(B)(N) SPLS Staples Incorporated

Deal Book. Staples is estimated to have 40% percent of the U.S. office supply market with gross revenues of about $25 billion per year but paper thin margins on the order of 5% or less than $1 billion per year, and its smaller rivals, Office Depot and OfficeMax, are combining for a further 20% and 15% of that market (Reuters, February 20, 2013, Office Depot in $1.2 billion deal to buy rival OfficeMax). Apart from a great deal of enthusiasm for the office supply market three years ago in 2009 and early 2010 (please see Exhibit 1 through 3 below), none of these companies are currently included in the Perpetual Bond™. It is said that office supply retailers are “often seen as a barometer of economic health” and that the demand for their products has been attenuated by the recent alleged U.S. recession and strong competition from online retailers and warehouse clubs in the same government, business and individual markets.

The Risk Price (SF) for Staples (please see Exhibit 1) is currently $21 and remains well above the current stock price of $13 to $15 which has an estimated downside due to demonstrated volatility of minus ($1.50) (please see our Post, Popoviciu’s Volatility, September 2012, for more details on that calculation). Staples also pays a current dividend of $0.44 per share or $300 million per year for an attractive current yield of 3% but, obviously, that doesn’t help us as investors if the stock price can be up or down by 10% or more at any time. One really needs a better reason for buying and holding or selling the stock, or any stock for that matter, less we only buy and sell on the basis of “The Investor Product” that is routinely sold to “retail investors” (including our pension, trust and endowment funds) by dealers, brokers, analysts and pundits of all sorts on the basis of what sounds good without any guarantee of what is good. Please see our Post, The Investor Product, February 2013, for more on what sounds good and below for more on what is good and guaranteed to all but the hopelessly reckless.

Exhibit 1: (B)(N) SPLS Staples Incorporated – Risk Price Chart

Staples Incorporated operates as an office products company that sells and delivers office products and services. It also operates stores that sell office products and services.

(Please Click on the Chart to make it larger if required.)

The Risk Price (SF) is our estimate of the “least stock price at which a company is likeable” (Goetze 2009) and “likeability” is provably defined by the demonstrated properties of risk aversion (rather than “risk seeking” or “what sounds good” such as “we’ll never see prices this low again – buy now”) – we want to keep our money safe (100% Capital Safety) in the investments that we buy and obtain a hopeful (but not necessarily guaranteed) return above the rate of inflation. For more information, please see our Posts, The Price of Risk, August 2012, and The Nash Equilibrium & Its Stock Price, October 2012.

Accordingly, we only buy or hold a stock at stock prices that are plausibly above the Risk Price (SF) (not below) so that, for example, we bought and held Staples at between $18 and $23 (and cashed our dividends regardless of the ambient stock price volatility) in 2009 and 2010 (the Stock Price (SP), Red Line, above the Risk Price (SF), Black Line in Exhibit 1 above) and otherwise not and we bought, held or sold with our usual methods of price protection in force (please see almost any of these Posts or The Wall Street Put, August 2012). In particular, we sold our holdings in Staples at no less than $23 in mid-2010 and have not owned it since (absent a brief opportunity in late 2010) despite obvious possibilities for risk seeking investments based on volatility and “what sounds good” as the “catch of the day”.

Exhibit 2: (B)(N) ODP Office Depot Incorporated – Risk Price Chart

Office Depot Incorporated is a global supplier of office products and services under the Office Depot brand and other proprietary brand names.

(Please Click on the Chart to make it larger if required.)

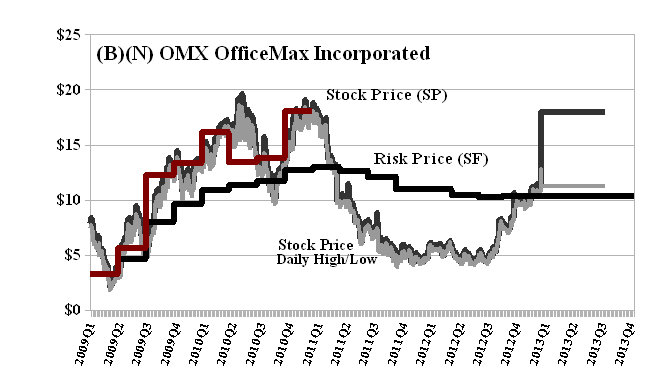

It’s also noteworthy that Office Depot has proposed to buy all of OfficeMax at the Risk Price (SF) by offering 2.69 shares of its common stock (to be issued from treasury) for each share of OfficeMax (which might also pay a special dividend of $1.50 per share or $130 million to its shareholders to “sweeten” the deal). The Risk Price (SF) for Office Depot is currently $3.80 to $3.85 (or $10.20 to $10.40 with the factor of 2.69 per share) and the Risk Price (SF) for Office Max is currently $10.25 to $10.50. The rationale, of course, is that the investment risk of owning the stock of Office Depot should not be greater than owning the stock of OfficeMax based on what is known rather than what might be conjectured. And we’re in good company. This deal was brokered by the firm of J.P. Morgan as the financial adviser and the firms of Skadden, Arps, Slate, Meagher & Flom LLP and Dechert LLP as the legal advisers to OfficeMax. Peter J. Solomon Co and Morgan Stanley were financial advisers to Office Depot’s board and the firm of Simpson Thacher & Bartlett LLP was the legal adviser to Office Depot, and Kirkland & Ellis was the legal adviser to its board. Perella Weinberg Partners also acted as financial advisers to the transaction committee of Office Depot’s board.

Exhibit 3: (B)(N) OMX OfficeMax Incorporated – Risk Price Chart

OfficeMax Incorporated provides office supplies and paper, print and document services, technology products and solutions and furniture to large, medium and small businesses, government offices and consumers.

(Please Click on the Chart to make it larger if required.)

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.