(B)(N) DVA DaVita HealthCare Partners Incorporated

Deal Book. Berkshire Hathaway owns about 15 million shares of DaVita HealthCare Partners and that is an approximately 14.2% interest in the 105,759,863 shares outstanding (106 million in round numbers) but Berkshire has also entered into a “standstill” agreement with the company that would allow it to increase its stake to 25% or 26.5 million shares without triggering takeover defenses (Reuters, May 7, 2013, Berkshire may boost DaVita stake to 25 percent).

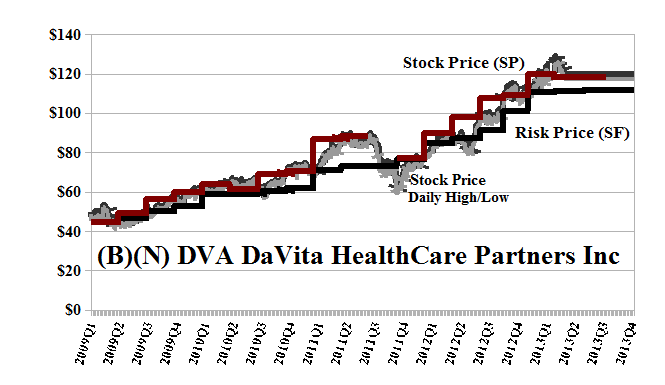

The company is currently in the Perpetual Bond™ at $120 and we last bought it at $80 in 2011 (please see Exhibit 1 below); however, the stock was trading at $125 two weeks ago (in mid-April) but had dropped down to $118 prior to the announcement, and it is now trading up $2 at $120, and who knows what the future price will be. But we’re sharpening our pencils, and we advocate that the company, DaVita and its shareholders, of which there are over 400 institutions and mutual funds that hold 97% of the stock, consider offering to sell 10 million shares out of treasury at the current Risk Price (SF) of $118 in order to complete this deal.

Moreover, that is the “best deal” that can be done for the benefit of the shareholders, which includes Berkshire Hathaway, and the company, and the standard for “best” is “the demonstrated societal standard of risk aversion and bargaining practice” (please see our Post, The Price of Risk, August 2012).

Pragmatically, the deal increases the net worth of the company by $1.18 billion in cash, from the current $3.8 billion to $5 billion (in round numbers), which can be used to support the growth and services of the company; or to retire debt (currently at $12 billion); or to pay a special dividend of $10 per share to all the shareholders, and, in fact, return $250 million to Berkshire Hathaway (which is probably not their intention, because it makes the stock look “cheap” and it would likely drop $10 per share thereafter; the company currently does not pay any dividends).

The alternative is that Berkshire just accumulate shares in the open market as they go up for sale at whatever blocks or ambient stock prices it can obtain; this benefits only those shareholders who are selling their stock, and there is no “timeline” to effect the sales and purchases – they could occur at any price between a higher price or a lower price depending on the future, which is unknown.

Of course, it’s none of our business how they do this deal – who are we to say how companies or investors should spend their money? Or why should anyone plan for the future, rather than just do what feels good, or “deals” good? However, another way to put it is that (as we said) it is the best deal within “the demonstrated societal standard of risk aversion and bargaining practice” and, therefore, supports the “good” of the capital markets rather than the “bad” which might be described as “buccaneering” or “gambling” (please see our Post, Bystanders & Collateral Damage, April 2013).

And to put it yet another way, the reason that it’s the “best deal” is that the Risk Price (SF) is the “least stock price” at which the stock is as “as good as cash” and “better than cash” because it holds out the hopeful opportunity to receive a return that exceeds the rate of inflation, which is what an investment is – an investment is the purchase of risk in order to receive a hopefully non-negative real (that is, net of inflation) rate of return, a property that money as cash just doesn’t have.

Exhibit 1: (B)(N) DVA DaVita HealthCare Partners Incorporated – Risk Price Chart

(B)(N) DVA DaVita HealthCare Partners Inc

DaVita HealthCare Partners Inc operates kidney dialysis centers and provides related lab services mainly in dialysis centers and in contracted hospitals across the United States. It also operates other ancillary services and strategic initiatives.

(Please Click on the Chart to make it larger if required.)

From the Company: DaVita is the dialysis division of DaVita HealthCare Partners Inc., a Fortune 500® company that, through its operating divisions, provides a variety of health care services to patient populations throughout the United States and abroad. A leading provider of kidney care in the United States, DaVita delivers dialysis services to patients with chronic kidney failure and end stage renal disease. DaVita strives to improve patients’ quality of life by innovating clinical care, and by offering integrated treatment plans, personalized care teams and convenient health-management services. As of December 31, 2012, DaVita operated or provided administrative services at 1,954 outpatient dialysis centers located in the United States serving approximately 153,000 patients. The company also operated 36 outpatient dialysis centers located in eight countries outside the United States. DaVita supports numerous programs dedicated to creating positive, sustainable change in communities around the world. The company’s leadership development initiatives and social responsibility efforts have been recognized by Fortune, Modern Healthcare, Newsweek and WorldBlu.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.