Popoviciu’s Volatility

Tiberiu Popoviciu (1906-1975) was a Romanian mathematician who gave us an inequality for the variance (1935) that we use almost every day as a ball-park estimate of what we might expect as the downside of stock prices without having to watch them too closely – our brokers can do that for us because they are responsible for executing a timely stop-loss at market prices in case this is not a good day and possibly worse days are to follow.

The mechanism is not perfect because the stock price could drop significantly below the stop-loss price and keep on dropping before we get a new executable market price to effect the sale and the “Wall Street Put” (please see our Letter,The Wall Street Put, August 2012) is iron-clad when it comes to protecting our prices and gains but could – although not always – cost us a few cents or dollars per share. But that’s the price of options and absolute safety, isn’t it.

If X={x1, x2, …, xN) is a (numerous) basket of (positive) numbers purported to be the demonstrated stock prices (or returns) of a company (please see our Letter, Stock Prices Are The New Pink, June 2012 or Economics is Confusing, June 2012, for the reasons for our circumlocution and laborious precision – we’re in our mathematical mode today and pray that we have some friends who want to hear this) and M=Maximum(X) and m=Minimum(X), then

Variance(X) ≤ (M-m)²/4 (Popoviciu 1935).

As a rule of thumb, this result is rather easy to prove and it has nothing to do with statisics. We note that Var(X)=[Σ(xi-a)²]/N is a minimum for a=Avg(X)=Σxi/N (just differentiate the expression for Var(X) with respect to the variable (a)) and, hence, for any other such (a) which is a plausible measure of “location” in X such as a=(M+m)/2, where M=maximum(X) and m=minimum(X), we must have that the variance of X with respect to (a) is larger and, therefore,

Var(X) = Σ[(xi – Avg(X))²]/N

≤ [Σ(xi – (M+m)/2)²]/N

= [Σ [(xi-m) – (M-xi)]²]/4N

≤ [Σ [(xi-m) + (M-xi)]²]/4N (because xi-m ≥0 and M-xi≥0 for each i)

= [Σ[M-m]²]/4N = (M-m)²/4 which proves the result.

In practice, the downside is not measured by the volatility but usefully and more conservatively by the “standard deviation” which is the square root of the variance, δ(X) = √Var(X)≤(M-m)/2, and measures “distance” as opposed to “area” (more on this distinction below). In effect, if a=Avg(X)=Σxi/N or a=(M+m)/2 are our measures of “location” in (X), then δ(X) is a measure of the shortest “straight” paths from here to there within (X). If, in fact, we had any idea of what stock prices really are and how they are related, we could use a more general measure of “distance” (such as the tensors and metrics of General Relativity, perhaps).

However, we’re not done. For stock prices, the most commonly quoted maximums and minimums (other than daily) are the rolling 52-week maximums and minimums such as in Exhibit 1.

Exhibit 1: Dow Jones Industrial Companies – High and Low Prices

(Please Click on the Chart to make it larger if required.)

In the case of AA Alcoa Inc, for example, we see that the previous 52-week maximum is M=$12 and minimum m=$8 but that our bound for the downside (Delta column) is not $2=(12-8)/2 but $1. The reason for this is that the annual volatility is too long a range for us to be effective and we really don’t care about daily, weekly or even monthly volatility as long as we have a realistic stop-loss point to protect us against losses due to ambient (but possibly lasting for some time) market factors or volatility.

In order to calculate an estimate of the quarterly volatility (Delta in the table) we note that Var(X + Y) = Var(X) + Var(Y) + 2×Cov(X,Y) which is a formal algebraic result and has nothing to do with statistics. However, it is reasonable for us to assume that for the most part ambient market factors from quarter to quarter are more or less independent (orthogonal) so that Cov(X,Y) is a small number that we may take to be zero in comparison to Var(X) and Var(Y). Hence, Var(X+Y) ≈ Var(X) + Var(Y) and, therefore, δ(X+Y) ≈ √[δ(X) + δ(Y)] = √2 ×δ(X) if we assume (as we do) that the ambient volatility (not prices) is more or less the same. This result obviously extends to four consecutive (or any) quarters (periods X, Y, Z, W) making up the year with the result that δ(X+Y+Z+W) ≈ √4 × δ(X) = 2× δ(X) and our estimate of the quarterly volatility is, therefore, δ(X) = δ(X+Y+Z+W)/2 ≤ (M-m)/4. We also note that it doesn’t matter whether we consider X+Y or X-Y as representative of stock prices over successive quarters – the volatility will be the same regardless of their “location”.

We would not be mathematicians if we failed to mention an even stronger and beautiful result due to Rajendra Bhatia and Chandler Davis (1999):

Var(X) ≤ (M – Avg(X))×(Avg(X) – m) (Bhatia-Davis 1999)

which, of course, implies the Popoviciu result because if a=M-Avg(X) and b=Avg(X) – m, then ab ≤ (a+b)²/4 = (M-m)²/4. One might wonder that we’ve been calculating variances for one hundred and fifty years (since Carl Gauss 1777–1855 ) and no one seems to have noticed that the Bhatia-Davis “rectangle” is also location invariant.

To prove this result, we note that the “dispersion” defined by (M – Avg(X))×(Avg(X) – m) is a “rectangle” with sides (M-Avg(X)) and (Avg(X)-m) and that a typical point xi in X can be located on a line (which must include both of the points m and M)

[m………xi………avg………………M]

where avg=Avg(X), m≤ xi ≤M and xi could be located anywhere on the line (not just below the average). However, it’s evident that no matter where xi is located on the line, the “box” with sides (xi – avg) will have an area (xi – avg)² and if (a big “if” because it’s true in exactly and only one case) it were always true that the “box” was contained in the “rectangle” then (xi – avg)² ≤ R=(M-avg)(avg-m) and

var(X) = [ Σ(xi-avg)²]/N ≤ (ΣR)/N = (NR/N) = R.

But that is true (consider xi=M for some i if M-avg>avg-m or xi=m if m-avg>M-avg) if and only if the “rectangle” itself is a “box”, that is, the sides are of equal length, M-avg = avg-m, and hence, avg=(M+m)/2 which is again the Popoviciu case. On the other hand, if the “rectangle” is not a “box” and avg(X) ≠ (M+m)/2, then one would think that we have outliers or simply not enough observations to remove an “up” or “down” bias.

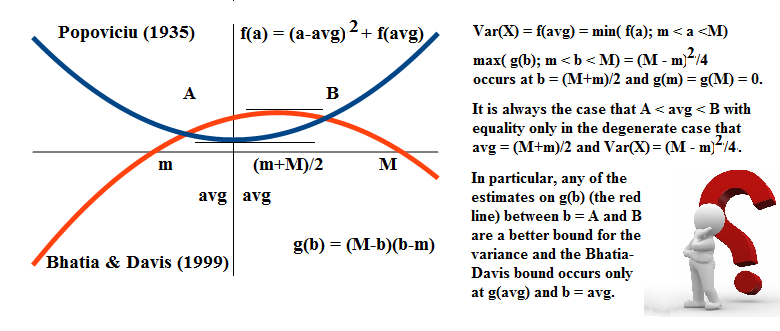

Nevertheless, these considerations provide us with an elementary proof of the Bhatia-Davis Inequality. We can define a “variance” in X with respect to any variable (a) as f(a) = Σ[xi – a]²/N = (a-avg)² + f(avg) where, by doing the algebra or just substituting a=avg, f(avg) = Var(X). Similarly, we can define a function g(b)=(M-b)(b-m) and we note that f(a) is a parabola opening upwards with a minimum point at a=avg and g(b) is also a parabola but it opens downwards with a maximum point at b=L=(M+m)/2. Moreover, f'(a) = 2(a-avg) and g'(b) = (M+m) – 2b = 2(L – b).

Because f(L) ≤ g(L) for L=(M+m)/2 (Popoviciu) there exists a unique

smallest A and a unique largest B such that f(a) ≤ g(a) for all A ≤ a ≤ B and in order to prove the Bhatia-Davis inequality, f(avg) ≤ g(avg), we need to show that A≤avg≤B.

However, for such A and B, f(A)= g(A) because g(a)≥f(a) for a≥A and g(a)≤f(a) for a≤A and, similarly, f(B)=g(B) because g(b)≥f(b) for b≤B and g(b)≤f(b) for b≥B, by the definition of A and B. In particular, if f(a) is decreasing at a=A then g(a) is increasing and if f(a) is increasing at a=A, then g(a) is decreasing and the reverse situation obtains at B so that if f(a) is increasing at a=A then f(b) is decreasing at b=B because f(a) and g(b) are parabolas.

Figure 1: Bhatia and Davis (1999)

But if f(a) is decreasing at a=A, then f'(A)=2(A-avg)≤0 and f'(B) = 2(B-avg) ≥0 so that A≤avg≤B (Bhatia-Davis). On the other hand, if f(a) is increasing at a=A then f'(A) = 2(A-avg)≥0 and avg≤A and f'(B)= 2(B-avg)≤0 so that avg≤A and avg≥B, which is impossible unless A=B=L and we already know that f(L)≤g(L) (Popoviciu). That completes the proof; please see Figure 1 on the right for an illustration.

For more information, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us (for free) in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”.

Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability.

We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now.

The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.