(B)(N) TS-B Torstar Corporation Class B Non-voting

Deal Book. The Toronto Star is an institution and has been publishing its newspaper, and doing good things in the community, for over 120 years since 1892. But as a stock, its fallen on hard times, and as a business, its had to make some hard decisions (Reuters, May 8, 2013, Torstar profit plummets; Co cuts 105 jobs) and had some odd exposures in the arena of publishing and intellectual property rights (CNW, April 2, 2013, Class Action Complaint Against Harlequin Enterprises Dismissed).

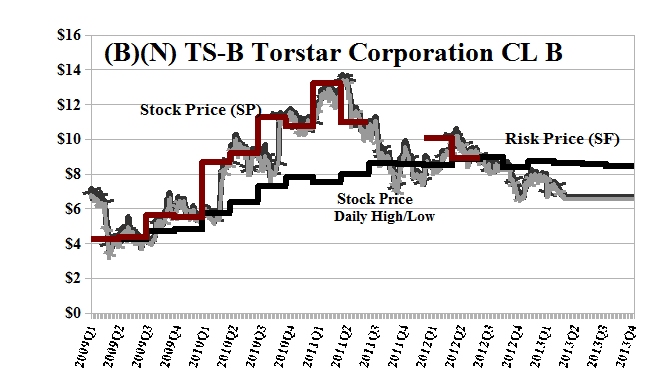

The company has a current market value of about $430 million based on the non-voting Class B stock of which there are 70 million shares currently priced at $6.20 and below the Risk Price (SF) of $8.50 (please see Exhibit 1 below). The indicated dividend is expected to be $0.131 per share per quarter for a payout of $42 million this year, including the more exclusive Class A voting stock of about 10 million shares, for an extraordinary yield of 8.5% or more if the stock price doesn’t get any better. Moreover, at the option of the Company or the shareholder (please see the Annual Report 2012, Torstar Corporation, Note 17), the dividend can be paid in shares of the Class B stock issued to both the Class A and Class B shareholders, which would mean a roughly 10% dilution, or 7 million new shares of the Class B stock, at the current stock price.

However, 7 million new shares with a market value of $42 million is not the same as $42 million in cash because the shares are trading at a discount to the Risk Price (SF) of $8.50 which is “cash” and “better than cash” because it is the stock price at which the company becomes an “investment” – that is, it’s the purchase (or gift or acquisition) of risk that is likely to obtain a non-negative real return (please see our previous Post, (B)(N) DVA DaVita HealthCare Partners Incorporated, May 2013, for a more detailed explanation and another example).

In other words, in order that 7 million new shares should be as good as cash and an “investment” (which is what stock is supposed to be), the company would have to issue more of them (in fact, $8.50/$6.20 is 40% more of them) in order to make up the “gap” between $8.50 per share, which is “cash” and “better than cash”, and $6.20 per share which is not cash but a stock with the “risk attached” and a price, $6.20 per share, that it might never see again. That’s a pretty sharp pencil, isn’t it.

An 8.5% yield is in fact an 8.5% yield if paid in cash, but if paid in stock, then only if the stock price is at the “price of risk” which we can reliably calculate as the Risk Price (SF) and it puts a burden (or opportunity) on the company owners, the voting stock, to do what it takes to encourage those values – a stock price at or above the price of risk, and, of course, it works the other way if that is the case.

Exhibit 1: (B)(N) TS-B Torstar Corporation Class B Non-voting – Risk Price Chart

(B)(N) TS-B Torstar Corporation CL B NV

Torstar Corporation is engaged in the publishing of newspapers, books and websites. It publishes daily and community newspapers, speciality publications, digital properties, Syndicate content, as well as women’s fiction.

(Please Click on the Chart to make it larger if required.)

From the Company: Torstar Corporation engages in the media and book publishing businesses in North America and internationally. The company operates in two segments, Media and Book Publishing. The Media Segment publishes four daily newspapers: the Toronto Star, The Hamilton Spectator, the Waterloo Region Record, and the Guelph Mercury, as well as approximately 100 community newspapers in Ontario. It also publishes the English-language metro newspapers in various Canadian cities; and the Chinese-language Sing Tao daily and its related publications in Toronto, Vancouver, and Calgary. In addition, this segment offers editorial content to newspapers and other media; and printing, outdoor advertising, Chinese language telephone directories, radio, and weekly magazine publishing. Further, it operates thestar.com, a newspaper Website; Wheels.ca and toronto.com for events and attractions; Olive Media for online advertising; eyeReturn Marketing that provides online marketing services; wagjag.com and Tuango.ca daily deal Websites; Jaunt.ca, a travel deal Website; travelalerts.ca, a publisher of travel promotional emails; targetvacations.ca, an online travel agency; Workopolis, which provides Internet recruitment and job search solutions; goldbook.ca; and flyerland.ca, HomeFinder.ca, gottarent.com, save.ca., and LeaseBusters.com. Additionally, this segment operates Torstar Media Group television, a teleshopping channel, and a product sourcing and distribution business. The Book Publishing segment publishes and distributes books in various genres and formats, including digital. It offers books under various imprints, including Harlequin, Harlequin MIRA, Harlequin HQN, Harlequin LUNA, Harlequin Nonfiction, Harlequin TEEN, Harlequin Kimani Press, and Carina Press. This segment sells books through the retail channel, in stores, and online, as well as directly to the consumer through direct mail and its Internet sites. Torstar Corporation was founded in 1892 and is based in Toronto, Canada.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.