The Power Principle (Econo-physics)

Essay. The science of physics is built on a foundation of undefined terms or “names” such as energy, mass, time, space, and so forth, which derive “meaning” from observation and experiment and the eventual development (or lexicon) of “physical intuition” that shows and sometimes explains, the relationships between the undefined terms or “names”. Obviously, the fewer undefined terms there are, and the more relationships that we can find and verify, the more successful is our theory of physics. For example, whenever a “relationship” is discovered, the number of undefined terms drops by one and a successful theory will also discover necessary properties of the undefined terms that we will then need to verify, if possible. Whereas in the 19th century everybody “knew” what energy, mass, time, distance and so forth were, today, nobody knows but we also know enough to know that we don’t know. (Please see, for example, J.S. Bell, Speakable and Unspeakable in Quantum Mechanics, Cambridge University Press, 1st Edition, 1987)

Our problem is exactly like that. If we assume that investors are risk averse – that they want to save or keep their money and, towards that end, obtain a hopeful return above the rate of inflation – and that risk aversion is a substantial “societal good” and fairly common “preference” as opposed to “gambling” which, one sees, is also a societal good and fairly common preference (please see our Post, The Active Investor (DOA), November 2012), then the utility or usefulness of an investment to a “risk averse” investor is described by a “utility function” of von Neumann-Morgenstern type:

U = SP – SF

where SP is the “stock price” and SF is the “price of risk” which we define as “the least stock price at which the company is likeable” (Goetze 2009) and, therefore, might have a reason to buy it because we “like” it. However, please see our Post, The Price of Risk, August 2012, for more information on how “likeability” is defined and tested and for some examples from our common experience. For example, one could begin with the definition that the “price of risk” is “money now that we can spend or invest” (U=0 and SP=SF) and we need to discover some equivalents that are at least as good and possibly more useful such as “we would “like” definitely more money or the same money, later, when we might need it”. We also note that if the current stock price, SP, is less than the risk price, SF, then the utility is negative and vice versa if the stock price exceeds the price of risk. In the former case, we have paid too little for what we “like” and it’s a “bargain” if we get what we want and in the latter, too much unless we get what we want.

The solution to this equation is defined by a Nash Equilibrium (please see our Post, The Nash Equilibrium & Its Stock Price, October 2012) that assumes nothing at all about stock prices – which is good because we really don’t know anything about stock prices (please see our Post, Stock Prices Are The New Pink, June 2012) – and, as a consequence or relationship, provides us with a form or schema for calculating the “price of risk” which we usually call the Risk Price (SF):

Risk Price (SF) = [V/N*]rms × N*/Share (Power Equation)

In the parlance of von Neumann-Morgenstern, N*/Share is a measure of “risk aversion” – however we define or measure N* and at this point in our discussion, there are no rules – and [V/N*]rms is the quadratic mean of any number of samples or observations of any frequency of its unit price, V/N*, and V is the “market value” of the firm.

In that form, the Risk Price (SF) is a calculation rather than a conjecture and one notes that it has the same form as the remarkable and ubiquitous “Power Equation” of physics, P = Vrms × I, where V is a varying or constant “voltage” and I is a more or less steady “current” in the same time frame as V.

Unlike stock prices, it’s easy enough for us to “feel” the power equation by simply looking at a common light bulb or electric motor (which is a source of resistance or impedance related as R = V/I in the same notation) and observing what happens when we increase the “voltage” whether constant, V, or varying, Vrms, while holding the “current”, I, constant, or the reverse, holding the voltage constant and increasing or decreasing the current. When we put it that way, we notice that “voltage” and “current” do not derive their meaning from the emission of “power” in the light bulb – they are defined and measured in some other way – and it becomes quite remarkable that the visible effect that we call “power” is related to their product in such a simple way because we also use the same term “power” in other contexts such as “horsepower” or “steam power” or “will power” in which we might then be challenged to find out what the analogous or metaphorical “voltage” and “current” are in order to find out what is being “optimized” (as in the sense of the Nash Equilibrium or some other equilibrium such as the Capital Assets Pricing Model (CAPM) which develops the same equation by a different means and objective or utility function). Moreover, one appreciates even more the remarkable fact that the power equation obtains in electrical circuitry of all sorts from microchips and millivolts to nuclear power plants and megawatts, and it’s always the same.

Like the physicists of the 19th century who really believed in time, distance, velocity and so forth, many investors “like” N* to be equal to the “earnings” of the company over some period of time, such as monthly, quarterly, annually or future, and, therefore, N*/Share is equal to the “earnings per share” (EPS) so that the “Power Equation” becomes “Risk Price” (SF) = [PE]rms × EPS where PE = V/N* = (V/Share)/(N*/Share) is the usual “price to earnings ratio” (PE). This becomes even more familiar when we note that [PE]rms² = (Average PE)² + (Standard Deviation PE)² exactly and there is an entire industry engaged in the pursuit of estimating future earnings, PEs and EPSs (please see Thomson Reuters, I/B/E/S).

Thomson Reuters I/B/E/S provides detailed and consensus estimates featuring up to 26 forecast measures including GAAP and pro-forma EPS, revenue/sales, net income, pre-tax profit and operating profit, and price targets and recommendations for more than 60,000 companies in 67 countries worldwide. With I/B/E/S you can leverage the most comprehensive and accurate estimate content from close to 1,200 contributors worldwide. Each contributor is rigorously qualified prior to inclusion to maintain the highest quality content.

Quality Control : Thomson Reuters reviews all estimates according to rigorous quality control measures, both pre- and post-product quality reviews. Quality checks incorporate automated algorithms such as standard deviation, percentage difference from the previous, and number of revisions in a short time period. Monthly audits show accuracy levels greater than 99.9%.

Comparability : Mean estimates only include estimates on the same accounting basis for apples-to-apples comparisons.

That’s excellent work but what, exactly, does it do for our investments? The answer is the same as What did the Rain Dance do for the American Indians? Nothing but it was a great party.

In order to test that result, we note that the price to earnings ratio (PE) for a given company could be anything depending on the stock price (which could be anything but is at least non-negative due to the limited liability of the common shareholder) and the “earnings” which could be negative, zero or positive in any quarter (and let’s use quarterly data because these are generally available for public companies on a timely basis). Most investors rely on a spot estimate of the PE but we could also use a consensus estimate and even throw in multiple spot estimates and even future earnings compared to the current stock price or ambient prices to calculate an estimate of the “voltage” factor [V/N*]rms = [PE]rms and we note as above that [PE]rms = √{(Average PE)² + (Standard Deviation PE)²} which provides us with some basis for “error control” and an opportunity to work with the simple average PE with an “error estimate” if we so desire and if we actually believe that there is such a thing as an “average PE” for a given company.

The second factor, N*/Share = EPS, is then our measure of “risk aversion” and one would think that a higher EPS for a company or for a company in its industry is preferred to a lower EPS but there is no reason for us to be subjective or judgmental; the so-defined

“Gambler’s Ruin” (SF) = [PE]rms × EPS

takes care of that for us. A “high” stock price would then be one that is above the “Gambler’s Ruin” (SF) and provides “positive utility” with respect to our measure of “risk aversion” but any stock price could be “high” if the EPS as realized or expected are low enough and any stock price could be “low” if the EPS are high enough assuming that the [PE]rms is more or less well-known and not directly dependant on the current earnings per share (EPS).

Nevertheless, should we not sell the “high priced” stocks that have positive utility and, hopefully, take profits, and buy or hold only the “low priced” stocks and hold on until they become “high priced”?

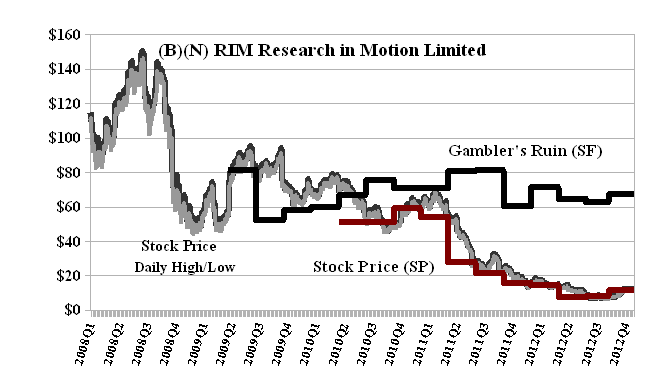

Exhibit 1: (B)(N) RIM Research in Motion Limited – Gambler’s Ruin (SF)

Using this simple policy, the investor never got a chance to sell the “high priced” stock with positive utility that they had “hoped” for but instead owned it all the way down (Red Line below the Black Line) but (or and) still owns it now.

(Please Click on the Chart to make it larger if required.)

The example is not only not unusual but it is to be expected. If we have paid too little for what we “like”, it’s a “bargain” only if we get what we want, and in the reverse case, we have paid too much unless we get what we want and there appears to be nothing in PEs or EPSs that is relevant to what we want – we want to keep our money with a hopeful return above the rate of inflation.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.