(B)(N) DII.B Dorel Industries Incorporated

Drama. Dorel Industries is based in Montreal, Quebec, and has about 5,000 employees and global markets for its brand-name recreational and home products. The company has prudently slowed down its bicycle production because of a tough market due to inclement and unpredictable weather and its competitors are slashing prices in order to move more of their inventory (The Canadian Press, June 13, 2013, Dorel to cut 50 jobs as poor weather expected to hurt bike segment results).

Courtesy: Dorel Industries

Like Bombardier, the company has a dual class share structure with a public float of about 27 million shares in the Class B stock and an ownership class of 4 million Class A shares; it pays each class of stock the same dividend of $0.30 per share per quarter for a payout of $33 million this year and a current yield of 3.4%, and it’s also anticipating to slowly buy in and cancel 850,000 shares or about 3% of the public float during the next year.

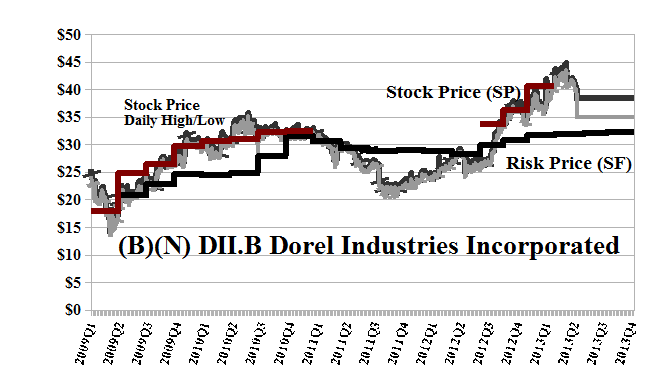

It re-entered the Perpetual Bond™ at $34 last year and we’ve been stopped out (forced stop/loss sales) at $40 in March but the stock remains above the price of risk and we can afford to re-purchase our shares at lower prices. Please see Exhibit 1 below, Red Line Stock Price (SP) above the Black Line Risk Price (SF) and for no other reason.

There’s no options market in the stock and our estimate of the demonstrated downside volatility in the stock price is as much as minus ($5) per share so that we would not be surprised by any price between the current $35 and $30 to $40 in the next several months.

Exhibit 1: (B)(N) DII.B Dorel Industries Incorporated – Risk Price Chart

Dorel Industries Incorporated is a consumer products company which designs, manufactures or sources, markets and distributes a diverse portfolio of powerful product brands, marketed through its Juvenile, Recreational/Leisure and Home Furnishings segments.

(Please Click on the Chart to make it larger if required.)

From the Company: Dorel Industries Incorporated manufactures and sells juvenile products, bicycles, and furniture worldwide. It operates in three segments: Juvenile, Recreational/Leisure, and Home Furnishings. The Juvenile Segment manufactures and imports products, such as infant car seats, strollers, high chairs, toddler beds, playpens, swings, furniture items, and infant health and safety aids. This segment markets its products under the Cosco, Safety 1st Maxi-Cosi, Quinny, Bébé Confort, Baby Relax, BABY ART, Bertini, and Mothers Choice, as well as Disney and Eddie Bauer brands. The Recreational/Leisure segment offers bicycles, bicycling and running footwear and apparel, jogging strollers, bicycle trailers, childrens electric ride-ons, and toys, as well as related parts and accessories under the Schwinn, Mongoose, Roadmaster, Iron Horse, InStep, Schwinn, and KidTrax brands. The Home Furnishings segment provides ready-to assemble furniture for home and office, as well as metal folding furniture, futons, mattresses, bunk beds, step stools, hand trucks, specialty ladders, and other imported furniture products. This segment markets its products under the Ameriwood, Altra, System Build, Ridgewood, DHP, Dorel Fine Furniture, and Cosco brands. The company sells its products to mass merchant discount chains, specialty stores, department stores, club format outlets, hardware/home centers, independent stores, sporting goods stores, and Internet retailers. It owns and operates 70 retail stores in Chile and Peru. Dorel Industries Incorporated was founded in 1962, has 5,400 employees, and is headquartered in Montreal, Canada.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2006) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks. Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.Disclaimer Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.