(B)(N) SPRD Spreadtrum Communications Incorporated

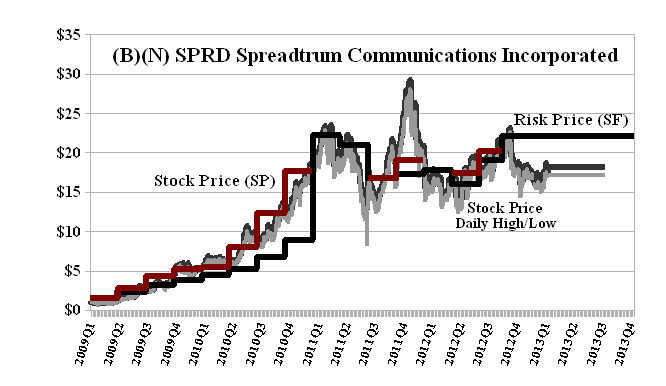

Drama. Spreadtrum Communications Incorporated is a relatively small NASDAQ™ 100 company with a market capitalization of about $1 billion. It pays a dividend of $0.095 per quarter or $18 million a year to its shareholders for a current yield of 2.1% and has an operating margin of more than 40% on sales of about $900 million per year which are up five-fold since 2009. It’s an astonishing story in complicated and innovative technology, sales, marketing and manufacturing efficiency (The StreetAuthority Network, March 12, 2013, Little-Known Stock Could Deliver 28% Returns at Apple’s Expense) but, despite all of that, we can’t buy it as an investment for the Perpetual Bond™ because, and only because, the ambient stock prices of about $18 are below the Risk Price (SF) of $23 and no amount of “future gazing” (or bar charts, ibid The StreetAuthority) and optimism can help us to overcome that fact and, in our view, buying the stock at $18 now is just a gamble. Nor could we buy it at prices of about $15 a few months ago but we could think about buying it at prices above $23 now or above $20 in mid-year 2012, nearly a year ago. Please see Exhibit 1 below.

On the plus side, and to our benefit, we did own the stock between $2 and $18 for two years between early 2009 and early 2011 (Red Line Stock Price (SP) above the Black Line Risk Price (SF)) when we were “called out” on a short call of $20 against our long position AND we did NOT own it again between $23 and $12 in the next year (no harm there, please see Exhibit 1 below) but we did own it again at higher prices of $18 in late 2011 when we were effectively “stopped out” at $16 (but saved by our long “protective” put at $18) and again in 2012 between $16 and $18 when we were “called out” at $23.

It seems complicated but every step is “mandated” and obvious if we understand the meaning of the Risk Price (SF) (which we will explain below) and “guessing”, or hoping, is not required. For example, if we were to think about buying it now at $18, we need to consider that the downside risk due to the demonstrated volatility of the stock price is minus ($2.50) (please see our Post, Popoviciu’s Volatility, September 2012) and the August 2013 put at $18 costs $2.75 today and the cost can only be somewhat offset by a sold or short call at $19 (which is all that’s available unless we can convince our broker to write one at a higher price such as $23) against our long position at $1.65 per share so that protecting our price at between $18 and $19 for the next five months will cost $1.10 per share today ($2.75 less $1.65) and raise the cost of our purchase to $19.10 (plus transactions costs). Obviously, there’s no upside for us unless other investors are willing to buy the stock at $19 or more in the future (and we buy an additional offsetting call at $19 to cancel or roll over our short call at that price). For a more inspiring purchase relying on the same ideas, please see our Post on (B)(N) TRP TransCanada Corporation, March 2013.

Exhibit 1: (B)(N) SPRD Spreadtrum Communications Incorporated – Risk Price Chart

Spreadtrum Communications Incorporated is a “fabless” (manufacturing is outsourced to specialist firms) semiconductor company that designs, develops and markets baseband processor solutions for the wireless communications market.

(Please Click on the Chart to make it larger if required.)

Spreadtrum’s head office is in Shanghai, China, and it is a leading supplier to Samsung, Huawei Technology Company and other manufacturers that stand to gain if iPhone growth slows (ibid, The StreetAuthority Network).

The Price of Risk

The Risk Price (SF) is our best estimate (and provably so) of the “price of risk” which is the stock price at which a Nash Equilibrium is established between “risk averse” and “risk seeking” investors. A company is a (B), and can, therefore, be included in the Perpetual Bond™, if and only if the ambient stock prices appear to be above the “price of risk” and an (N) otherwise. Stock prices above the “price of risk” (B) indicate that “risk averse” investors – we want to keep our money – 100% Capital Safety – and obtain a hopeful but not necessarily guaranteed rate of return above the rate of inflation – are willing to buy and hold the stock of the company at those prices, whereas stock prices below the “price of risk” (N) indicate uncertainty and stock price volatility that is caused by “risk seeking” investors who, for whatever reason, are hoping to anticipate the future. Please see our Posts, The Price of Risk, August 2012, and The Nash Equilibrium & Its Stock Price, October 2012, for more information.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.