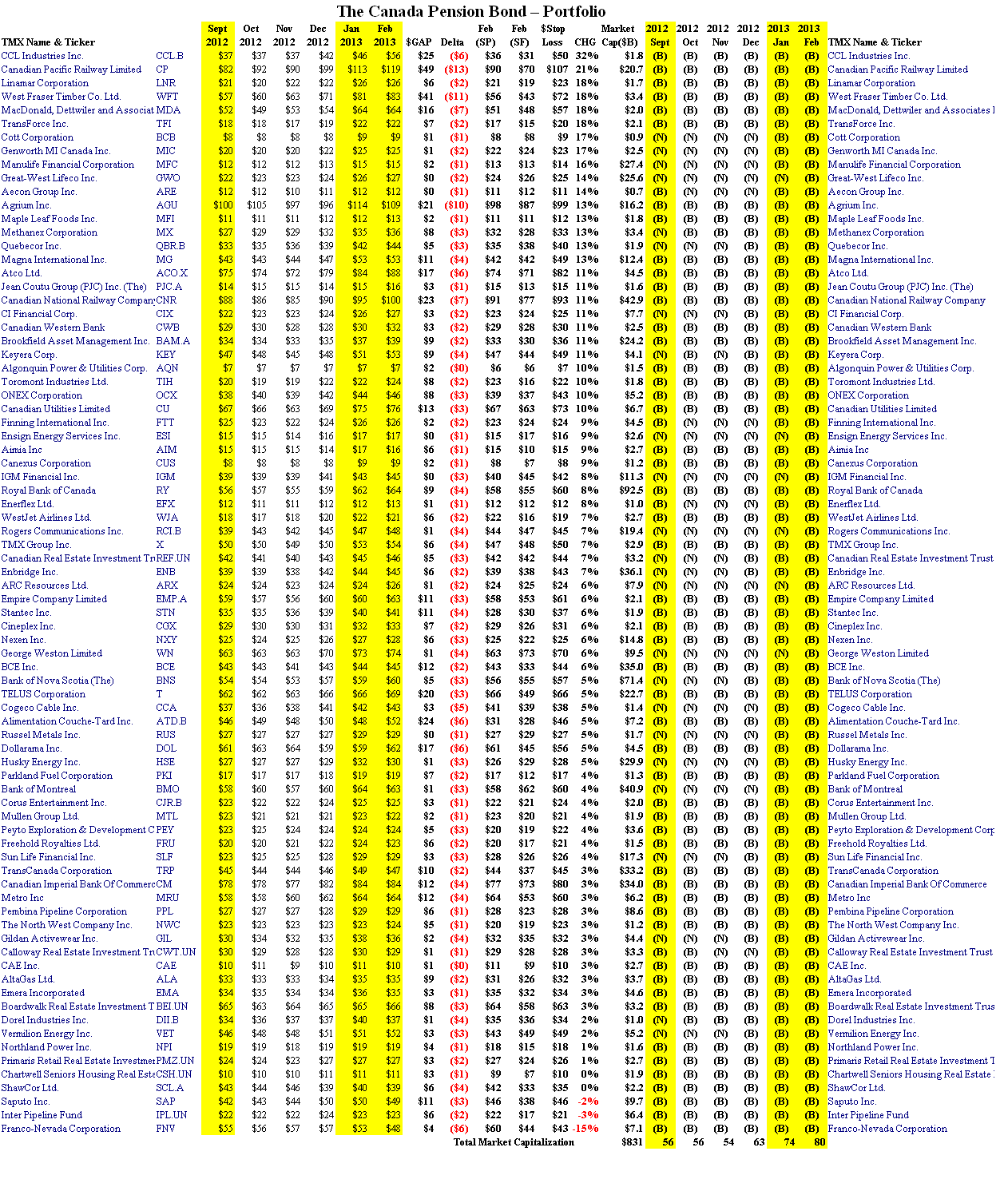

The Canada Pension Bond

The Canada Pension Bond™ is the result of a “replication technology” applied to the stocks of the companies in the Canadian equity market (the three hundred or so companies of the S&P TSX called “Canada” in this context) that produces (or “replicates”) a “bond” in the sense that the invested capital is provably 100% safe – 100% Capital Safety – akin to a high-grade corporate or government bond AND we have reason to expect a hopeful (but not necessarily guaranteed) rate of return above the rate of inflation. Actually, we do more than that AND we’ve already done it in the first two months of this year. If inflation is less than 6% this year – which is highly likely absent a fiscal crisis or economic disaster that we have no reason to expect – then we can say that the Canada Pension Bond™ has produced “3% plus inflation, every year, no matter what” guaranteed and we can reasonably expect to do that every year, no matter what, as long as there is a capital market somewhere, and hopefully in Canada, that is at all productive.

“Small” investors cannot do that (and “small”, as we explain below, would be less than $2 million in capital in this example). Small investors might make a lot more than “3% plus inflation” in some years, such as in 2009 in which +15% was to be expected because the “markets” returned that much, or a lot less such as in 2008 when -20% was the norm, but they will not be able to produce “3% plus inflation, every year, no matter what” guaranteed because they depend on luck or happenstance and factors of the market that are not explained by luck. (For more on this and the theme of investment by “risk aversion” rather than “risk seeking”, please see almost any of the (B)(N) Company posts or more specifically, The Active Investor (DOA), November 2012, or The Investor Product, February 2013.)

The Canada Pension Bond™ is, therefore, an application of the Perpetual Bond™ applied to the S&P TSX market with a domain that is restricted to only the companies that pay a dividend (however small, but typically, with a 2%-3% yield which we accumulate in addition to the capital gains that we are concerned to obtain by the “replication technology” in the equity market) and with a market capitalization in excess of $500 million.

We “like” companies that pay dividends because it tends to demonstrate a mature management competence that tends to lead the company to make profits in excess of what they need to spend to make them, as opposed to so-called “growth companies” that don’t have any profits or claim that their earnings are best spent on their own enterprise and if investors are to make profits by buying and selling the stock of their company then they will just have to make them by buying and selling their stock to each other on the basis of the “greater fool” theory of investment management.

We also prefer to invest only in mid- to large-cap stocks which in this market means companies with a market value in excess of $500 million. Our current portfolio has eighty companies in it (please see Exhibit 2 and 3 below) and the same portfolio scales from $2 million to $20 million to $200 million to $20 billion in the $800 billion market without causing us to own or control any of the companies in it. After all, we don’t know anything about retail, oil & gas, railroads, gold mines, forestry, et cetera. We’re just investors and the only thing that we need to be sure of is 100% Capital Safety – we don’t want to lose any of our money – and we would like to have an investment return that exceeds the rate of inflation even though we also don’t know anything about “economics” or “fiscal policy” that might reliably affect the stock prices of all the companies in the market. (For more information on what we do know about “stock prices”, please see our more ambitious Posts, Stock Prices Are The New Pink, June 2012, or Do Stock Prices Mean Anything?, November 2012.)

The only Rule that we have is that we only buy and hold the stock of companies that appear to trading above the Risk Price (SF) and otherwise not, that is, we sell them or don’t buy them if they are trading or tending to trade below the Risk Price (SF). There are many examples and explanations of that Rule in these Posts but consider the case of CCL.B CCL Industries Incorporated that has been in our portfolio since the beginning of last year (2012 and earlier) and has gained +32% since December (and it is not a candidate for acquisition as far as we know).

Exhibit 1: (B)(N) CCL.B and CCL.A CCL Industries Incorporated – Risk Price Chart

CCL Industries Incorporated supplies manufacturing services and specialty packaging products for the non-durable consumer products market including formulation and manufacturing services, labels, aluminium and plastic specialty tubes, containers, and closures to marketers of cosmetic, personal care, pharmaceutical, household, and specialty food products.

(Please Click on the Chart to make it larger if required.)

CCL Industries has two classes of stock, CCL.B with 31.4 million shares outstanding is a non-voting stock and holds most of the market value, and CCL.A with 2.4 million shares outstanding is the voting and, therefore, the ownership stock. It trades at a slight premium to the non-voting stock but each class of stock receives comparable dividends of $0.86 per share for a total of $29 million per year and a rather meagre yield of 1.5% at the current prices. As investors, of course, we don’t know anything about labels and packaging which is CCL’s business and, even more, as investors in the Class B stock, we have no say at all in how the company is run. All that we know is that stock prices above the “price of risk” as summarized by the Risk Price (SF) are provably an “economic free good” and the investor expectation (for whatever reason) is that those prices will be earned. (For more information, please see our Posts, The Price of Risk, August 2012, and The Nash Equilibrium & Its Stock Price, October 2012.) We could, of course, “take profits” or risk a volatility based downside of minus ($6) per share by setting the stop/loss at $50 which is still more than twice our purchase price in 2009. Unfortunately, there is no option market for this stock (please see our Posts, The Wall Street Put, August 2012, and Popoviciu’s Volatility, September 2012, for more information on how we can routinely protect our prices at nearly no cost).

The Canada Pension Bond™ which is illustrated in Exhibit 2 and 3 below is, therefore, an actively managed portfolio of stocks in the S&P TSX that respects only the One Rule – we only buy or hold the stock of a company in the portfolio if the ambient stock prices as summarized by the Stock Price (SP) appear to be above the Risk Price (SF) (designated as a (B) in Exhibit 3 below) and otherwise, the stock is sold or not bought (designated as an (N)). The Cash Flow Summary has been simplified to reflect buying and selling only in blocks of 1,000 shares at the prices shown in Exhibit 3.

So, for example, this portfolio is a continuation of one which we started much earlier in December 2011 and its status is shown at the end of September 2012. The portfolio value is $2,075,000 at the end of September but we also bought one company and sold two during September leaving an ongoing margin account of minus ($111,000 which is convenient but not required) and a net total value (portfolio of 56 companies plus or minus cash) of $1,964,000 at the beginning of October which increased to $2,153,000 during October before the required transactions (we bought three and sold three). Similarly, the total value at the end of December was $2,062,000 and $2,254,000 at the end of February for a +9% gain for the year to date plus dividends that are expected but not yet accumulated in this report.

The Companies line, on the other hand, shows what happened if we had just bought 1,000 shares of each of the eighty companies in the domain, whether (B) or (N), and we note that the cost was $2,861,000 at the end of September and the value at the end of February is $3,252,000 for a +8% gain in contrast to the Index which has a +6% gain so far this year but also demonstrated recent volatility of between -4% and +5% per month (Change line).

One could conclude that +8% is not a bad return in two months and that simply buying all of the mid- to large-cap dividend paying stocks in the S&P TSX is not a bad policy. It just takes more money, in general, and we have shown elsewhere that the portfolio of stocks that are all (N) and only (N) tends to provide a zero or slightly negative return. In other words, (N) is just “noise” and including them is a speculation that, on balance, provides a zero or slightly negative return in large portfolios. Please see, for example, What’s a girl to do?, January 2013, or Stock Prices Are The New Pink, June 2012, or the NASDAQ 100 – (B)(N) There And Done That, June 2012.

Exhibit 2: The Canada Pension Bond™ – Cash Flow Summary

(Please Click on the Chart to make it larger if required.)

Exhibit 3 below shows the contents of The Canada Pension Bond™ at the end of February (which consists of all eighty of the eligible companies) and their (B)(N)-status in the prior months since the end of September. Ambient (or sampled) stock prices are shown in the first six columns by month and the $GAP is the difference between some stock price in February and the Risk Price (SF) (“Feb (SF)”) which does not change until new balance sheet information becomes generally available.

In contrast, although there is always a “stock price” every minute of every day, we don’t really know what “the” current Stock Price (SP) is until we decide or are required to make a buy, sell or hold decision and that price may also be affected by the details of “price protection” (please see our Post, The Wall Street Put, August 2012).

For example, we note that CCL is trading at $56 during or at the end of February (Feb 2013) and the “$Stop Loss” price is $50 ($56 less the Delta) whereas our “buy and hold price” is $36 (Feb (SP) from previous months) but the Stock Price (SP) is nominally $46 (please see Exhibit 1 above) and was updated when we updated the Risk Price (SF) to $31. Similarly, the table of (B)’s and (N)’s is a “state table” that indicates the kind decisions that we need to consider rather than an “action table” that summarizes what we actually did or had to do. For example, a month-to-month state table such as “(B)(N)(B)” would have an outcome that is either “(B)(B)(B)” indicating that we continued to hold the stock or “(B)(N)(N)” indicating that we sold the stock and did not buy it back, and a table such as “(N)(B)(N)” would typically have an outcome of “(N)(N)(N)” or “(N)(B)(B)”.

Exhibit 3: The Canada Pension Bond™ – Portfolio

(Please Click on the Chart to make it larger, and again, if required.)

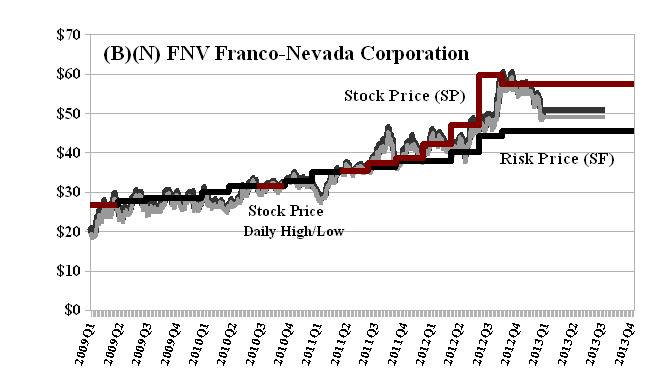

As another example of the use of the table in Exhibit 3, consider the case of the Franco-Nevada Corporation (Exhibit 4 below). Franco-Nevada was the “worst performing” stock in the portfolio and the stock price has dropped minus (15%) since the end of December but the stock prices are still above the Risk Price (SF) of $44 which was calculated in September and the Stock Price (SP) (Feb (SP)) is $60 which is the price that is protected by either a stop/loss at $54 ($60 less the Delta of $6) or a protective put at $60 which we do not necessarily have to execute now even though it’s currently worth about $12 per share.

Exhibit 4: (B)(N) FNV Franco-Nevada Corporation – Risk Price Chart

Franco-Nevada Corporation is a gold-focused royalty and income stream company with additional interests in platinum group metals, oil & gas and other resource assets. The current dividend is $0.06 per share per month or $100 million year for a modest yield of about 1.5%.

(Please Click on the Chart to make it larger if required.)

The Canada Pension Bond™ is a commercial investment product. We offer it to family trusts, endowment funds and pension plans as “3% plus inflation, every year, no matter what” guaranteed (and no fees or loads) and we show exactly how the guarantee is enforced and enforceable which makes the work and life of the fund sponsors and beneficiaries much easier. It could also be mutualized by major selling organizations such as the banks, insurance companies and mutual funds on the basis of “no fees, no loads and 3% plus inflation, every year, no matter what” guaranteed which would undoubtedly create a revolution in “The Investor Product” (please see our Post, The Investor Product, February 2013).

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.