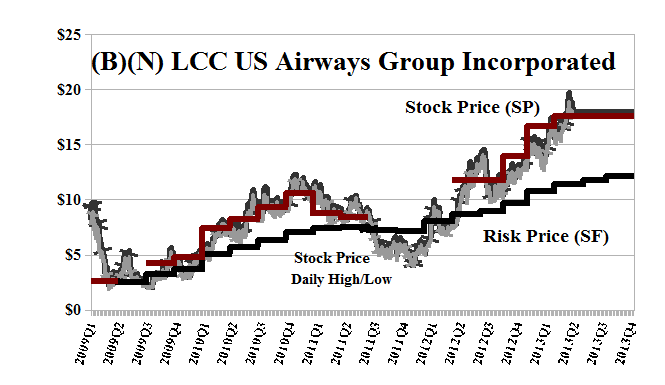

(B)(N) LCC US Airways Group Incorporated

Deal Book. US Airways and American Airlines (AMR Corporation) are in the process of merging and there’s so much red (losses and deficits), blue (route plans) and grey (unknowns) in the deal that we are minded of Napoleon’s Armies trekking back from Moscow in the Winter of 1812, just 200 years ago (PRNewswire, March 4, 2013, American Airlines and US Airways Receive Request From DOJ In Connection With Proposed Merger).

Napoleon’s Army in Retreat from Moscow December 1812

Wikipedia: Adolph Northen (1828–1876)

US Airways has 32,000 employees and is much smaller than American Airlines with 78,000 employees, but US Airways has the money and the combined companies pro forma will have total assets of $34 billion, total liabilities of $40 billion, and a shareholders equity of minus (-$6.6 billion) for which investors are willing to pay $4.5 billion in the open stock market for both companies.

Neither company pays a dividend and US Airways has more or less steady revenues of $13 billion per year, but is still in a net loss position since 2008; and American Airlines has more or less steady revenues of $24 billion per year on which it has lost about $2 billion a year since 2008 inclusive (5 years) but we would hope that with a combined revenue of about $37 billion the combined company would be able to staunch a loss of $2 billion a year.

That’s about 5% of the gross revenue and a margin typical of grocery stores, but that doesn’t mean that it’s easy; for example, Wal-Mart had gross sales of $470 billion last year and a net income of $17 billion (3.6% profit) but Supervalu had sales of $18 billion and a loss of ($1.5 billion).

And it’s also noteworthy that 5% was the return rate on Napoleon’s Army of over 400,000 and he took no prisoners, as today’s managements are constrained to do.

If we follow the money, the mutual funds do not have a large interest in either company but there are ten institutions that each hold between 2% and 10% of US Airways for a combined holding of 43% of which Fidelity Management and Research Company has the largest position at about 10%. In AMR, only Fidelity Management and Research Company holds as much as 2% since ICC Capital Management sold 3% and 12.5 million shares of its interest in March.

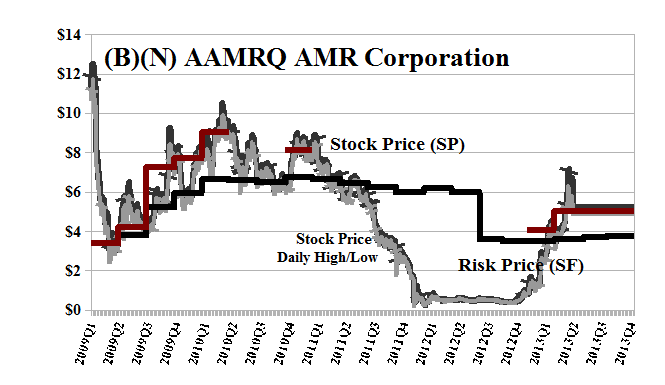

Our understanding of the situation would then be that the institutions reasonably expect that the US Airways model will be the winner; and that many small shareholders began buying AMR at the bargain prices of $0.50 per share last year and are now holding a $5 stock and waiting for the takeover price (which, would be fairly set at the Risk Price (SF) of $4).

We are then prepared to be sold out from our AMR position (please see Exhibit 2 below) and can also afford a stop/loss on US Airways at the current stock price of $17 to $18 less the indicated price volatility of minus (-$2.50). If the stock were paying a dividend, we would think about a collar but we only benefit from an upside in any case.

Exhibit 1: (B)(N) LCC US Airways Group Incorporated – Risk Price Chart

(B)(N) LCC United Airways Group Incorporated

US Airways Group Incorporated is a network air carrier through its wholly owned subsidiaries. The Company operates the airline in the United States as measured by domestic revenue passenger miles and available seat miles.

(Please Click on the Chart to make it larger if required.)

From the Company: US Airways, along with US Airways Shuttle and US Airways Express, operates more than 3,000 flights per day and serves 198 communities in the U.S., Canada, Mexico, Europe, the Middle East, the Caribbean, Central and South America. The airline employs more than 32,000 aviation professionals worldwide, operates the world’s largest fleet of Airbus aircraft and is a member of the Star Alliance network, which offers its customers more than 21,900 daily flights to 1,329 airports in 194 countries. Together with its US Airways Express partners, the airline serves approximately 80 million passengers each year and operates hubs in Charlotte, N.C., Philadelphia, Phoenix and Washington, D.C. Aviation Week and Overhaul & Maintenance magazine presented US Airways with the 2012 Aviation Maintenance, Repair and Overhaul (MRO) of the Year Award for demonstrating outstanding achievement and innovation in the area of technical operations. Military Times Edge magazine named US Airways as a Best of Vets employer in 2011 and 2012. US Airways was, for the third year in a row, the only airline included as one of the 50 best companies to work for in the U.S. by LATINA Style magazine’s 50 Report. The airline also earned a 100 percent rating on the Human Rights Campaign Corporate Equality index for six consecutive years. The Corporate Equality index is a leading indicator of companies’ attitudes and policies toward lesbian, gay, bisexual and transgender employees and customers.

Exhibit 2: (B)(N) AAMRQ AMR Corporation – Risk Price Chart

(B)(N) AAMRQ AMR Corporation – May 2013

AMR Corporation, through its subsidiaries, operates in the airline industry.The main subsidiary of AMR, American Airlines, Inc. or American provides scheduled jet service to approximately 160 destinations.

(Please Click on the Chart to make it larger if required.)

From the Company: American Airlines focuses on providing an exceptional travel experience across the globe, serving more than 260 airports in more than 50 countries and territories. American’s fleet of nearly 900 aircraft fly more than 3,500 daily flights worldwide from hubs in Chicago, Dallas/Fort Worth, Los Angeles, Miami and New York. American flies to nearly 100 international locations including important markets such as London, Madrid, Sao Paulo and Tokyo. With more than 500 new planes scheduled to join the fleet, including continued deliveries of the Boeing 737 family of aircraft and new additions such as the Boeing 777-300ER and the Airbus A320 family of aircraft, American is building toward the youngest and most modern fleet among major U.S. carriers. American’s website, AA.com®, provides customers with easy access to check and book fares, and personalized news, information and travel offers. American’s AAdvantage® program, one of the most popular frequent flyer programs in the world, lets members redeem miles for flights to almost 950 destinations worldwide, as well as flight upgrades, vacation packages, car rentals, hotel stays and other retail products. The airline also offers nearly 40 Admirals Club® locations worldwide providing comfort, convenience, and an environment with a full range of services making it easy for customers to stay productive without interruption. American is a founding member of the oneworld® alliance, which brings together some of the best and biggest airlines in the world, including global brands like British Airways, Cathay Pacific, Iberia Airlines, Japan Airlines, LAN and Qantas. Together, its members serve more than 840 destinations served by some 9,000 daily flights to nearly 156 countries and territories.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.