(B)(N) HTZ Hertz Global Holdings Incorporated

Deal Book. The stock of Hertz Global Holdings has jump-started since acquiring the much smaller, and possibly struggling, Dollar Thrifty Automotive Group, in November last year for a cash offer of $87.50 per share, or $2.5 billion, which is a bargain at only a +10% premium on the stock which had been bouncing around between $70 and $80 for the year previous, and the deal closed within a near record time of less than three months, in contrast to some of the other deals that we’ve seen in the last year. We don’t know why an entire car when and where we need it, is less strategic than the oil and gas in it. For example, please see our Post, The All Canadian Four Play, October 2012.

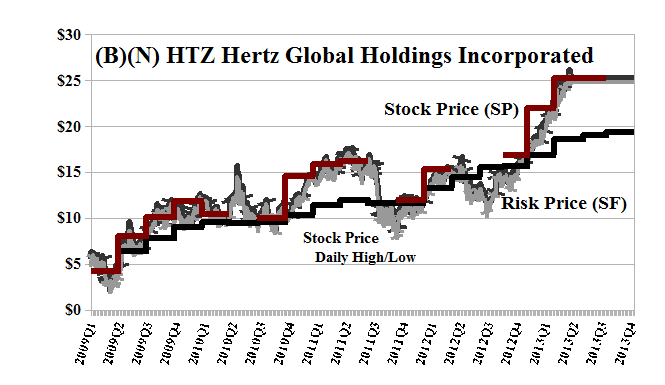

Barron’s also likes that new car smell and has gushed that the stock of Hertz could increase by another +70% in the next two years, which got us to wondering what it’s all about (Barron’s, May 26, 2013, Hertz stock could rise 70 percent in two years). Please see Exhibit 1 below.

Hertz became eligible for the Perpetual Bond™ in September 2012, just about the same time that it announced a tender offer for the Dollar Thrifty Group, and it promptly blew away our collar at lower prices. We’ve been riding bareback in a solid profit position ever since with just a stop/loss at minus (-$4) per share, reflecting a possible quarterly price volatility that should not surprise us.

Barron’s obtained its price target of $43 by projecting the expected earnings of $3.10 to $3.30 per share against a P/E-multiple of 13 (13×$3.30 = $43) and the stock is already up +50% since December and, indeed, shows no signs of returning to its previous earth orbit in the $10 to $15 range.

However, the stock has never paid a dividend and is currently trading at $25 and well above the current Risk Price (SF) of $20. Investors can only make money on the stock by selling it to each other at a higher price, which, when we think about it, seems like a very odd ritual, like climbing a ladder with no steps, or a “rope trick”.

Some of the usual suspects, Vanguard, Wells Fargo, and T.Rowe-Price, are holding large positions in the stock in $400 million range, but there are also several comparable and still larger foreign interests of the LLC- and LLP-type that might also help to explain some of the price drive, and our possible future exposure to profit-taking should there be any “flats” or “potholes” on the road ahead, so to speak.

Because we know “where we are” in these uncharted lands, should the big investors decide to bail to take profits, wag their tail to adjust their “beta”, or pay unearned dividends to their own shareholders, we’ve got the bucket already in place and intend to keep it there. Please see our Post, Earnings Don’t Matter, April 2013.

Exhibit 1: (B)(N) HTZ Hertz Global Holdings Incorporated – Risk Price Chart

(B)(N) HTZ Hertz Global Holdings Incorporated

Hertz Global Holdings Incorporated is a general use car rental brand and is engaged in equipment rental businesses in the United States and Canada. The Company and its licensees and associates accept reservations for car rentals & equipment.

(Please Click on the Chart to make it larger if required.)

From the Company: Hertz is the largest worldwide airport general use car rental brand, operating from approximately 8,800 corporate and licensee locations in approximately 150 countries in North America, Europe, Latin America, Asia, Australia, Africa, the Middle East and New Zealand. Hertz is the number one airport car rental brand in the U.S. and at 111 major airports in Europe. In addition, the Company has sales and marketing centers in 60 countries which promote Hertz business both within and outside such country. Product and service initiatives such as Hertz Gold Choice, Hertz #1 Club Gold®, NeverLost® customized, onboard navigation systems, Sirius XM Satellite Radio, and unique cars and SUVs offered through the Company’s Adrenaline, Prestige and Green Traveler Collections, set Hertz apart from the competition. In 2008, the Company entered the global car sharing market with its service now referred to as Hertz On Demand which rents cars by the hour and/or by the day, at various locations in the U.S., Canada and Europe. Hertz also operates one of the world’s largest equipment rental businesses, Hertz Equipment Rental Corporation, offering a diverse line of rental equipment, from small tools and supplies to earthmoving equipment, as well as new and used equipment for sale, to customers ranging from major industrial companies to local contractors and consumers, from approximately 340 branches in the United States, Canada, China, France, Spain and Saudi Arabia, as well as through its international licensees. Hertz also owns Donlen Corporation, based in Northbrook, Illinois, which is a leader in providing fleet leasing and management services.

Through its Dollar Rent A Car and Thrifty Car Rental brands, the Dollar Thrifty Automotive Group has been serving value-conscious leisure and business travelers since 1950. The Company maintains a strong presence in domestic leisure travel in virtually all of the top U.S. and Canadian airport markets, and also derives a significant portion of its revenue from international travelers to the U.S. under contracts with various international tour operators. Dollar and Thrifty have approximately 280 corporate locations in the United States and Canada, with approximately 5,800 employees located mainly in North America. In addition to its corporate operations, the Company maintains global service capabilities through an expansive franchise network of approximately 1,300 franchise locations in 82 countries. In November 2012, Hertz Global Holdings, Inc. acquired Dollar Thrifty Automotive Group, Incorporated which is now a wholly-owned subsidiary of Hertz.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.