(B)(N) TKA ThyssenKrupp AG

Deal Book. In business since 1811 and headquartered in Essen, Germany, with operations in 80 countries, the legendary steel maker and advanced technology industrial materials and equipment manufacturer, ThyssenKrupp AG, is divesting its steel making and processing plants in Brazil and Alabama, U.S.A., known jointly as the Steel Americas (Reuters, August 10, 2013, Steel Americas cloud hangs over Germany’s ThyssenKrupp, and The Wall Street Journal, July 16, 2013, ThyssenKrupp Close to Selling Brazil Steel Mill Stake to CSN).

Courtesy: Thyssen Krupp AG

However, the processing plants are drawing offers of only $2 billion – $3 billion Euros, which is short of the book value of $3.4 billion Euros, and well short of the estimated $12 billion Euros that the company has spent in developing these plants over the last seven years.

Moreover, there appears to be only one buyer, Brazil’s Companhia Siderurgica Nacional (CSN), and even then, not without the approval of the Brazilian miner, Vale SA, which owns 27 percent of the Brazilian mill and has a long-term exclusive supply agreement for iron-ore, and the Brazilian government is also involved in the negotiations.

ArcelorMittal MT and Nippon Steel & Sumitomo Metal Corporation have also been mentioned as possible buyers for the Alabama plant at US$2 billion (ibid, WSJ), but the combined current operating losses on the plants, due to unanticipated higher costs and slack demand, have totalled about $500 million Euros in the last six months – let’s say $80 million Euros, or US$100 million per month to keep the furnaces running and the folks employed – and the plants have been for sale for more than a year.

To date, ThyssenKrupp has cancelled its annual dividend of 0.313 Euros, paid in January in the previous two years, for a then total payout of $170 million Euros and rough yield of 2% at the current stock prices.

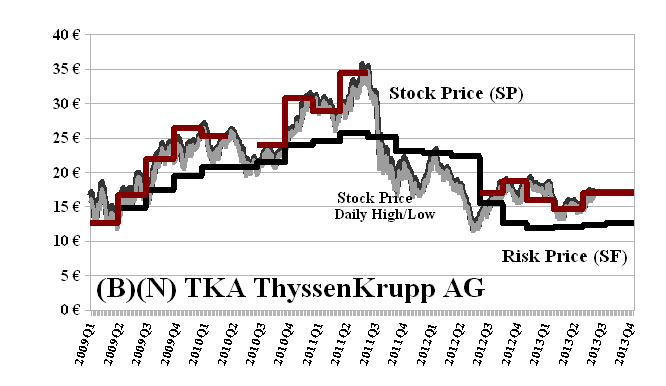

Despite these difficulties that would likely decimate a lesser stock trading on noise and volatility, the company remains profitable with annual sales of about $40 billion Euros (ibid, Reuters) and is trading above the price of risk (please see Exhibit 1 below); and although four to five million shares change hands on a typical day, the stock was issued as bearer shares and the Krupp Foundation owns about 25% of the total shares outstanding.

The float is, then, about 385 million shares, and the current market value of the company is about $9 billion Euros. The company estimates that 90% of the shares are held by institutions, and in large blocks in private hands, and that about 250,000 shareholders hold the balance of 10% or 50 million shares.

If the Steel Americas are sold, the company has stated that it intends to make a rights offering that would raise an additional $750 million to $1 billion Euros.

Refreshingly absent in this difficult situation are “green mailers“, hedge funds, and “activist shareholders” who would like to turn a “quicker buck”, so to speak. Please see our recent report, The S&P TSX “Hangdog” Market, for more information on foreign and “alternative” investments in this season of desperate returns and accountability.

Exhibit 1: (B)(N) TKA ThyssenKrupp AG – Risk Price Chart

(B)(N) TKA ThyssenKrupp AG

ThyssenKrupp AG operates in the areas of materials and technologies in Germany and internationally.

(Please Click on the Chart to make it larger if required.)

From the Company: The company offers flat carbon steel products for use in the automotive, construction, appliance, energy, and packaging sectors; and carbon and stainless steel, tubes and pipes, nonferrous metals, and plastics; and supplies new and used industrial plant and equipment. It also provides tailored materials services, such as processing, logistics, warehouse, inventory management, and supply chain management; technical and infrastructure services for railway equipment, civil engineering, port construction, and plant and steel mills; and installation, maintenance, and repair services for machinery, plant, and technical structures, as well as engages in consultancy and planning, equipment hire, and customer and spare parts services activities. In addition, the company is involved in the construction, service, maintenance, and modernization of passenger and freight elevators, escalators, moving walks, passenger boarding bridges, and stair and platform lifts. Further, it provides cement and minerals industry equipment; machinery, plant, and systems for the mining, processing, handling, and transportation of raw materials and minerals; components for body and final assembly process chain; assembly systems for automotive and supply industry production lines; and transrapid components, as well as engages in the planning and construction of chemical plants, refineries, and other industrial plants. Additionally, the company develops, constructs, and refits submarines and naval surface vessels; supplies premium segment yachts; and offers components for the automotive, construction, and engineering sectors, as well as for wind turbines. ThyssenKrupp AG was founded in 1811, has 150,00 employees in 80 countries, and is headquartered in Essen, Germany.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.