(B)(N) CNR Canadian National Railway Company

Drama. There is a light at the end of the tunnel in Canada and it’s the two Canadian railways, the CNR Canadian National and the CP Canadian Pacific Railway, both of which have been in the Perpetual Bond™ for a long time (please see Exhibit 1 and 2 below) and long before the “shareholder activist” attention of Pershing Square Capital Management and new investments by other notables (please see our earlier Posts, (B)(N) CNR Canadian National Railway Company, December 2012, and (B)(N) CP Canadian Pacific Railway Limited, November 2012).

The CNR is in the news today because it beat the chill of the analyst forecast average of $1.21 per share by a penny a share on “adjusted” revenue of $519 million (Reuters, April 22, 2013, CN Railway profit hurt by winter weather chill) but that does not explain a drop in the stock price of nearly $1 a share (or 1% which is what a penny looks like) to $97, and a loss of $340 million in the market value of the company.

Nor does it help us with the “big picture”; there are currently 82 companies – but less than a third of all the possible companies – in the S&P TSX Perpetual Bond™; they have a total market value of $800 billion, and nearly half of them have had stock price gains in excess of +10% in the last several months, in contradistinction to less celebrated earnings reports and the index which is down minus (4%). Please see the S&P TSX Composite section (Exhibit 7 & 8) of our recent Post, The Wall Street Put, April 2013.

To protect ourselves against ambient volatility and “surprise”, we always have either a stop/loss price in effect, or a “collar” in case we want control on stock price outcomes and options on whether we keep the stock or sell it. The Canadian National has an indicated downside volatility of minus ($7) per share so that we would not be surprised by any price between the current $97 and a low price of $90 or a high price of $114, with no explanation required. Since we’ve been holding the stock since $43 in 2009 (please Exhibit 1 below, Red Line Stock Price (SP) above the Black Line Risk Price (SF)), we could afford the loss. On the other hand, the September put at $94 costs $3.40 today and we can sell or short an offsetting call at $100 for $3.45 – sounds like a deal to us. For a gain of $0.05 per share today ($3.40 less $3.45) against our long position, we can be assured of no less than $94 and no more than $100 during the next six months, and collect dividends of $0.43 a share per quarter for a current yield of 1.8%, which, of course, is much higher for us because be paid a lot less for the stock, four years ago, and sixteen quarterly earnings reports ago, not all of which were as discriminating as today’s report.

Exhibit 1: (B)(N) CNR Canadian National Railway Company – Risk Price Chart

(B)(N) CNR Canadian National Railway Company – April 2013

Canadian National Railway Company is headquartered in Montreal, Quebec, and together with its wholly-owned subsidiaries, is engaged in the rail and related transportation business.

(Please Click on the Chart to make it larger if required.)

CN has a current market value of $42 billion, total assets of $27 billion and a shareholders equity of $11 billion.

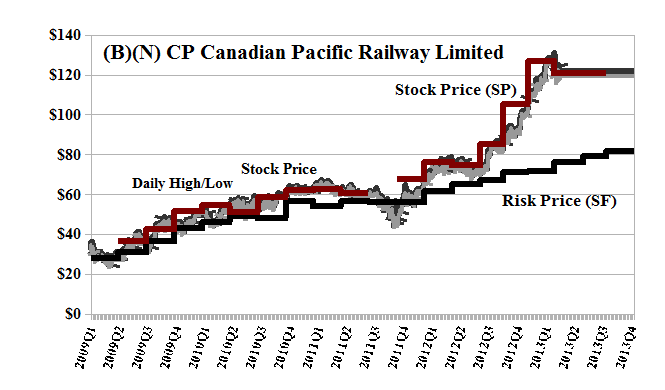

The situation of the Canadian Pacific Railway is similar but the “gap” between the “risk adjusted price” is $52, with a stock price of $122 over a risk adjusted price, the Risk Price (SF), of $70; and the stock price is up +24% since the beginning of the year and well up above our first purchases at $38 in 2009 (please see Exhibit 2 below).

Our estimate of the downside risk due to volatility is minus ($15), which we could tolerate, but to stay on the train in case the “activist investor” interest and other excitement wanes, we’ve bought the September put at $120 per share for $7.70 per share and sold an offsetting opportunistic and hopeful call at $125 for $7.50 per share so that for a net cost of $0.20 per share ($7.70 less $7.50), we can continue to collect our dividends of $0.35 a share per quarter for a current yield of 1.2% which is, of course, worth a lot more to us, and also stay on track between $120 and $125 for the next six months. None of that was in the news today or in anyone’s earnings reports.

Exhibit 2: (B)(N) CP Canadian Pacific Railway Limited – Risk Price Chart

(B)(N) CP Canadian Pacific Railway Limited – April 2013

Canadian Pacific Railway Limited provides freight transportation services, logistics solutions, and supply chain expertise in Canada and the United States.

(Please Click on the Chart to make it larger if required.)

CP is about half the size of CN, with a market value of $21 billion, total assets of $15 billion and a shareholders equity of $5 billion.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation.

Stock prices that are less than the price of risk are “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”. On the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information. Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more details.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.