(B)(N) SLF Sun Life Incorporated

Deal Book. Sun Life is a life insurance, disability insurance, and group benefits insurer that also offers investment products as a natural extension of its services, such as how to deal with life insurance benefits or annuities. But no life insurer – nor anyone else – can guarantee returns in the equity markets and that causes capital stress in life insurance companies who are carefully regulated and whose equity investments are marked-to-market regardless of how promising or hopeful they might be (Reuters, June 21, 2013, Sun Life says regulatory hurdles delay sale of U.S. annuity unit).

The Market Line

Bad Things Can Happen To Good People

Moreover, there is nothing in the investment models that they rely on that can be used to guarantee the capital.

There are only three investments that can and will guarantee the capital 100%: Real Return Bonds (RRBs) or Treasury Inflation Protected Securities (TIPS) or The RiskWerk Company.

Anything else is just a gamble and of these three, only RRBs and TIPs can guarantee a return that is at or above the rate of inflation because they are the government, and they are inflation (in a nice way by way of the Consumer Price Index (CPI)), and can always tax or print more money if there’s a problem because of a buoyant economy.

The rest of us have to earn it and the market wrote down Sun Life in December last year because of the announcement that the company was intending to sell its US annuity business (Reuters, December 17, 2012, Sun Life sells U.S. annuity business, shares drop) and that would affect the earnings and because so much investment is tied to the Capital Assets Pricing Model (CAPM) that is widely used by hedge funds, mutual funds, and so forth, a small change in a company’s stock price can start an even larger one as the models begin to sell the stock.

Hug The Bear. Thank You!

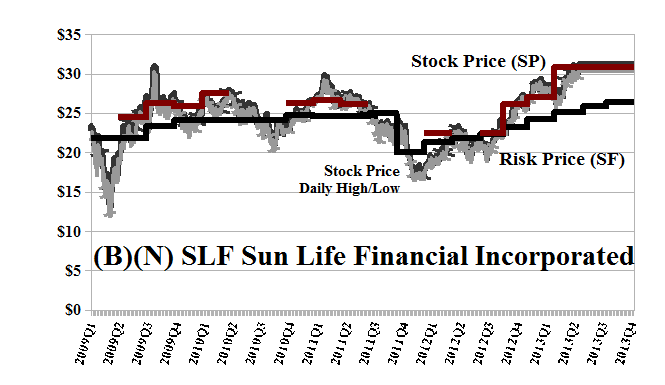

All of that is good for us because whereas the market tends to shoot the bears, we embrace them. The market sold us out on a stop/loss (please see Exhibit 1 below) but because Sun Life was still trading above the price of risk, we just took profits, and bought it back at a lower price, and it’s in our portfolio now, the Perpetual Bond™, at $30 and up from the bargain prices of $25 to $27 earlier this year.

Our estimate of the downside in the stock price is still minus ($2.50) so that it would trade for us between $28 and $32 without surprise. On the other hand, the dividend is $0.36 per share per quarter for an expected payout of $900 million this year and a current yield of 4.7% which we don’t have to leave on the table for the hair-triggers to get.

The August put at $28 can be bought for $0.38 per share today and the August call at $32 can be sold against our long position for $0.42 per share, so that for the cost of holding the stock at $30 and a small gain on the collar ($0.38 less $0.42), we can hold the stock for between $28 and $32 for the next several months and not worry about any stray bullets from the market line.

Exhibit 1: (B)(N) SLF Sun Life Insurance – Risk Price Chart

(B)(N) SLF Sun Life Incorporated

Sun Life Financial Incorporated provides diversified financial services. It offers savings, life and health insurance, and retirement and pension products to individuals and groups through its operations in Canada, United States, United Kingdom and Asia.

Please Click on the Chart to make it larger if required.)

From the Company: Sun Life Financial Inc., an international financial services organization, provides a range of protection and wealth accumulation products and services to individuals and corporate customers. The company operates in five segments: Sun Life Financial Canada, Sun Life Financial U.S., MFS Investment Management, Sun Life Financial Asia, and Corporate. It offers insurance products, such as universal life, term life, permanent life, participating life, critical illness, long-term care, and personal health insurance; savings and retirement products, including accumulation annuities, guaranteed investment certificates, payout annuities, mutual funds, and segregated funds; provides life, dental, drug, extended health care, disability, and critical illness benefit programs to employers; and voluntary benefit solutions, including post-employment life and health plans to individual plan members. The company also offers pension and retirement products and services, including investment-only segregated funds and fixed rate annuities, stock plans, group life annuities, pensioner payroll services, guaranteed minimum withdrawal benefits, and solutions for de-risking defined benefit pension plans. In addition, it provides asset management services to individual and institutional investors, as well as independent financial advisors through mutual funds, separately managed accounts, and retirement plans; and offers run-off reinsurance services. The company markets and distributes its products through its own sales force and third-party distribution channels, as well as through partnership with independent advisors and benefits consultants in Canada, the United States, the United Kingdom, Ireland, Hong Kong, the Philippines, Japan, Indonesia, India, China, Australia, Singapore, Vietnam, and Bermuda. Sun Life Financial Incorporated was founded in 1999 and is headquartered in Toronto, Canada. Sun Life has about 15,000 employees and over 120,000 advisors world-wide.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2006) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks. Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.Disclaimer Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.