(B)(N) WFC Wells Fargo & Company

Drama. Analysts have been wondering what to do about Wells Fargo (The Street, June 14, 2013, Wells Fargo Slips as Analysts Disagree). Well, it’s elementary – we buy it and hold it and collect our dividend of $0.30 per share per quarter of which the company expects to pay $6.4 billion this year to the shareholders for a current yield of 3%.

Courtesy: The Wells Fargo Bank

We don’t know, for example, how “the operating and regulatory environment [which is clearly challenging], revenue diversity and credit/expense leverage should allow the company to grow EPS going forward” (ibid, The Street) will affect the stock price, although the analyst suggests $42 to $44.

If we look more closely at the facts, we might know more?

We don’t know if “WFC’s outlook [which remains constructive], particularly expense leverage tied to the company’s efficiency initiative and legacy servicing/mortgage-related costs, [but] earnings growth is clearly moderating into ’14” (ibid, The Street) will affect the stock price, although the analyst concludes that $42 is about right.

Indeed, WFC’s “evaluation” (10.5×earnings) is higher than the other “Big Six” banks, which have tended to be between 9.2×earnings and 10.8×earnings, but we don’t know whether that is due to the deemed pivotal “return on average tangible common equity (ROTCE)” which was 16.72% (ibid, The Street) in contrast to the other guys for which the ROTCE has been all over the place, from the single digits to the double digits even for the same company (ibid, The Street), and they still have a stock price.

Undoubtedly, there will be other challenges for the company this year and next, but, fortunately, there is a management there that has demonstrated an ability to deal with the challenges in the past. That’s why we pay them $3 million to $6 million a year, plus whatever else.

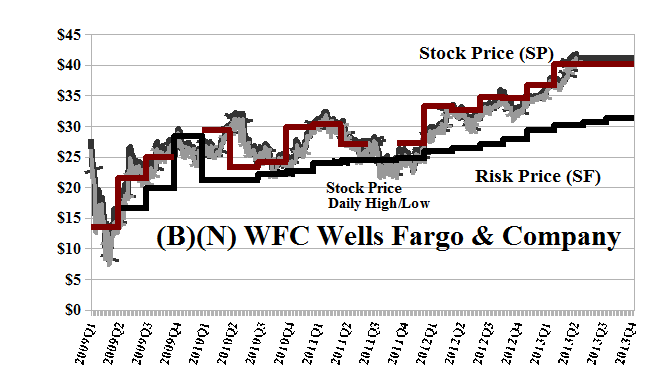

And we do know that the company has been trading at or above the price of risk for quite some time and that it was already eligible for inclusion in the Perpetual Bond™ at $25 two years ago, and is still in the Perpetual Bond™ at $40 today, and will continue to be eligible at any price above the current Risk Price (SF) of $32 and rising. Please see Exhibit 1 below; Red Line Stock Price (SP) above the Black Line Risk Price (SF) and for no other reason.

We also know that the price of risk is the “least stock price at which the company is likeable” and that portfolios of “likeable” companies have the property that their value, in aggregate, is “as good as cash” and “better than money”; in other words, such a portfolio of stocks is an investment and one should hang on to them, absent a “surprise” that none of us knows anything about. That’s why it would be a “surprise”.

To avoid “surprises”, we note that the demonstrated volatility in the stock price is minus ($2.50) so that the stock could be trading anywhere between the current $40 and $38 to $42 without surprise. We can certainly afford the stop/loss at $38 but then we would only have to buy it back at lower prices, if still above the price of risk. Pity. More good money into an investment.

Exhibit 1: (B)(N) WFC Wells Fargo & Company – Risk Price Chart

(B)(N) WFC Wells Fargo & Company

Wells Fargo & Company provides financial services through subsidiaries engaged in various businesses, mainly: wholesale banking, mortgage banking, consumer finance, equipment leasing, agricultural finance, commercial finance etc.

(Please Click on the Chart to make it larger if required.)

From the Company: Wells Fargo & Company provides retail, commercial, and corporate banking services. The company’s Community Banking segment offers deposits, such as checking accounts, savings deposits, market rate accounts, individual retirement accounts, time deposits, and debit cards; and loan products, including lines of credit, auto floor plan lines, equity lines and loans, equipment and transportation loans, education loans, residential mortgage loans, and credit cards. This segment also provides equipment leases, real estate and other commercial financing, small business administration financing, venture capital financing, cash management, payroll services, retirement plans, health savings accounts, credit cards, merchant payment processing, and private label financing solutions, as well as purchases retail installment contracts. Its Wholesale Banking segment offers commercial loans and lines of credit, letters of credit, asset-based lending, equipment leasing, international trade facilities, trade financing, collection services, foreign exchange, treasury management, investment management, institutional fixed-income sales, interest rate, commodity and equity risk management, online/electronic products, and investment banking services. This segment also provides construction loans, land acquisition and development loans, secured and unsecured lines of credit, interim financing arrangements, rehabilitation loans, affordable housing loans and letters of credit, permanent loans for securitization, commercial real estate loan servicing, and real estate and mortgage brokerage services. The company’s Wealth, Brokerage, and Retirement segment offers financial advisory, wealth management, brokerage, retirement, trust, and reinsurance services. As of June 11, 2013, it provided services through approximately 9,000 stores, 12,000 ATMs, the Internet, and offices in approximately in 35 countries. The company was founded in 1852, has 275,000 employees, and is headquartered in San Francisco, California.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2006) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks. Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.Disclaimer Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.