America’s Most Unwanted Companies

Drama. Fortunately, the North American markets are all significantly up for the first month of 2013 and regardless of the news, “concerns” and some investor anxiety that they’re not getting enough, soon enough (for example, Reuters, January 6, 2013, Einhorn sues Apple, marks biggest investor challenge in years and our recent Post on (B)(N) AAPL Apple Incorporated, February 2013), there are many companies that just keep on producing and those that don’t “produce” or fail in some egregious way, acquire the infamy of “America’s Most Unwanted” or “Least Liked” or “Undesirable Aliens”. What happened last year, we ask rhetorically, to such brand names as J.C. Penney, Dish Network Corporation, T-Mobile USA (a division of Deutsche Telekom), Facebook Incorporated, Citigroup Incorporated, Research In Motion Limited, American Airlines (owned by AMR), Nokia Corporation (ADS), Sears Holding Company, and the Hewlett-Packard Company? For more details of these failures and “incorporate corporates” that have failed so badly in just one year, please see the on-line journal 24/7 Wall Street, January 11, 2013, 10 most hated companies in North America. Corporations can anger their customers, fail their shareholders, and mistreat their employees and many of our previous Posts.

For example, “J.C. Penney went from being a mediocre national retailer with modest challenges to one of the great public company management disasters of the last few years.” – ibid, 24/7 Wall Street.

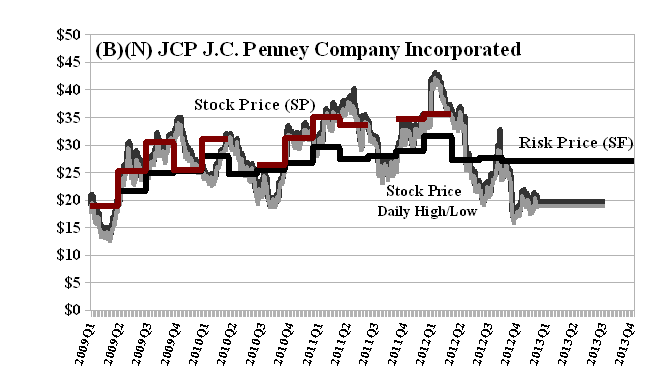

Exhibit 1: (B)(N) JCP J.C. Penney Company Incorporated – Risk Price Chart

J. C. Penney Company Incorporated is a holding company whose business consists of selling merchandise and services to consumers through its department stores and Direct channels. It sells family apparel and footwear, accessories, fine and fashion jewellery, furniture, bed & bath, and for the home in well-known brands.

(Please Click on the Chart to make it larger if required.)

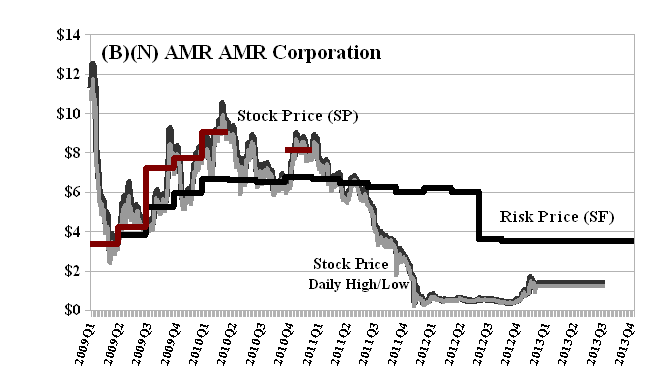

Or, “AMR, parent of American Airlines, has, in a remarkably short period of time, ruined its relationships with shareholders, bondholders, pilots, customers, suppliers, and most of its other employees. The November 2011 Chapter 11 filings of AMR virtually wiped out shareholders.” – ibid, 24/7 Wall Street.

Exhibit 2: (B)(N) AMR AMR Corporation – Risk Price Chart

AMR Corporation operates in the airline industry through its subsidiaries. The main carrier is American Airlines which provides scheduled jet service to approximately 160 destinations.

(Please Click on the Chart to make it larger if required.)

What can we say (please see Exhibit 1 and 2 above) but, Where is Mom & Pop to run these companies as if they loved them? Two “holding companies” and two disasters that are a fair warning to the sponsors and directors of the latest fads in “hedge funds” and “alternative investments” for the well-heeled pension plans with lots of our cash to buy “things” that we eventually pay for, again.

“Likeability” is not just about competence and good intentions or good luck and good “economics” but it is a measurable and actionable economic good that demonstrates investment risk as both volatility and uncertainty and although one might hope that an investment is the purchase of something that retains and hopefully increases in value, it is that hope rather than that certainty that suggests that an investment is just and only the “purchase of risk” (and hope) and like any other purchase that we might make, we ought to know to price of it, that is, we ought to know the “price of risk” if we are to be “investors” and not merely gamblers. Please see our Posts, The Price of Risk, August 2012, and The Nash Equilibrium & Its Stock Price, October 2012, for more information on “risk” as a “societal good”.

The price of risk is provably “the least stock price at which a company is likeable” (Goetze 2009) and “likeability” (in our case) is exactly the demonstration that investors with a strong sense of risk aversion – we want to keep our money and obtain a hopeful return above the rate of inflation – are committed to buying and holding this stock at those prices, and otherwise not.

Accordingly, we only buy or hold a stock if the ambient stock prices as represented by the Stock Price (SP) (Red Line, a step-function in Exhibit 1 and 2) appear to be at or above the “price of risk” or Risk Price (SF) (Black Line) which is also a step-function updated at most quarterly as new balance sheet information becomes generally available.

For example, with reference to Exhibit 1 and 2 above, we owned J.C. Penney between $25 and $35 in 2010 and 2011 and not thereafter, selling the last of our holdings at $36 in mid-2012, and we haven’t owned AMR since between $4 and $8 in 2009 and 2010. News and information investors, on the other hand, have suffered a different fate attending investment angst and have no idea why that might be the case or why the stock price is what it is or was. (Please see our Post, The Active Investor (DOA), November 2012.) For example, some investors bought J.C. Penny at $40 last year and other investors bought it from them at $30 six months later and possibly $20 this year and some investors bought AMR at $6 last year and other investors bought it from them for $0.50 (50¢) in December and might have tripled their money by mid-January if only they had as much reason to sell between fear, hope and greed as they might have had to buy.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.