(B)(N) S&P TSX Quintessential Perpetual Bond

We follow about three hundred companies in the S&P TSX with a combined market capitalization of about $1.6 trillion which is said to represent about 70% of the market capitalization of all the Canadian public companies and all of those with a market capitalization of $1 billion or more. In world terms, of course, $1.6 trillion is not a lot of money (please see our Post, Numbers 20:12, August 2012, for some insight into how competitive and desperate investing really is) and, moreover, the market as measured by the S&P TSX Composite Index has returned a very tepid and unexpected +3% this year and is finishing up at about the same level as at the end of 2009, three years ago, despite the early optimism of the first few months of this year (2012) and the likely early (and unfounded) optimism of investors in the coming year (2013).

Not to worry. The thirty four companies of the S&P TSX Quintessential Perpetual Bond™ with a combined market capitalization of $225 billion are up +18% this year, plus another 2% to 3% of dividends that we have earned but not included, and we have similar results in the much larger NYSE markets of the Dows, the NASDAQ 100 and the S&P 500 that could easily absorb a lot more of our investment capital. In fact, ten times as much but that is still barely enough to advance the interests of vast accumulations of “money” that needs to earn income in the pension funds, trust and endowment funds, and the private capital of wealthy investors.

For example, there are many investors who hoped – however unfounded and unreasonable – for double digit returns this year (and, possibly, every year) but are being handed double digit losses in exotic locales, exotic and “experimental” investments and the even more exotic and experimental investment styles of world class leaders in the exotic profession of “wealth management” ($3 trillion worth according to Reuters, December 19, 2012, Too big to fail? China’s wealth management products stir debate). Undoubtedly, there is a lot of “wealth management” going on but it is just not ours (nor is it theirs any more) absent the only thing that we need to look for in our investments – 100% Capital Safety guaranteed and a hopeful return above the rate of inflation. How hard is that?

The RiskWerk Company S&P TSX Quintessential Perpetual Bond™ is a managed portfolio of equities and began the year with sixty more companies that we sold in the course of the year on plausible or likely (B)- to (N)-transitions. Buying the stocks is easy. If they’re a (B) we are prepared to buy and hold them regardless of the purchase price when we buy them. However, selling them, and taking profits, is a discipline and a process that is not reflected in the simplified Cash Flow Statement (please see Exhibit 1 below and for more details on the selling discipline, The Wall Street Put, August 2012 or nearly any of the company (B)(N) discussions). Moreover, in our view, “wealth management” is not so much about what we buy but how we sell it and what we do with the profits and earned dividends that had better be there.

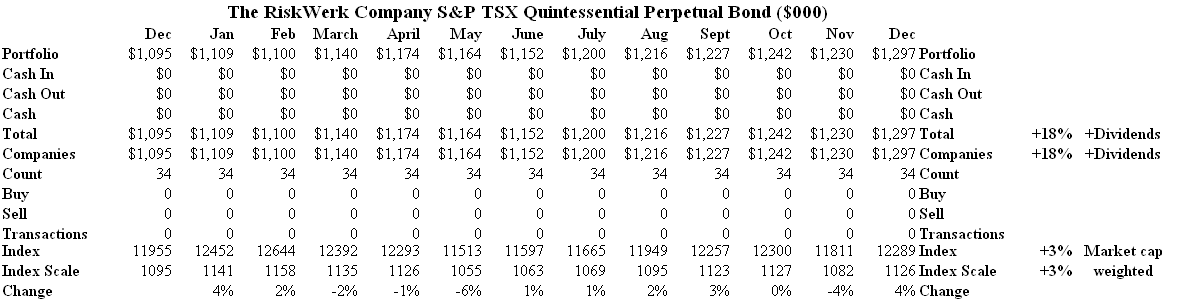

Exhibit 1: The RiskWerk Company S&P TSX Quintessential Perpetual Bond™ – Cash Flow

The RiskWerk Company S&P TSX Quintessential Perpetual Bond – Cash Flow

The Portfolio Chart (Exhibit 2 below) summarizes the current S&P TSX Quintessential Bond™ which will be carried into 2013 pending any plausible (B)- to (N)-transitions that we do not have any reason to revise until new balance sheet information becomes generally available. In the meantime, the most important entries in the table are the “$GAP” and Stop/Loss amounts and prices.

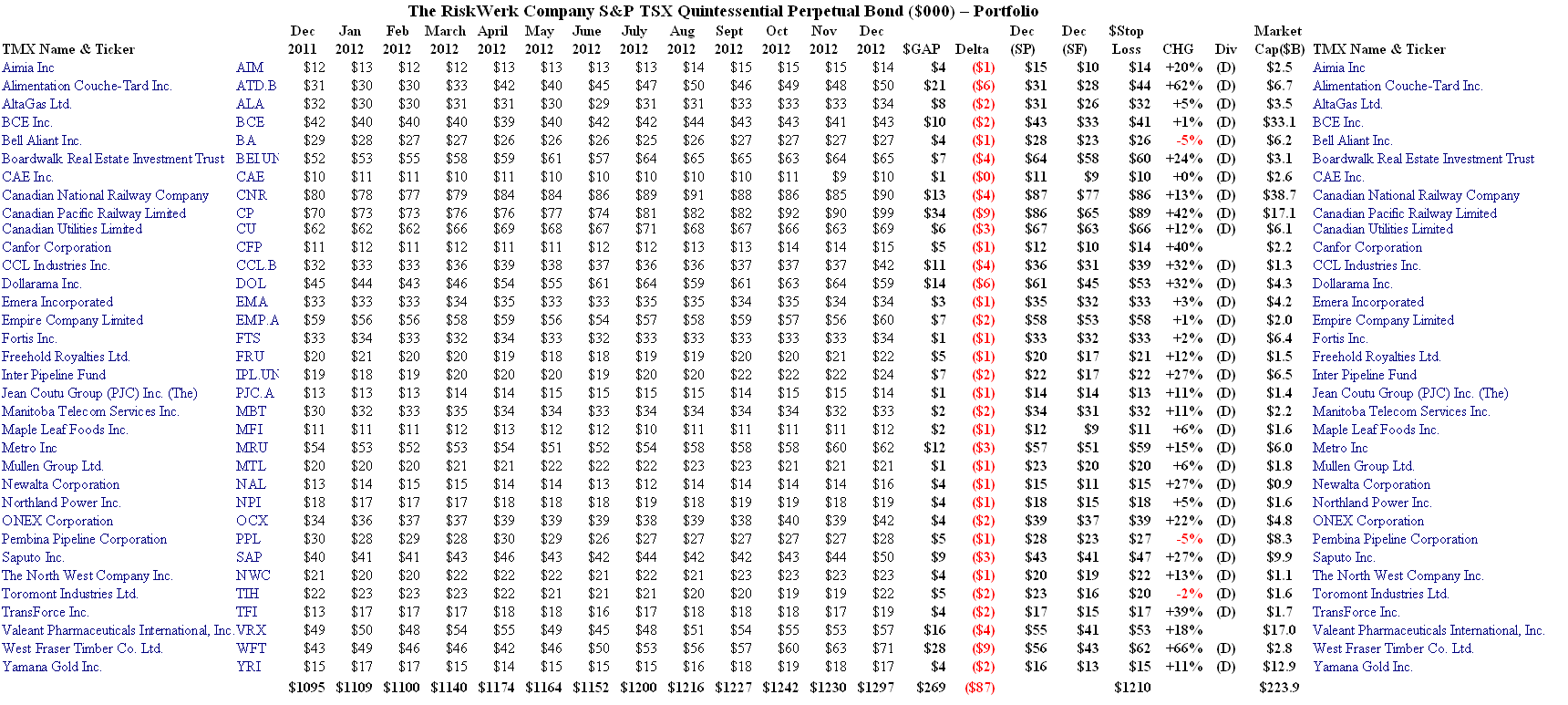

For example (please see Exhibit 2 below), we purchased AIM Aimia Incorporated (which offers loyalty services such as Coalition Loyalty, Proprietary Loyalty and Loyalty Analytics) at $12 in December last year and have held it the entire year at prices between $12 and the current $14 to $15 for a stock price gain of +20% and earned dividends of $0.64 per share and a yield of more than 5%.

The “$GAP” is the excess of the current Stock Price (SP) over the Risk Price (SF) and is currently $4 to $5. The “$GAP” needs to be earned or closed by the expected – as in provably “expected” by the risk averse investors who own the stock at these prices and won’t accept less – future performance of the company because stock prices above the price of risk are a provably “economic free good” and should not exist (in a perfect world). Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more details.

The other important estimate is the “Delta” which is our estimate of the stock price downside that we might expect due to demonstrated volatility (please see our Post, Popoviciu’s Volatility, September 2012) and there is either a “$Stop/Loss” in effect which is the current stock price less the “Delta” or we have “collared” the current price using the put and call options market. For example, today’s stock price is $15 and the January put at $15 costs $0.20 per share. We can partially offset the cost of buying the long put by shorting (or selling) the opportunistic January call at $16 for $0.10 per share so that for a net cost of $0.10 per share ($0.20 less $0.10) we can lock in our current price at no less than $15 per share and no more than $16 per share for the next month while we think about this situation. Please Exhibit 3 below for more details of this example.

Exhibit 2: The RiskWerk Company S&P TSX Quintessential Perpetual Bond™ – Portfolio

(Please Click on the Chart to make it larger and again if required.)

Exhibit 3: (B)(N) AIM Aimia Incorporated – Risk Price

Aimia Incorporated (formerly, Group Aeroplan) offers a full-suite of loyalty services including Coalition Loyalty, Proprietary Loyalty and Loyalty Analytics.

(Please Click on the Chart to make it larger if required.)

A company is entitled to be in the Perpetual Bond™ if and only if the ambient stock prices summarized as the Stock Price (SP) at which we buy, hold or sell the stock, are plausibly above the price of risk or Risk Price (SF) (dark Black Line, which is a step-function and depends on generally available balance sheet data. There are no “forecast” or “conjectural” data used.)

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.