(B)(N) CLR Continental Resources Incorporated

Deal Book. Continental Resources, and its Chairman, Mr. Harold Hamm, are credited with discovering the enormous Bakken oil field in North Dakota , which now stretches into Montana, and also with developing the technology, including horizontal drilling and “fracking”, to produce it.

The field currently produces about 700,000 barrels a day which is nearly 10% of America’s daily crude oil requirements and the field is estimated to contain at least 24 billion barrels of producible oil (Reuters, June 14, 2013, Special Report: Lack of a prenup imperils oil billionaire’s fortune)

Courtesy: Continental Resources Incorporated Horizontal Drilling

The company is publicly traded and has 186 million shares outstanding at $86 per share for a current “market value” of $16 billion, which is where we have a “problem”.

Why does it have any “value” at all?

We ask the question because the company is at least 2/3rds owned by Mr. Hamm and doesn’t pay a dividend; institutional ownership is minor at about 20% in total and no institution owns more than 4% at the present time.

Why would Mr. Hamm not buy in the rest of the stock and become a private company to which he has access to all the cash flows?

For example, the revenue has more than tripled since 2008 and 2009 and is currently $2.4 billion per year, and last year the net income after tax was $740 million or $4 per share, up from $0.40 per share in 2009 and $1.00 per share in 2010.

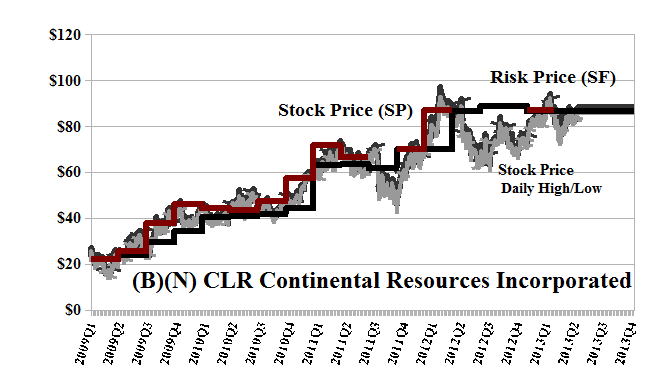

All of that has been diligently recorded in the stock price for a company that has only a 30% float, if that. Please see Exhibit 1 below. And the point is not moot because the ownership structure of the company could change as a result of Court orders (ibid, Reuters).

Moreover, it would be easy to drive down the price of the stock simply by failing to produce earnings per share, which belong mostly to Mr. Hamm, in any case, and, after all, oil is just a commodity and worse has happened to gold, silver, copper, and so forth.

The company was in the Perpetual Bond™ between $20 and $70 between 2009 and 2011 – please see Exhibit 1; Red Line Stock Price (SP) above the Black Line Risk Price (SF) and for no other reason – and is eligible for the Perpetual Bond™ again at the current $86 just brushing up against the Risk Price (SF) which is also $86 at the present time.

Our estimate of the downside in the stock price due to the demonstrated volatility is minus ($8) per share so that the stock could be trading at between $78 and $94 without surprise. However, surprise is in the air, and we don’t like “surprises”. In our view, a long dated put might be a better buy, and one wonders which hedge fund might “short” the stock by “borrowing” some of the stock from the institutions that own 20% it and, thereby, getting some “rent” in lieu of dividends?

Exhibit 1: (B)(N) CLR Continental Resources Incorporated – Risk Price Chart

(B)(N) CLR Continental Resources Incorporated

Continental Resources Incorporated is a crude oil and natural gas exploration and production company with operations in the North, South and East regions of the United States.

(Please Click on the Chart to make it larger if required.)

From the Company: Continental Resources Incorporated engages in the exploration, development, and production of crude oil and natural gas properties in the north, south, and east regions of the United States. The company sells its crude oil production to end users, as well as to midstream marketing companies or oil refining companies at the lease. As of December 31, 2012, its estimated proved reserves were 784.7 one million barrels of crude oil equivalent, with estimated proved developed reserves of 317.8 one million barrels of crude oil equivalent. Continental Resources, Inc. was founded in 1967, has 800 employees, and is headquartered in Oklahoma City, Oklahoma.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2006) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks. Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.Disclaimer Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.