(B)(N) ANF Abercrombie & Fitch Company

Drama. John Maynard Keynes (1883-1946), was an economist and, despite all of that knowledge, a pretty good investor too; he coined the term “animal spirits” and observed that “all sorts of considerations enter into market valuation which are in no way relevant to the prospective yield” – J. Maynard Keynes, The General Theory of Employment, Interest and Money, New York, 1936.

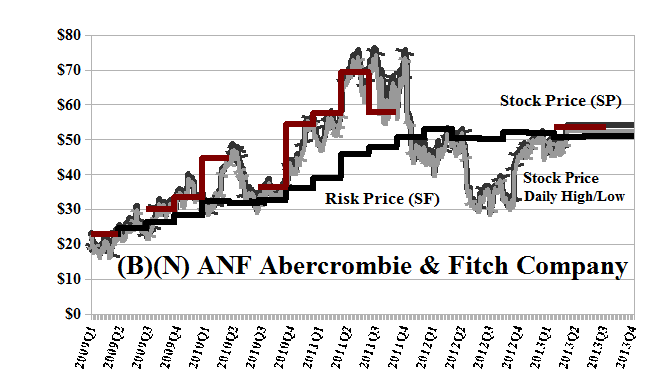

Oblivious to that observation, the tony fashion retailer, Abercrombie & Fitch Company, has twice failed to respect the difference between those who buy their clothes, and have no hips or waistline by preference and design, and those who buy their stocks, and have ample hips and waistlines by necessity regardless (Business Insider, May 3, 2013, Abercrombie & Fitch Refuses To Make Clothes For Large Women); and, so, has twice driven their stock price in apparently irrational fits of despondency from $70 in 2008 to $20 a year later to $70 in 2011 to $30 a year later and to $54 today (please see Exhibit 1 below). What will they say next (Insight, May 9, 2013, Abercrombie & Fitch CEO Mike Jeffries’s big fat mistake)?

We’ve had ample opportunity to own the stock in the Perpetual Bond™ between $30 in 2009 and $70 two years later – respecting our “selling discipline”, else we would have suffered the same fate as many others who were buying or holding it at $60 t0 $70 in 2011 or even $50 early last year – and it’s lunged its way back into the Perpetual Bond™ at the current $54 (please see Exhibit 1 below; Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason). The company has gross sales of $4.5 billion per year but manages only a paltry dividend of $0.20 per share per quarter, or $63 million to its shareholders for a thin yield of only 1.5%.

The indicated quarterly volatility in the stock price is minus ($6.50) per share or ±12% so that any price between the current $54 and $48 to $60 should not surprise us. If we give them another chance at $54, then we’re also going to buy the August “collar” at $52 for $3.50 per share and sell an offsetting short call at $58 for $3.00 so that for $54 for the stock and $0.50 for the collar ($3.50 less $3.00), we can ride out the summer sales at between $52 and $58, in case it’s a warm one and Mr. Jeffries is right after all. And please see our Post, Pension Envy, May 2013, for an update on the snugly fitting Lululemon Athletica’s “material” adventures.

Example 1: (B)(N) ANF Abercrombie & Fitch Company – Risk Price Chart

(B)(N) ANF Abercrombie & Fitch Company

Abercrombie & Fitch Company is a specialty retailer, which operates stores and direct-to-consumer operations. The Company sells products, including casual sportswear apparel, including knit and woven shirts, and graphic t-shirts.

(Please Click on the Chart to make it larger if required.)

From the Company: Abercrombie & Fitch Company, through its subsidiaries, operates as a specialty retailer of casual apparel for men, women, and kids. It operates through three segments: U.S. Stores, International Stores, and Direct-to-Consumer. The company sells various products, including casual sportswear apparel comprising knit and woven shirts, graphic T-shirts, fleece, jeans and woven pants, shorts, sweaters, and outerwear; personal care products; and accessories for men, women, and kids under the Abercrombie & Fitch, abercrombie kids, and Hollister brand names. It also offers bras, underwear, personal care products, sleepwear, and at-home products for girls under the Gilly Hicks brand. As of February 2, 2013, the company operated 912 stores in the United States and 139 stores internationally. Abercrombie & Fitch Co. sells its products through its stores and direct-to-consumer sales. The company was founded in 1892 and is headquartered in New Albany, Ohio.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.