(B)(N) DELL Dell Incorporated

Deal Book. Dell Incorporated is still selling business and personal computers and every flavor of desktop, laptop, notebook and ultra-book, and last year, they sold $60 billion worth, just as they did in every year for the last five years – neither much more nor much less; and it gets an 8% operating margin and bottom-line profits of about half of that at $2 billion per year.

But nobody wants this business except the founder, Mr. Michael Dell, who has a new vision. Else, it’s become so boring, and well-run, that it’s just a job, and all the top brass need to be paid several million dollars a year to show up every Monday and not stay home to bake cookies.

The name-brand, Mr. Michael Dell, wants to buy it back (please see our Post, (B)(N) DELL Dell Incorporated, February 2013) and re-orient the company from manufacturing and warehouse direct-to-customer sales, to an “integrated service company”, something like what the IBM Corporation did in the 90’s when it had a similar problem of commodity saturation and an uncertain future in the business that it created, and was trading at $20 and way below the current $200 and dividends of $4 billion a year to its shareholders, on sales of about $100 billion, just 50% more than the faltering and dormant Dell.

Enter Mr. Dell, Silver Lake Partners, the Blackstone Group LLP, and the activist investor, Mr. Carl Icahn, and others such as Southeastern Asset Management Incorporated and T.Rowe Price, that we know of, and even some shadowy figures such as the ex-portfolio manager at the Diamondback Capital Management company who is now serving 4 1/2 years in prison for front-running the deal (Reuters, May 2, 2012, Ex-fund manager sentenced to prison for insider trading).

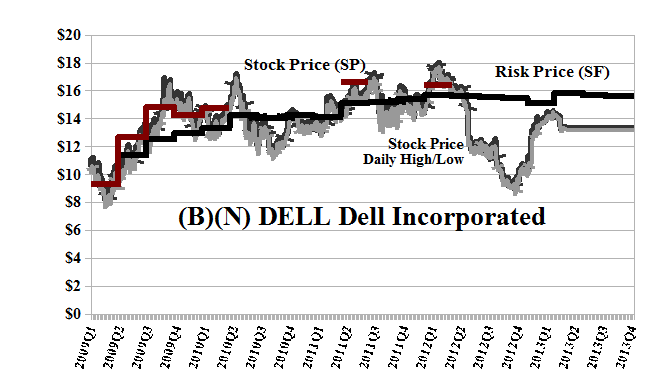

Did these guys buy at the stock at $20 to $25 in 2008, or more recently at $9 to $10 late last year? Hopefully, not the former, $20 to $25 in 2008, because the stock is now “worth” $15 per share or $27 billion that is “as good as cash” and “better than money” and any cash, or cash and stock deal, can be measured against that benchmark – anything else is just robbery or largesse. Please see Exhibit 1 below, and the Risk Price (SF) which is $15 and our best estimate of the “price of risk” while the stock is trading at $13 to $14 on volumes of between 10 million and 100 million shares per day, depending on the latest fit of undue “concern” for maximizing alleged shareholder value that is no more than $15 per share.

The “price of risk” is provably the “least stock price” at which the stock – which is just a piece of paper – is “as good as cash” and “better than money” because that is our best estimate of the exact price at which the investor can hope for a non-negative real rate of return, that is, a rate of return that is positive and exceeds the rate of inflation which “cash” can’t do. Please see our Post, Bystanders & Collateral Damage, April 2013, for more information. If an investor wants more than that, then, perhaps they should sell their stock and buy gold (sic)? Please see our Posts, The Silly Season For Investment Advisers, April 2013, or Extraterrestrial Funds (ETFs), March 2013, for more on that.

However, Mr. Dell does not have $27 billion in cash to pay to the shareholders for all of their stock, but is said to personally own about 16% of the stock whereas the Icahn group apparently owns about 13% of the stock and is agitating for some price between $12 and $15, or whatever they can get at the end of the day, regardless of what might happen to the company, thereafter, when all the “financial engineering” is done and found to be wanting.

The Blackstone Group LLP was apparently offering $14.25 per share for all of the company, but has since dropped out, citing reservations about acquiring the “cookie cutter”-like business in a market of “bakers” and chip-makers that they don’t understand, so to speak; and the Icahn group has offered $15 per share for 58% of the company (USA Today, April 19, 2013, Blackstone drops out of race to buy Dell) but has axed that offer, too, and come up with yet another offer – in a letter to the Board – that we don’t understand (Reuters, May 10, 2013, Icahn, Southeastern offer alternative to Dell buyout). It’s likely that others are in the same boat and Mr. Icahn is applying the cudgels to our ignorance – “It’s insulting to shareholders’ intelligence for the board to tell them that this board only has the best interests of shareholders at heart. We are often cynical about corporate boards but this Board has brought that cynicism to new heights.”

We don’t own any of the stock in the Perpetual Bond™ because it’s trading below the Risk Price (SF) and it also has an estimated quarterly downside volatility in the stock price of minus ($3) so that it could be trading anywhere between the current $13 and $10 or $16 with no surprise.

What is best for the shareholders, in our view, is that Mr. Dell & Company, just keep doing what they’re doing and implement the changes that they want to make as they can, and forget about the billet doux “letters to the Board”, or just share them with the Press so that no one else should have to go to jail at the tax payers’ expense.

Exhibit 1: (B)(N) DELL Dell Incorporated – Risk Price Chart

(B)(N) DELL Dell Incorporated – May 2013

Dell Incorporated is a information technology company, which offers a range of technology solutions, including servers and networking products, storage products, services, software and peripherals, mobility products, and desktop PCs.

(Please Click on the Chart to make it larger if required.)

From the Company: Dell Incorporated is an information technology company, and provides a range of technology solutions worldwide. The company offers client computing devices, including desktop personal computers, notebooks, and tablets; rack, blade, tower, and hyper-scale servers for enterprise customers, and value tower servers for small organizations, networks, and remote offices; networking solutions; and storage solutions, including storage area networks, network-attached storage, direct-attached storage, and backup systems. It also sells peripherals, including monitors, printers, projectors, and other client and enterprise peripherals, as well as third-party software products. In addition, the company offers support and extended warranty services, enterprise installation services, and configuration services; and infrastructure and security managed services, cloud computing and infrastructure consulting services, and security consulting and threat intelligence services. Further, it provides applications services, such as application development and maintenance, application migration and management, package implementation, testing and quality assurance functions, business intelligence and data warehouse solutions, and application consulting services; business process services comprising back office administration, call center management, and other technical and administration services; and system management, security software, and information management services. Additionally, the company offers financial services, including originating, collecting, and servicing customer receivables primarily related to the purchase of its products. It serves corporate businesses; educational institutions, government, health care, and law enforcement agencies; small and medium-sized businesses; and consumers directly, as well as through retailers, third-party solution providers, system integrators, and third-party resellers. Dell Incorporated was founded in 1984, and now has about 110,000 employees and is still headquartered in Round Rock, Texas.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.