(B)(N) Bear Droppings in U.S. Silica & the Blue Nile

Deal Book. We’ve recently heard that grizzly bears (Ursus arctos or brown bears) will attack, kill and eat their distant cousins, the black bears (Ursus americanus), and it’s not always about food – that is, money and we’ll use the terms “money” and “food” interchangeably – absent a “famine”, but more commonly about territory or power and, again, “territory” and “power” are synonomous, as has been the case historically.

Grizzly Bear and Black Bear Throw down

Courtesy: Calgary Sun

We’re minded of this because the “grizzled” veterans and fabled titans of Wall Street, Mr. Soros and Mr. Icahn, and their allies, appear to be in a deadly embrace with the new generation of emerging “titan wannabes” such as Mr. Ackman and Mr. Cohen, and their acolytes, by alternately taking long and short positions in the same family of stocks of which there are only a few, and betting hundreds of millions of dollars, and even billions, on the outcome.

Obviously, it helps the cause to be famous or infamous or renowned, and where there might have been a mere hint of an opportunity for arbitrage, bringing in the bets from the sidelines will help their cause (CNBC, August 15, 2013, Carl Icahn takes a shot at Bill Ackman…again).

But the new money that’s parked and undecided, is not ours. We’re usually already there, and if the company is in the Perpetual Bond™, then it’s there for reasons that have nothing to do with the “noisy rumblings in the bush”, so to speak, which serve only to provide us with new opportunities to pillage the titans and harass the newcomers who want to buy (or sell, by shorting) our stock.

The case of the long position is obvious because the new money and new buyers are going to chase what we already have if it’s in the Perpetual Bond™. But if it’s not, it might also push companies that are in the Contra Portfolio (N) into prices that are trading at or above the price of risk, and, in that case, we might buy in if we’re confident that we can enforce our usual price protections, or we might buy call options if we recognize the move early, and its cause, and make a killing of a different sort.

Herbalife is a good example of the short position and we made money, first from the “black bears” on their enormous short position, and now from the “brown bears” on their enormous long position. Please set our recent Post for an update.

The Street is also in tune with this and has reviewed the second quarter SEC Schedule 13F and 13D filings to identify three old cases, Herbalife, J.C. Penney, and Chesapeake Energy (which has found its way to $26 from $20 this year), and two new cases, US Silica Holdings Incorporated and Blue Nile Incorporated (TheStreet, August 22, 2013, 5 Heavily Shorted Stocks That Hedge Funds Love). Please see Exhibit 1 and 2 below.

Neither of these two companies is very large by S&P 500 standards; US Silica has a market capitalization of $1.2 billion at the current 53 million common shares and stock price of $24, but the float is only 35 million shares since the company is a wholly-owned subsidiary of the privately owned GGC USS Holdings LLC, which has revenues of about $40 million a year, in contrast to US Silica which has revenues of about $440 million per year and pays a total dividend of $27 million per year for a current yield of 2.2%.

Blue Nile is even smaller with a market capitalization of $460 million at $38 and 12 million shares outstanding; Blue Nile does not pay a dividend but has revenues of about $400 million per year.

However, the short interest in US Silica is estimated to be 40% of the float (ibid, TheStreet), or 14 million shares which would be valued at $336 million at $24 per share; and the short interest in Blue Nile is estimated to be 18% of the common shares outstanding, or 2.2 million shares worth $82 million at $38 per share. And every $1 increase in the price of the stocks (both of them) adds $16 million to that total deficiency from the point of view of the short sellers who might need to cover their shorts at any time.

And for that, they might need to talk to Mr. Steve Cohen, founder of the hedge fund SAC Capital Advisors (The New York Times, August 25, 2013, SAC Capital Is Indicted, and Called a Magnet for Cheating) who could buy both companies with his chequebook, but has instead taken the long position of owning about 2.1 million shares of US Silica (6% of the float) and 670,000 shares of Blue Nile (5% of the common shares outstanding).

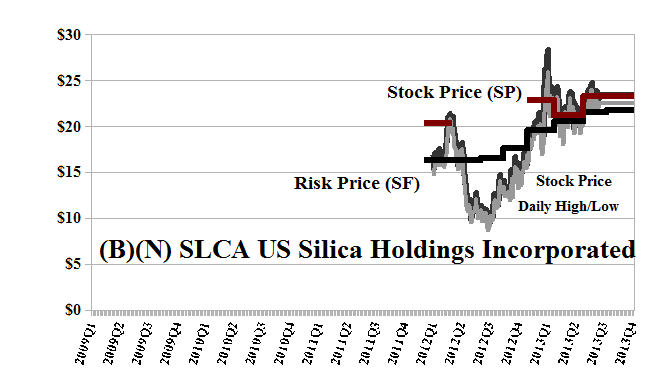

Exhibit 1: (B)(N) SLCA US Silica Holdings Incorporated – Risk Price Chart

(B)(N) SLCA US Silica Holdings Incorporated

US Silica is trading above the current Risk Price (SF) of $22 but our estimate of the downside due to the demonstrated volatility is minus ($4) per share.

(Please Click on the Chart to make it larger if required.)

Although we could buy the stock at $24 and a collar for about $0.50 per share that would protect the price between $22.50 and $25 for the next month, it’s hardly worth doing the trade with the call in place.

Absent the call, we could buy the stock for $24, buy the put for $0.80, collect our dividends, and hope that the price rises to at least $25 in the next month.

From the Company: U.S. Silica Holdings Incorporated, together with its subsidiaries, engages in the mining, processing, and sale of commercial silica in the United States. It operates in two segments, Oil & Gas Proppants and Industrial & Specialty Products. The company offers whole grain commercial silica products to be used as fracturing sand in connection with oil and natural gas recovery, as well as in various size distributions, grain shapes, and chemical purity levels for manufacturing glass products. It also provides ground commercial silica products for use in plastics, rubber, polishes, cleansers, paints, glazes, textile fiberglass, and precision castings; and fine ground silica for use in premium paints, specialty coatings, sealants, silicone rubber, and epoxies. In addition, the company offers other industrial mineral products, such as aplite, a mineral used to produce container glass and insulation fiberglass; calcined kaolin clay, a mineral primarily used as a functional extender in paints, plastics, specialty coatings, and rubber; and adsorbent made from a mixture of silica and magnesium for preparative and analytical chromatography applications. It serves oil and gas recovery markets, as well as various industries, including, container glass, fiberglass, specialty glass, flat glass, building products, fillers and extenders, foundry products, chemicals, recreation products, and filtration products. As of February 26, 2013, U.S. Silica Holdings, Inc. controlled approximately 307 million tons of proven and probable recoverable mineral reserves. The company was formerly known as GGC USS Holdings, Inc. and changed its name to U.S. Silica Holdings, Inc. in July 2011. The company is headquartered in Frederick, Maryland, has 800 employees, and is a subsidiary of GGC USS Holdings, LLC

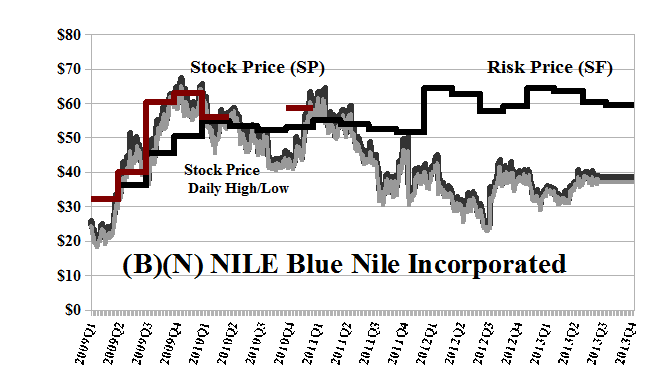

Exhibit 2: (B)(N) NILE Blue Nile Incorporated – Risk Price Chart

(B)(N) NILE Blue Nile Incorporated

Blue Nile is trading at $40 and is $20 below the Risk Price (SF) of $60, and doesn’t pay a dividend. Although the stones are beautiful, the stock would need a takeover price to work out as an investment.

(Please Click on the Chart to make it larger if required.)

From the Company: Blue Nile Incorporated operates as an online retailer of diamonds and fine jewelry worldwide. The company offers various engagement products, including gold or platinum engagement rings with a diamond center stone and loose diamonds; and non-engagement products, such as rings, wedding bands, earrings, necklaces, pendants, and bracelets, as well as gifts and accessories with precious metals, diamonds, gemstones, or pearls. Blue Nile Incorporated sells its products through the Web sites bluenile.com, bluenile.ca, and bluenile.co.uk. The company was formerly known as Internet Diamonds, Inc. and changed its name to Blue Nile Incorporated in November 1999. Blue Nile Incorporated was founded in 1999, has 240 employees, and is headquartered in Seattle, Washington.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.