Lemons to Juice

Deal Book. The Street has been bombed again by “anomalies” in the investor “thought process” and can’t explain the lack of appetite for three “perfect” companies that ought to be getting big price gains, but aren’t: the companies are Salesforce.com Incorporated, Radian Group Incorporated, and AMN Healthcare Services Incorporated (The Street, June 5, 2013, Cramer: How Perfect Stocks Morph Into Lemons).

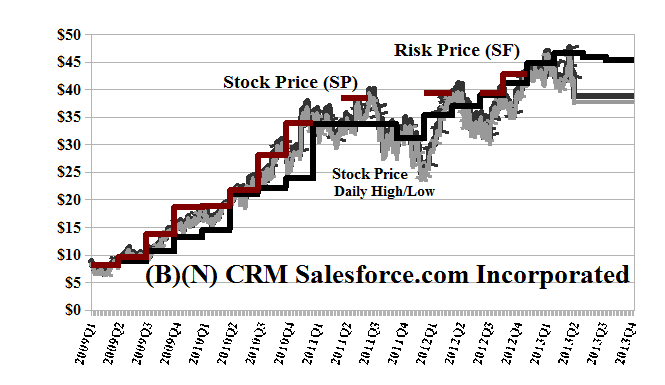

We looked at Salesforce.com last week (please see Exhibit 1 below) and the lack of support for the stock price has morphed into an “air pocket” after the “stunning” (ibid, The Street) acquisition of the like-minded digital marketer, ExactTarget Incorporated (ET), for $33.75 per share which is a +53% premium over the closing stock price of only $22 the day before.

The deal will cost $2.5 billion and is set to close in July but – reality check – $2.5 billion is half the total assets and $300 million more than all of Salesforce’s sales in 2012 for which it also posted a loss of ($250 million).

On the other hand, the stock market value of Salesforce is $25 billion and we could think about lending them another “dime”, so to speak, so that they can complete this deal, save the company, and, possibly, save the stock price for us all; for example, could Salesforce “pump” or “sell” the deal and float 10% of its own equity into the stock market, or to ExactTarget’s shareholders, to pay for it, or will it need to add another $2.5 billion to its current debt of $3.2 billion and another $1 billion to its already awesome $1.5 billion of “goodwill”?

We’ll just have to wait and see, but we don’t own any of the stock at the present time (please see Exhibit 1 below; Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason).

Exhibit 1: (B)(N) CRM Salesforce.com Incorporated – Risk Price Chart

(B)(N) CRM Salesforce com Incorporated – June 5, 2013

Salesforce.com Incorporated provides enterprise cloud computing solutions, offering social and mobile cloud apps and platform services, as well as professional services to facilitate the adoption of its solutions.

(Please Click on the Chart to make it larger if required.)

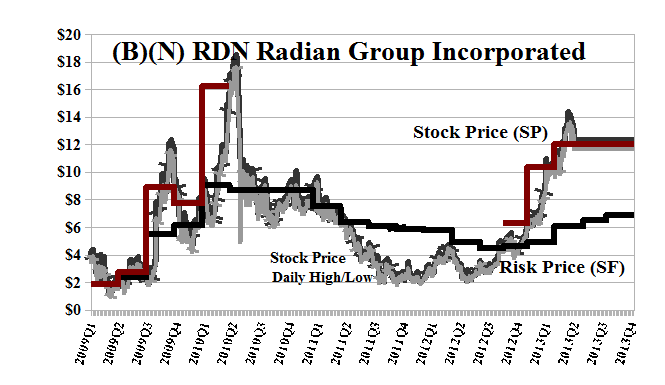

The Radian Group (please see Exhibit 2 below) insures mortgages; it’s basically a “desk” and a “telephone” with $6.4 billion in total assets, $7 million of fixed assets, negligible equity of $ 900 million (down from $2 billion in 2009), and a market value of $2 billion; the company pays a dividend of $2 million a year to its shareholders for a current yield of 10 basis points (1/10th of 1 percent).

The price drop from $19 to $6 in less than a month in early 2010 might have been related to a quarterly loss of $300 million that eventually grew to $1.8 billion for the year, but the shareholders must be used to that by now because it’s only made a profit once in the last five years.

The demonstrated stock price volatility is minus (-$3) per share so that we would not be surprised at any price from the current $12 to $9 or $15. It’s eligible for the Perpetual Bond™ (Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason) and we’ve bought the July put at $12 for $0.85 per share from our profits and partially offset the cost of that by selling the July call at $13 for $0.65 per share so that for the cost of holding the stock at $12 and the collar at $0.20 per share ($0.85 less $0.65), we can see how this plays out at between $12 and $13 per share, guaranteed, in the current season of hot new Fed rates.

Exhibit 2: (B)(N) RDN Radian Group Incorporated – Risk Price Chart

(B)(N) RDN Radian Group Incorporated

Radian Group Incorporated through its subsidiaries and affiliates, provides credit-related insurance coverage and financial services to mortgage lenders and other financial institutions.

(Please Click on the Chart to make it larger if required.)

From the Company: Radian Group is a credit enhancement company with a primary focus on domestic, first-lien residential mortgage insurance. The company’s business segments are mortgage insurance and financial guaranty. The mortgage insurance segment provides credit-related insurance coverage, principally through private mortgage insurance, and risk management services to mortgage lending institutions. The financial guaranty segment has provided direct insurance and reinsurance on credit-based risks. The company has discontinued writing any new financial guaranty business but it maintains a sizable financial guaranty insured portfolio, consisting of public finance and structured finance risks. The company has 700 employees and is headquartered in Philadelphia, PA.

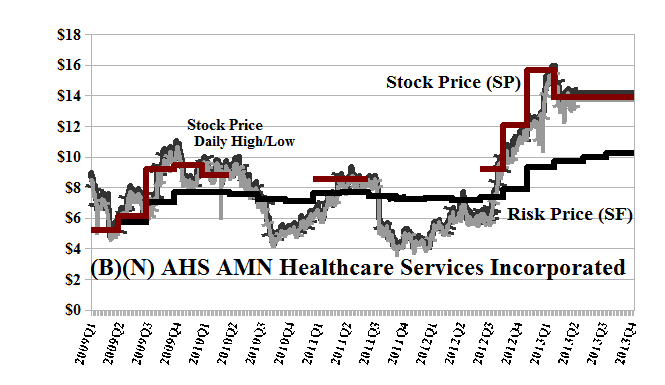

AMN Healthcare Services Incorporated is another “great” growth company sinking on its own merits – sales of about $1 billion, no dividends, and losses for three of the last five years. We picked it up at $10 last year (please see Exhibit 3 below, Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason) and it’s trading now at $14 and still well above the current Risk Price (SF) of $10 and rising.

The demonstrated downside in the price due to volatility is minus (-$2.50) so that we would not be surprised by a price as low as $11.50 or as high as $16.50 in the next several months. There are no options to speak of so we’ve set the stop/loss at $13 and sold a call against our long position at $16 in July for $0.50 (making our own dividends, so to speak, on a “growth” stock) and might hang on for $13 to $16 and $3 or more in profits, and a +30% or more return should the healing process continue.

Exhibit 3: (B)(N) AHS AMN Healthcare Services Incorporated – Risk Price Chart

(B)(N) AHS AMN Healthcare Services Incorporated

AMN Healthcare Services Incorporated is a healthcare staffing company which recruits and places physicians, nurses and allied health professionals nationally and internationally on a temporary or permanent basis at healthcare facilities throughout the US.

(Please Click on the Chart to make it larger if required.)

From the Company: AMN Healthcare Services Incorporated provides healthcare workforce solutions and staffing services to healthcare facilities in the United States. The Nurse and Allied Healthcare Staffing segment offers a range of clinical workforce solutions, including a comprehensive managed services workforce solution that enables users to manage the contingent needs for a client; a recruitment process outsourcing program that leverages support systems to replace or complement a clients existing internal recruitment function for permanent staffing needs; and traditional staffing service solutions of local, and short and long-term assignment lengths. This segment also provides a shorter-term staffing solution of four to eight weeks under its NurseChoice brand to address hospitals urgent need for registered nurses; and allied health professionals under Med Travelers, Club Staffing, and Rx Pro Health brands to acute-care hospitals and other healthcare facilities. The Locum Tenens Staffing segment places independent contractors physicians of various specialties, certified registered nurse anesthetists, nurse practitioners, physician assistants, and dentists on a temporary or locum tenens basis with various healthcare organizations, including hospitals, medical groups, occupational medical clinics, individual practitioners, networks, psychiatric facilities, government institutions, and managed care entities under the Staff Care and Linde Healthcare brand names. The Physician Permanent Placement Services segment provides physician permanent placement services under the Merritt Hawkins and Kendall & Davis brand names to hospitals, healthcare facilities, and physician practice groups in the United States. It serves acute and sub-acute care hospitals, government facilities, community health centers and clinics, physician practice groups, and other healthcare settings. AMN Healthcare Services Incorporated was founded in 1985, has 1,700 employees, and is headquartered in San Diego, California.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks. Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.Disclaimer Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.