The Dow (B)-Nots

Drama. There are nine companies in the Dow Jones Industrial Companies that didn’t make it into the (B)-list of The Wall Street Put (please see our Post, The Wall Street Put, April 2013); we’re going to call them the Dow (B)-Nots (at least today) because they’re (N)’s, and not (B)’s, with the exception of Chevron and AT&T which we started buying in February and March, respectively, and, therefore, too late to make it into the 1st quarter portfolio. Please see Exhibit 1 and 2 below.

The case of AT&T is still tricky, however, because our estimate of the downside volatility is minus ($2) and an ambient price drop, for whatever reason, could trigger selling at the $Stop/Loss price of $36 because a ($2) loss on the stock price would breach the Risk Price (SF) of $36 and throw it back into the (N)-pit; to protect our price, we bought the July put at $37 for $0.75 per share and sold an offsetting short call at $40 for $0.52 per share so that for a net cost of $0.23 per share ($0.75 less $0.52), we’re indifferent to price changes between $37 and $40 for the next several months, and can collect our hefty dividends of $0.45 per share per quarter for a smashing current yield of 4.7%.

Of the nine, we’d like to take a closer look at Caterpillar, Chevron and du Pont; all the others have been discussed in recent Posts (Alcoa in Black Swans & The Lame Ducks, November 2012; Cisco in (B)(N) CSCO Cisco Systems Incorporated, February 2013; Hewlett-Packard in Belts, Braces and Scaffolds, November 2012 and, also, in America’s Most Unwanted Companies, February 2013; Intel in (B)(N) INTC Intel Corporation, April 2013; Microsoft in Microsoft, Apple, Google & The Tech Wars, February 2013; and AT&T in (B)(N) DISH Network Corporation, April 2013.

Some of these companies have pretty good price increases since December; for example, Hewlett-Packard is up +42% from $14 to $20 (please see Exhibit 2 below) but the Risk Price (SF) is $51 and seems to have been crafted on another planet. But Hewlett-Packard isn’t going there, absent “surprise”, and we need to leave those profits to “risk seeking” adventurers who are out-bidding each other in their excitement to make money, or are far-seeing and see what we don’t (perhaps like Christopher Columbus, or the fabled Viking raider, Ragnarr Loðbrók, who discovered Northumbria in the 9th century), or they think that earnings matter (please see our Post, Earnings Don’t Matter, April 2013). We’re confident that we’ll see their money later.

As a portfolio, these name brands have returned +4.3% this year in contrast to the Perpetual Bond™ in the Dows which is up +13% (please see The Wall Street Put, April 2013).

Exhibit 1: The Dow B-Nots (N) – Cash Flow Summary – April 2013

The Dow (B)-Nots (N) – Cash Flow – April 2013

(Please Click on the Chart to make it larger if required.)

Exhibit 2: The Dow B-Nots (N) – Portfolio Summary – April 2013

The Dow (B)-Nots (N) – Portfolio – April 2013

(Please Click on the Chart to make it larger, and again, if required.)

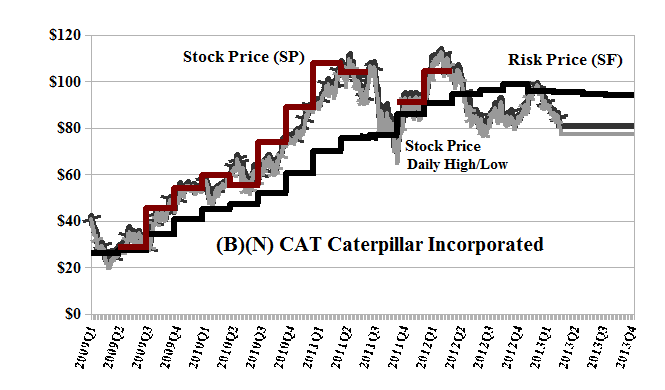

Caterpillar is up today (+2.5%) at $82 and the trading volume is more than 13 million shares, more than twice the normal daily volume (Reuters, April 22, 2013, Caterpillar profit misses, cuts outlook on weak mining). We sold the last of our holdings at $105 last year and haven’t owned it since because – and only because – the stock price is trading below the Risk Price (SF); please see Exhibit 3 below, Red Line Stock Price (SP) has to be above the Black Line Risk Price (SF).

Exhibit 3: (B)(N) CAT Caterpillar Incorporated – Risk Price Chart

(B)(N) CAT Caterpillar Incorporated – April 2013

Caterpillar Incorporated is a manufacturer of construction and mining equipment, diesel and natural gas engines, industrial gas turbines and diesel-electric locomotives. It also provides financial services through its subsidiaries.

(Please Click on the Chart to make it larger if required.)

Chevron is in the Perpetual Bond™ since February; the current Risk Price (SF) is $108 and it’s trading at $116 today; the dividend is $0.90 per share per quarter, or $7 billion per year, to its shareholders and the current yield is 3%. Please see Exhibit 4 below.

Exhibit 4: (B)(N) CVX Chevron Corporation – Risk Price Chart

(B)(N) CVX Chevron Corporation – April 2013

Chevron Corporation provides administrative, financial, management and technology support to U.S. and international subsidiaries that engage operations of petroleum, chemicals, mining, power generation and energy services.

(Please Click on the Chart to make it larger if required.)

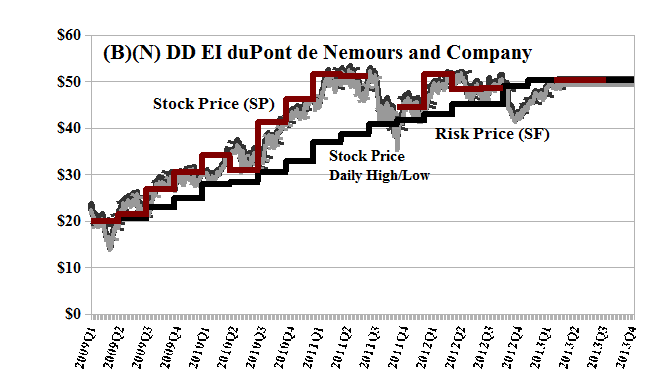

DuPont also looks promising; the Risk Price (SF) is $52 and it’s trading at $50 today; the dividend is $0.43 per share per quarter, or $1.6 billion per year, to its shareholders for a current yield of 3.4%. Please see Exhibit 5 below.

Exhibit 5: (B)(N) DD E.I. du Pont de Nemours & Company – Risk Price Chart

(B)(N) DD EI duPont de Nemours and Company – April 2013

E.I. du Pont de Nemours & Company offers a range of products and services for markets including agriculture and food, building and construction, electronics and communications, general industrial, and transportation.

(Please Click on the Chart to make it larger if required.)

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation.

Stock prices that are less than the price of risk are “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”. On the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information. Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more details.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.