(B)(N) NVE NV Energy Incorporated

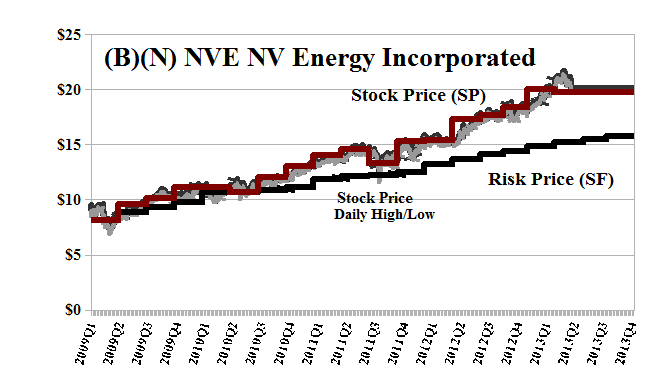

Deal Book. Berkshire Hathaway Incorporated’s subsidiary, MidAmerican Energy, bought Nevada’s largest electric utility, NV Energy Incorporated, today for $5.6 billion, or $23.75 per share which is a +20% premium on the current stock price of $19.75 and a +50% premium on the current Risk Price (SF) of $16 (Reuters, May 29, 2013, Buffett picks up Las Vegas-based NV Energy for $5.6 billion).

MidAmerican Energy is entirely Iowa-based and about five times the size of NV Energy, and the head offices of the two companies are separated by at least three states whether we go north or south (please see the map), but the deal is expected to help NV Energy retire its coal-fired plants and replace them with renewable energy and gas-fired plants (ibid, Reuters).

Source: Wikipedia: Nevada & Iowa

NV Energy was paying a dividend of $0.19 per share per quarter, or $180 million per year to its shareholders for a current yield of 3.9%. That amount, $180 million, is more than 60% of last year’s income (after tax) which was $322 million, but has been as low as $160 million to $180 million in recent years.

Dividends, of course, are no longer an issue, but the interest on $5.6 billion, would be $100 million per year at 2% (if we can get it) and NV Energy also has existing liabilities of $8.3 billion on which it paid $300 million in interest last year.

At the Risk Price (SF) of $16, the company is “valued” at $3.7 billion and that’s “as good as cash” and “better than money”, which is the meaning of the price of risk (please see the references below). But we can’t buy it for that price if the investors who are buying and holding the stock at $20 believe that the company is or will be “worth” $20 to them on the same basis – “as good as cash” and “better than money”; and if we’re only offering $20, why should they sell it to us?

In practical terms, NV Energy has total assets of $11.8 billion, total liabilities of $8.3 billion, and a shareholders equity of the difference, $3.5 billion. Moreover, at $16, the dividend yield would shoot up by 25% to 4.5% or more, which certainly exceeds the current familiar rate of inflation of about 2% (or less) to perhaps 2.5% in the foreseeable future. And so, $16 is right on the money, and even a bit cheap or “opportunistic” which one might expect if there is a “meeting of the minds” between “risk seeking” and “risk averse” investors. Please see our Post, Bystanders & Collateral Damage, April 2013, for more insight into that observation.

But all of that is still true at $24 which is the purchase price of all the earnings in an environment in which “money” as “cash” has a depreciating value. Best to buy something that is “as good as cash” and “better than money”, such as The Wall Street Put before they’re all gone.

Exhibit 1: (B)(N) NVE NV Energy Incorporated – Risk Price Chart

(B)(N) NVE NV Energy Incorporated

NV Energy Incorporated is an investor-owned holding company. Its utilities operate three business segments: NPC electric, SPPC electric and SPPC natural gas in the state of Nevada.

(Please Click on the Chart to make it larger if required.)

From the Company: NV Energy Incorporated together with its subsidiaries, engages in the generation, transmission, distribution, and sale of electric energy in Nevada. The company generates electricity from its gas, oil, and coal generating units. It also delivers natural gas service. As of December 31, 2012, the company served approximately 850,000 electric customers primarily in Las Vegas, North Las Vegas, Henderson, and adjoining areas; 324,000 electric customers in the western, central, and northeastern Nevada, including the cities of Reno, Sparks, Carson City, and Elko; and approximately 153,000 customers with natural gas service in Reno/Sparks area of Nevada. It has a generation capacity of approximately 6,078 megawatts through 61 generating units. NV Energy, Inc. serves residential, commercial, and industrial customers, as well as gaming/recreation, mining, warehousing/manufacturing, and governmental entities. The company was formerly known as Sierra Pacific Resources. NV Energy, Inc. was founded in 1906, has 2,700 employees, and is headquartered in Las Vegas, Nevada.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.