(B)(N) EURNY Eurasian Natural Resources Corporation PLC ADR

Deal Book. Eurasian Natural Resources Corporation PLC (ENRC) is in a bitter custody battle with a trio of the founding shareholders who own 45% of the stock between them.

They have the backing of the State Property & Privatisation Committee of Ministry of Finance of Kazakhstan which owns another 12% of ENRC, and they want to “buy” back the rest of the company from “uncle” Kazakhmys PLC who owns 26% of the stock and is also a major copper and other natural resources miner and electrical power producer in Kazakhstan since 1930 (Reuters, May 31, 2013, Exclusive: Founders seek more time for ENRC bid – sources).

Reuters: The Boss Mining Copper Operation in the southern Congolese province of Katanga – ENRC

To sweeten the deal, the Kazakh government has stock in Kazakhmys PLC (as well as 12% of ENRC, as above) and – in lieu of money – has offered to tender its stock in Kazakhmys along with cash from the founders and their backers in order to buy in all of the outstanding shares.

The specifics of the offer are 175 pence in cash plus 0.231 of a Kazakhmys share from the Kazakh government for each ENRC share, which amounts to about 251 pence in contrast to ENRC’s closing price of 239 pence last Friday (ibid, Reuters).

(B)(N) EURNY Eurasian Natural Resources Corporation PLC – Kazakhstan

However, in our view, the deal is still a “cheap shot” and undervalues the company (ENRC) significantly to what it would be worth to anyone who could actually produce its demonstrated “values” and no doubt that’s what the new owners have in mind.

We can say this with confidence because the demonstrated Risk Price (SF) of the ADR is $3.90 and twice the offer of 251 pence per share which is worth $3.82 per share or $1.91 for one ADR certificate worth 1/2 share. Please see Exhibit 1 below.

There are other players in the game, too, but not enough to score. Mr. Suleiman (Suleyman) Kerimov is said to own about 3% of the stock; and the four investment firms: BlackRock Incorporated of New York; SKAGEN Fondene of Stavanger, Norway; GIC Asset Management, a sovereign wealth fund based in Singapore; and Capital Research & Management, Los Angeles, California, each own about 1% of the stock for investments that would be currently valued at $50 million each, and down significantly from about $150 million last year (please see Exhibit 1 below).

The remaining shareholders of 10% of the stock would also lose about $1 billion on the deal, and there are no “Lawyers Without Portfolio” (LWPs) to represent them and agitate for the creation of “greater shareholder value” and “shopping the company around”; please see our recent Post, (B)(N) SFD Smithfield Foods Incorporated, May 29, 2013.

If Kazakhmys PLC throws its 26% interest into the deal, then more than 75% of the shares will be in the deal and the company can be delisted, and the remaining shareholders will get what they get, and at least $9 billion of “shareholder value ” has just “vanished” between June of last year and today.

The company is also operating at a loss of about ($600 million) on sales of $6 billion but is anticipating to pay dividends of $145 million to its shareholders for a current yield of 3% ($0.028 per share semi-annually on the ADR). Its competitors are much larger; BHP Billiton Limited ($60 billion), Rio Tinto PLC ($50 billion), and Vale SA ($47 billion).

But we would think that a company that mines copper in the Katanga province of the Congo (please see the illustration above) is a lot bigger than it looks and should fetch more than just one year’s revenue. Just saying.

Exhibit 1: (B)(N) EURNY Eurasian Natural Resources Corporation PLC ADR – Risk Price Chart

(B)(N) EURNY Eurasian Natural Resources Corporation PLC ADR (Equivalent to 1/2 Common Share at 240 pence)

Eurasian Natural Resources Corporation PLC is a diversified natural resources company performing integrated mining, processing, power generation, logistics and marketing operations.

(Please Click on the Chart to make it larger if required.)

The ADRs (American Depository Receipts) are thinly traded in New York in very small fractions of the traded stock in ENRC in London, England; one ADR is equivalent to 1/2 share of ENRC which trade in pence and, therefore, to avoid an arbitrage opportunity, the New York ADR price must also reflect currency exchange values as well as the much greater trading volume in London.

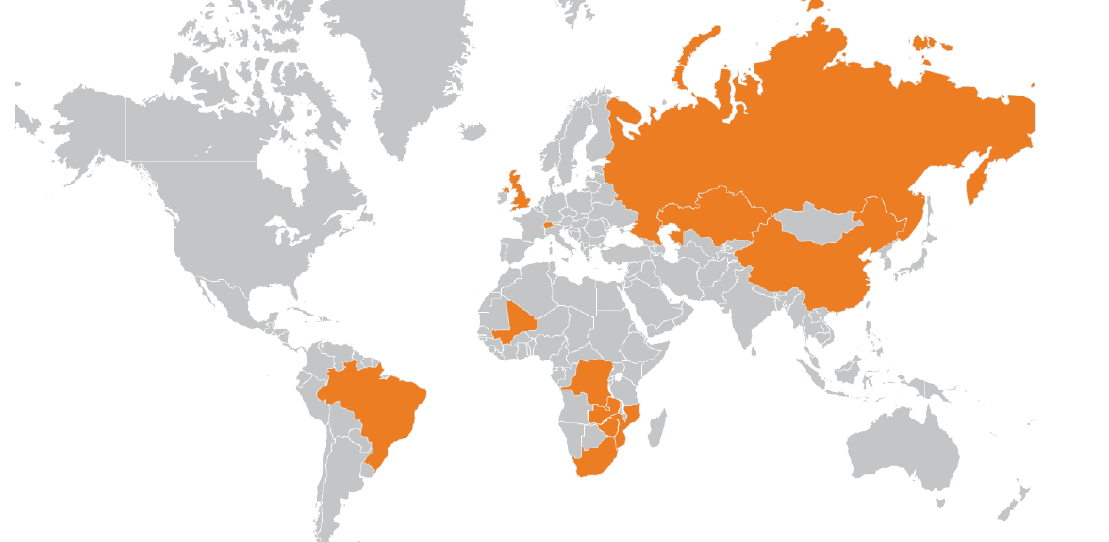

(B)(N) EURNY Eurasian Natural Resources Corporation PLC – Global Mining Operations

From the Company: Eurasian Natural Resources Corporation PLC (ENRC) is a diversified natural resources company, and engages in mining, processing, energy, logistical, and marketing operations worldwide. The company operates through six segments: Ferroalloys, Iron Ore, Alumina and Aluminium, Other Non-ferrous, Energy, and Logistics.

The Ferroalloys segment extracts and sells chrome ores, as well as produces ferroalloys from chromium and manganese ores. It offers high-, medium-, and low-carbon ferrochrome; and other alloys, including ferrosilicochrome and ferrosilicomanganese. This segment sells its ferroalloys to steel producers, third party ferroalloy producers, and the chemical industry.

The Iron Ore segment engages in the exploration, extraction, processing, and manufacture of iron ore products. It produces and sells iron ore concentrate and pellets primarily to steel producers.

The Alumina and Aluminium segment is involved in the extraction and processing of bauxite and limestone; and the smelting of alumina and aluminum. It sells alumina to aluminum producers.

The Other Non-ferrous segment engages in the exploration and extraction, processing, and manufacture of copper and cobalt products; the exploration of other minerals, including coal, bauxite, platinum, and fluorspar in Africa; and trucking and logistics operations.

The Energy segment is involved in coal mining and processing to produce coke and semi-coke products; and power generation in the Republic of Kazakhstan.

The Logistics segment provides transportation and logistics services. Its operations include freight forwarding, wagon repair services, railway construction and repair services, and trucking. This segment also operates a railway transfer and reloading terminal on the Kazakhstan-China border. Eurasian Natural Resources Corporation PLC has 80,000 employees and is headquartered in London, England.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.