On Golden Pond

Drama. The Canadian government has developed a number of “savings plans” to help workers and their families save for the necessities of life, including education and retirement, emergencies, or buying a home. There are three of them: the Tax Free Savings Account (TFSA), the Registered Retirement Savings Plan (RRSP), and the Registered Education Savings Plan (RESP), each of which helps savers to accumulate money (“savings”) and invest them for tax exempt or tax-deferred investment gains in capital gains (or losses), interest, and dividends.

We want 100% Capital Safety and Non-negative Real Returns

Courtesy: Ernest Thompson, Author

Any bank will set one up for us, and provide valuable tax advice, almost for free, but then proceed to abuse our trust and confidence in them by providing “investment advice” for which their advisers are not qualified unless they are prepared and instructed to recommend only one kind of investment: the capital (our “savings”) must be 100% safe and we should hope to obtain a hopeful but not necessarily guaranteed return above the rate of inflation.

Anything else is just a gamble – and they say that too – and there are casinos for that with provable odds, of which the stock market is not one.

However, there are only a few such investments: they are GICs (which will provide a non-negative return but not necessarily a non-negative real return) and Real Return Bonds (RRBs) which will provide a non-negative real return, but there are no such investments in the equity markets that provably provide both 100% capital safety and a hopeful but not guaranteed return above the rate of inflation, other than the Perpetual Bond™ which is managed by The RiskWerk Company and not by the banks or any of their mutual or segregated funds.

The RiskWerk Company

“Doing It On Our Own”

But, we are The RiskWerk Company, and we can do it on our own and the simplest is the TFSA which can be topped up to $25,000 this year and there is a scheduled increase that the government plans for future years.

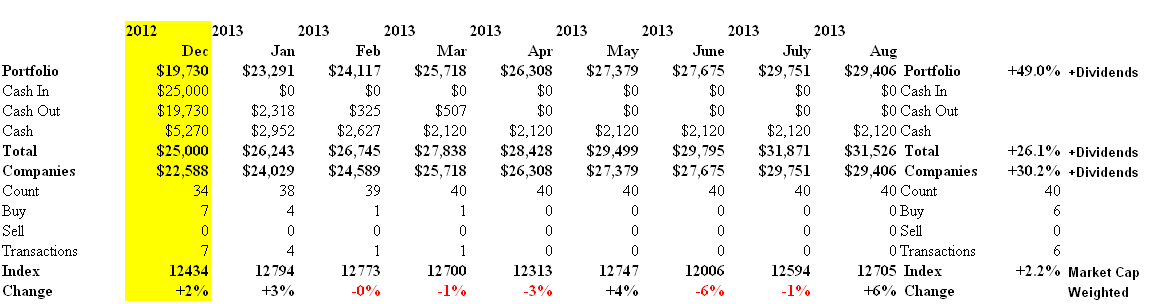

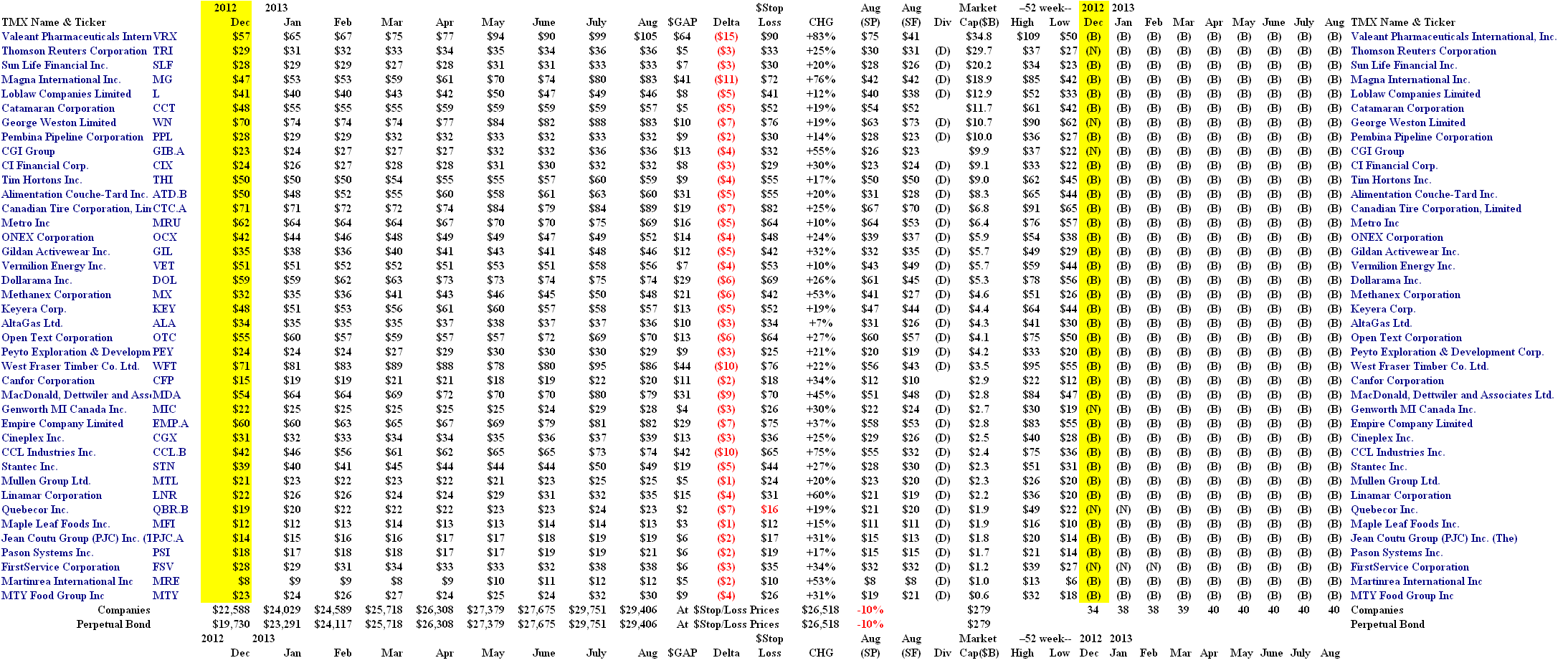

In January, we just bought 15 shares (respecting our budget constraint) at the market price in each of the thirty-four large capitalization, mostly dividend paying stocks, that were in the Perpetual Bond™ at least since September 2012. Please see Exhibit 1 and 2 below.

That cost $19,730 and we still had $5,270 in the cash account for additional purchases (which we did in January, February and March) but have done nothing since except set the stop/loss, collect our dividends, and pay a few transaction costs (less than $400 for the forty purchases, but there’s not been any reason to sell anything, as yet).

The portfolio – for which we did next to nothing – is up nearly +50% so far this year (please see the Portfolio line in Exhibit 1) and the account (Total line) is up +26%, only, because of the idle cash.

Moreover, unless we want to invest some more of our idle cash in additional stock, or buy more of what we have, we’re not going to do anything until next January except keep an eye on the stop/loss levels (please see Exhibit 2 below) as the stock prices increase or there are forced sales due to the stop/loss.

Exhibit 1: S&P TSX “On Golden Pond” TFSA – Cash Flow Summary

S&P TSX On Golden Pond – Cash Flow

(Please Click on the Chart to make it larger if required.)

Exhibit 2: S&P TSX “On Golden Pond” TFSA – Portfolio Summary

S&P TSX On Golden Pond – Portfolio

(Please Click on the Chart to make it larger and again if required.)

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.