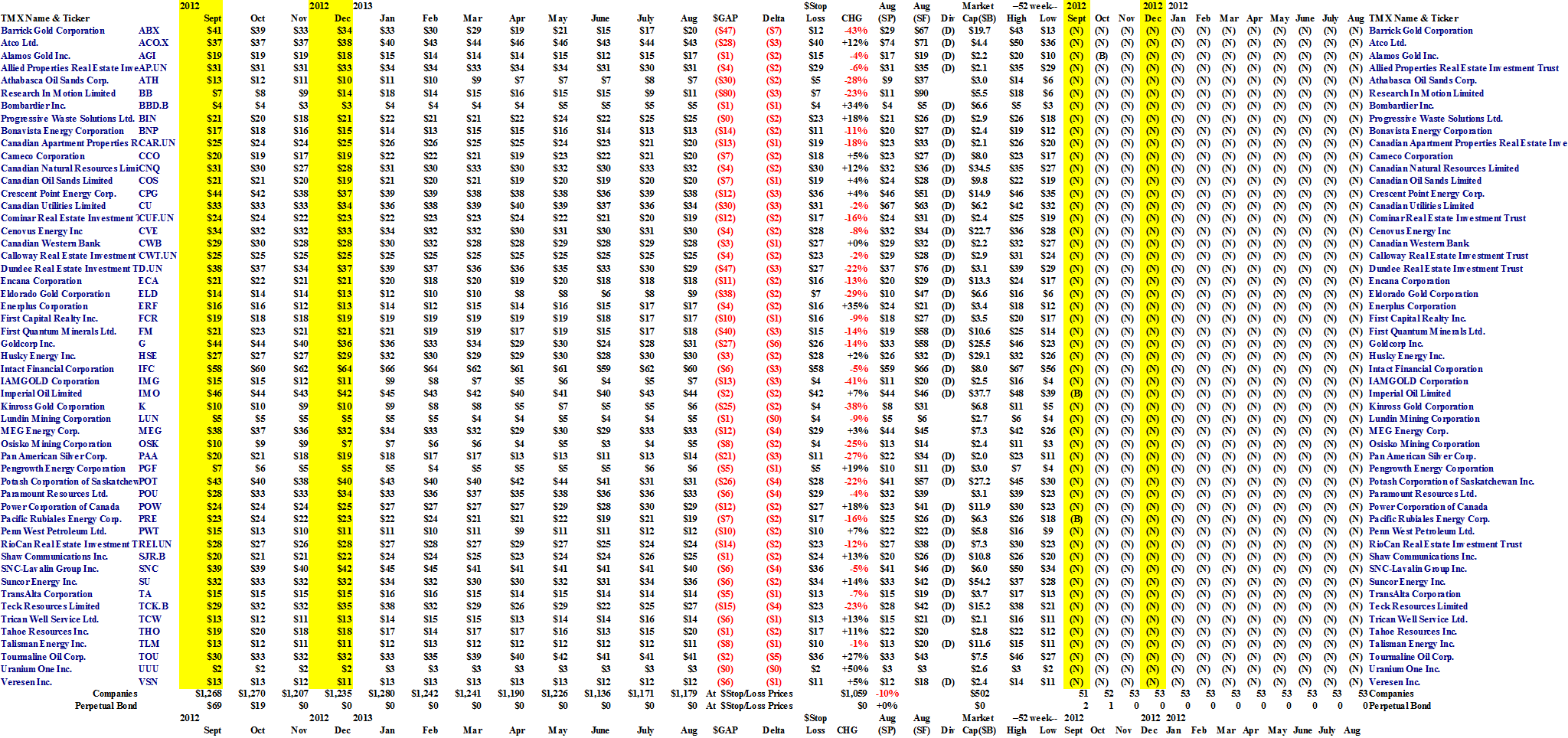

Exhibit 2 below is our standard “Cash Flow” summary for portfolio investments. In this, case, there is nothing in the Perpetual Bond™ other than a few companies that we bought and sold late last year, leaving $238,000 in the Cash account. However, the Companies line buys all the eligible companies on the same basis, and all fifty-three of them (in blocks of 1,000 shares each at a current market price) cost $1,235,000 in December and is worth $1,179,000 today for a loss of (-5%). And we didn’t have to do anything.

We also note that if we continue to do nothing but patiently wait for the companies to trade above their stop/loss prices (please see Exhibit 3 below), we could still lose another minus (-10%) should something “bad” happen to the entire market.

Of course, nothing bad will last forever – we’ll just get used to it.

Exhibit 2: S&P TSX “Patient Money” Portfolio – Cashflow – August 2013

(Please Click on the Chart to make it larger if required.)

Exhibit 3: S&P TSX “Patient Money” Portfolio – Portfolio – August 2013

(Please Click on the Chart to make it larger and again if required.)

To see what else real risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.