The Wall Street Put

Drama. There are over seven hundred U.S. companies that trade in New York and have a market capitalization in excess of $1 billion. They include most of the seventy companies of the Dow Jones Industrials, Transports and Utilities, and the broader S&P 500 NYSE and NASDAQ 100 listed companies which, in total, have a market capitalization of about $18 trillion and is comparable to the U.S. National Debt ($16 trillion) which, however, appears to be growing at the rate of about $3 billion per day and has been substantially “funded” by “inflation” for the last several years – that is, the real return on T-bills and the U.S. National Debt has been negative since 2010 and the future remains uncertain – “Monetary policy is a complicated process” (quote attributed to the Fed Chairman, Ben Bernanke) in Forbes, November 11, 2012, The End Of The Bernanke Put? Chairman Sparks Sell Off As He Indicates More QE Is Coming.

In contrast, the average market capitalization of these hard-working companies is about $25 billion of which the largest is the Exxon-Mobil Corporation ($400 billion) and (excusing Apple Incorporated. Please see our recent Post, Microsoft, Apple, Google & The Tech Wars, February 2013.) the next six largest, each weighing in at more than $200 billion but less than $300 billion, are the General Electric Company, Wal-Mart Stores Incorporated, IBM International Business Machines, Johnson & Johnson, Proctor & Gamble Company and Pfizer Incorporated.

If we further restrict our attention to just those companies that also pay a dividend and are currently in the Perpetual Bond™ (B), then we have crafted The Wall Street Put™ which is a portfolio of the largest public companies in America that pay dividends and are, in our opinion, “investment grade” (B) at the present time and that portfolio has returned a remarkable +7.5% in capital gains so far this year – in two months since the end of December – and will return an additional 2%-3% of dividend earnings in the course of the year AND we can guarantee that the return will not be significantly less than that at any time for the rest of the year. In other words, our response to the possible demise of the “Bernanke Put” (ibid, Forbes) is quite different and instead of a “selling spree” and unfounded anxiety that might load us up with “useless” cash earning a for certain negative return, we’re inclined to support a “buying spree” and we know exactly how to do it. (Please see Exhibit 2 & 3 below for the current list of those companies.)

For example, if we do nothing else but enforce the indicated stop/loss prices (please see the $Stop/Loss column in Exhibit 3 below) and all of the 215 companies that are in the portfolio hit those prices at bottom, somehow (and we have no idea how that might happen absent some complicated behaviour of risk-seeking investors), our return (despite the collapse of all those prices) would drop from +7.5% to +7.0% even as we continue to collect our dividends until that happens.

On the other hand, we can also be more proactive and “collar” all of, or selectively, our current prices by buying protective puts against our long position in the stock and selling (or shorting) calls at some opportunistic price above or at the current price (please see our previous Post, The Wall Street Put, August 2012, or almost any of the (B)(N) company Posts for more examples).

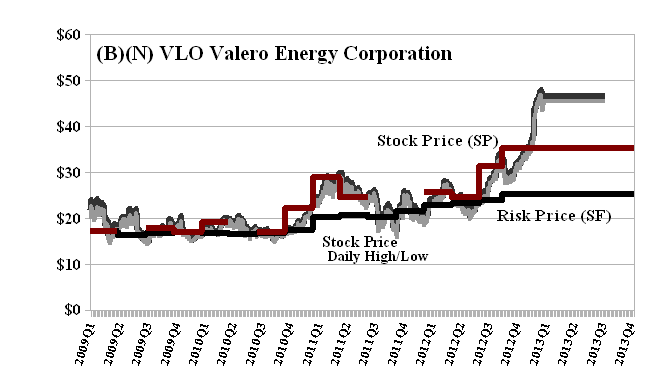

For example, Valero Energy Corporation (please see Exhibit 1 below) is a $25 billion company which stock price has increased by +30% in two months since the beginning of the year (and it is not a candidate for acquisition as far as we know, unlike the “food plan” for growth that has recently affected the H.J. Heinz Company. Please see our recent Post.). The dividend is currently $0.80 per share for an annual payout of $443 million and a current yield of a modest 1.75%. The June put at $45 costs $3.05 today and an offsetting sold or short call at $48 sells for $2.42 so that for a net cost of $0.73 per share ($3.05 less $2.42) today we don’t care what the stock price is for the next three months while we wait for more information, collect our dividends and think about what to do. If it drops below $45 then our put can be “put” or sold to make up the difference and if it rises above $48 then our call will likely be “called” and we might have to give up the stock at $48. (Oh well.) We also note from the chart (Exhibit 1 below) that Valero Energy Corporation has been in the Perpetual Bond™ (B) since early 2012 at much lower prices of around $25.

Exhibit 1: (B)(N) VLO Valero Energy Corporation – Risk Price Chart

Valero Energy Corporation is a refining and marketing company, which produces conventional gasolines, distillates, jet fuel, asphalt, petrochemicals, lubricants, and other refined products as well as a slate of premium products.

(Please Click on the Chart to make it larger if required.)

All the big-cap dividend-paying companies of the U.S. might seem like a lot of companies to own or deal with, but we’re not alone and there are millions of investors who are helping us and routinely tell us what they think these companies might be worth else the stock prices would have no reason to change. (Please see our Posts, The Price of Risk, August 2012, and The Nash Equilibrium & Its Stock Price, September 2012.) Moreover, most brokers are compelled by the competition and electronic trading to charge next to nothing to place a market buy or sell order for, for example, 1,000 shares in the common stock of each of 215 companies that we are prepared to name without further adieu or circumspection. All we need to do is come up with the required $11 million in December (Total line, $10,512,000) or $10 million ($10,210,000) in September last and its worth $11,301,000 now (net of the margin account which is convenient but optional). Please see Exhibit 2 below and for more information on the Chart elements, our recent Post, The Canada Pension Bond™, February 2013.

Exhibit 2: The Wall Street Put™ – Cashflow Summary

(Please Click on the Chart to make it larger if required.)

The illustration shows that we have made no changes in the portfolio since the last twenty-three companies were bought in December and that The Wall Street Put™ is a continuation of a much older Perpetual Bond™ which had a net value of $10,210,000 last September. Please see Exhibit 3 below. Moreover, the total market value of all of these companies is currently about $7 trillion so that, notwithstanding the “money” issue of not enough cash rather than too much cash, there is no reason not to scale the portfolio from 1,000 shares in each company (regardless of the price) to 10,000 shares or 100,000 shares or even 1 million shares ($10 billion) without presuming to take an ownership or controlling interest (“green mail”) in any of these companies.

Exhibit 3: The Wall Street Put™ – Portfolio Summary – February 2013

(Please Click on the Chart to make it larger, and again if required.)

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.