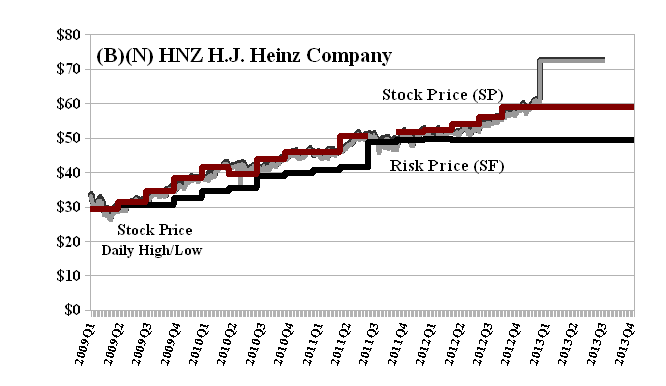

(B)(N) HNZ H.J. Heinz Company

Deal Book. The H.J. Heinz Company is about to be swallowed whole by 3G Capital (which also owns Burger King) and the investment company, Berkshire Hathaway Incorporated (Reuters, February 14, 2013, Buffett, Brazil’s 3G team up for $23 billion Heinz buyout). It’s been in our Perpetual Bond™ portfolio since $30 in 2009 (please see Exhibit 1 below) and, we suppose, we’re going to have to sell it today for the offering price of $72.50 a share plus the current dividend of another $0.52 per share. We’re saddened, of course, because we too like “growth companies” (Buffett’s plan) and “consumer food companies” (3G’s plan) with a current dividend yield of nearly 3% and will just have to find some more of them before they do and buy them with our profits and “their money”, so to speak. We’ll keep you posted and should probably take a look at companies such as General Mills and Campbell’s Soup (please see Exhibit 2 and 3 below) because it looks like 3G and Berkshire Hathaway are prepared to pay premium prices for the “food plan” and might have even more money to spend on it.

The provably “economic” and “fair” value for H.J. Heinz is the Risk Price (SF) of $50 per share or $18 billion although the market suggests $60 or $20 billion and the “new management” suggests $72.50 or $23 billion and “not a penny more” according to the reports (ibid, Reuters. Please see Exhibit 1 below.) although one really doesn’t know where they might get that idea. Perhaps its just a threat, one supposes, since nearly 60 million shares or 20% of the equity changed hands yesterday at prices between $60 and $72.50 and not a penny more although the price is already in dispute (Newswire, February 14, 2013, Buyout Of Heinz – Law Firm Seeks Higher Price For Shareholders).

The Risk Price (SF) is our best estimate of the “price of risk” which is the same as the “least stock price at which the company is likeable” (Goetze 2009) and “likeability” is exactly the “deliberated sentiment” that we, as investors, want to keep our money safe – 100% Capital Safety – and obtain a hopeful return above the rate of inflation. Stock prices above the price of risk express investor commitment to that goal and expectation that the risk price will eventually be that high as the stock price is earned, and, of course, stock price offers (such as $72.50) from the “new management” that are way above the price of risk suggest a vision or Eldorado that is beyond our ken at the present time (Reuters, February 14, 2013, 3G says too early to talk about Heinz cost cuts and Heinz CEO says no talk yet on management changes).

For more information, please see our Posts on The Price of Risk, August 2012, and The Nash Equilibrium & Its Stock Price, October 2012.

Exhibit 1: (B)(N) HNZ H.J. Heinz Company – Risk Price Chart

H.J. Heinz Company manufactures and markets an extensive line of food products throughout the world. Its main products include ketchup, condiments and sauces, frozen food, soups, beans and pasta meals, infant nutrition and other food products.

(Please Click on the Chart to make it larger if required.)

Exhibit 2: (B)(N) GIS General Mills Incorporated – Risk Price Chart

General Mills Incorporated is the manufacturer and marketer of branded consumer foods sold through retail stores. It also supplies branded and unbranded food products to the food service and commercial baking industries.

(Please Click on the Chart to make it larger if required.)

Exhibit 3: (B)(N) CPB Campbell Soup Company – Risk Price Chart

The Campbell Soup Company and its consolidated subsidiaries is a global manufacturer and marketer of branded convenience food products.

(Please Click on the Chart to make it larger if required.)

Both of these companies are currently in the Perpetual Bond™. For a different view of the “growth hormone”, please see our Post, The Last Twinkie, November 2012, on the fabled and troubled Hostess Brands Incorporated which was also taken private and failed to emerge from insolvency and bankruptcy.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.