Wallywood & The Baypatch

Drama. On an average day the “investment industry” is just another form of theatre and entertainment akin to “Wallywood” on Wall Street or the “Baypatch” at Bay & King and we watch them with the intensity and fascination of a soap opera – the deals, mama, the deals and the characters and persona, and the wealth, mother, the wealth – just think of it. Undoubtedly, the industry is too precious (or precious) and, with some exceptions, too big to fail (for which we are grateful) but the employment relationship has changed and we, as investors, don’t work for them any more (Reuters, January 10, 2013, Exclusive: Private equity eyed Legg Mason but were spurned – sources and CNBC, January 9, 2013, Deep Cuts Raise Questions About Morgan Stanley).

But, oddly enough, the firms Legg Mason Incorporated and Morgan Stanley and many others believe that their future is in “wealth management” – our wealth, actually – and that the future will be like the past and will eventually “mean revert” to their former grandeur although there is no reason for them to think that unless they also think that we, as investors, haven’t learned anything in the past twenty years and just want our old “job” back as bulk suppliers of fresh capital without much concern for our own future when the show is over, so to speak.

Legg Mason Incorporated is the fourth largest publicly traded asset manager in the USA with assets under management (which are basically unsecured liabilities owed to its customers and which can legally vanish due to investment risk) of about $648 billion and is fairly priced for acquisition at the current Risk Price (SF) of $28 (please see Exhibit 1 below). The current stock price, however, is $26 and way below the halcyon prices of $60 to $70 in 2008. The company pays a current stock dividend of $0.44 per share or $58 million per year to its shareholders for a current yield of 1.6% which is comparable to inflation and better than most of the bond yields that they’re selling to us. The stock is trading below the Risk Price (SF) and if we were to buy it as a speculation, we’d also have to pay to “collar” the price. For example, the May 2013 puts at $26 are available for $1.65 per share today and the sold or short call at $29 can be had for $0.85 per share so that for a net cost of $0.80 per share ($1.65 less $0.85) we can collect our dividends and lock in our price between $26 and $29 for the next five months while we wait for more information and some “news” or new drama that might suddenly affect the stock price up or down in the next episode.

Exhibit 1: (B)(N) LM Legg Mason Incorporated – Risk Price Chart

Legg Mason is a global asset management company that provides investment management and related services to institutional and individual clients, company-sponsored mutual funds and other pooled investment vehicles through its subsidiaries.

(Please Click on the Chart to make it larger if required.)

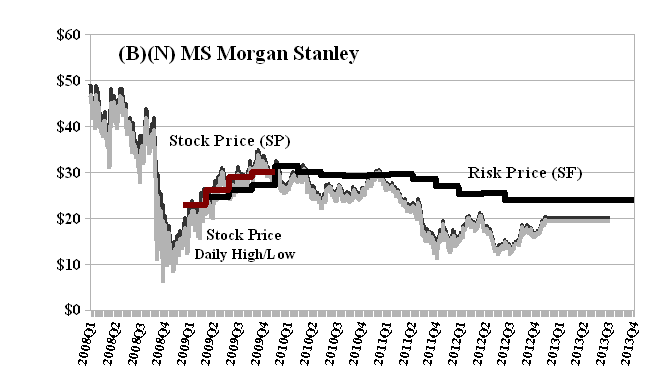

Morgan Stanley is also a publicly traded company with about $330 billion in assets under management (AUM) and net worth or shareholders equity of $62 billion or 20% of the AUM in contrast to Legg Mason which has a net worth of about $5.5 billion or less than 1% of the AUM. However, the business models are substantially different because Morgan Stanley is not just a wealth or asset manager but also an investment and merchant bank that takes an active interest in share flotation (normal course and IPOs) and mergers and acquisitions and restructuring. The company pays a current dividend of $0.20 per share or $395 million per year for a current yield of about 1%. The current Risk Price (SF) is $24 and the ambient stock prices are $20 with an indicated volatility of $2 per share (please see Exhibit 2 below).

Exhibit 2: (B)(N) MS Morgan Stanley – Risk Price Chart

Morgan Stanley is a financial services company, which through its subsidiaries and affiliates, provides products and services to a group of clients and customers, including corporations, governments, financial institutions and individuals.

(Please Click on the Chart to make it larger if required.)

It’s noteworthy that the wealth or asset management business is not only entertaining but a lot like “multi-level marketing” (please see our recent Post, (B)(N) HLF Herbalife Limited, January 2013, and the controversy among competing hedge fund managers about what they actually do for a living) and the host companies themselves (of which there are thousands) are at the top of the food chain because they provide the gloss and the promise or “product” of wealth and more wealth, execution and services that activate their sales forces and portfolio managers who long for “star quality”.

Unfortunately, it is not easy to make money in the stock market in any year, let alone year after year, and most portfolio managers will fail in that hopeful but not guaranteed promise of wealth and more wealth for us no matter how powerful they are as salespersons and last year nearly 90% of the established hedge fund managers – about 270 in 300 – failed to match the S&P 500 Index which gained +12% (CNBC, January 9, 2013, A horrid year for hedge funds) and underperformed all of the other major North American markets including the Dow Jones Industrials (+7%), the NASDAQ 100 (+17%) and the S&P TSX (+4%). One has to wonder that if they are not just gambling or “hunching” with our money (or bulk capital, so to speak) how that could happen to a “hedge fund” which is supposed to be tracking an index or balanced to defend our capital.

Exhibit 3: (B)(N) S&P 500 NYSE The RiskWerk Company Perpetual Bond™ – Cash Flow

(Please Click on the Chart and again to make it larger if required.)

In contrast, the Perpetual Bond™ (please see Exhibit 3 above) is an actively managed portfolio of stocks that returned +20% plus dividends of another 2% or 3% last year in the $11 trillion market of the S&P 500 NYSE which could absorb most private and public pension funds, endowment and trust funds in the first decimal point. Naturally, when we’re talking to our broker about their latest ideas and concerns we sometimes think or hum the famous words and music of Bob Dylan to entertain ourselves and remind us of why we are there:

Maggie’s Farm – Words and Music by Bob Dylan

I ain’t gonna work on Maggie’s farm no more.

No, I ain’t gonna work on Maggie’s farm no more.

Well, I wake up in the morning,

Fold my hands and pray for rain.

I got a head full of ideas that are drivin’ me insane.

It’s a shame the way she makes me scrub the floor.

I ain’t gonna work on Maggie’s farm no more.

I ain’t gonna work for Maggie’s brother no more.

No, I ain’t gonna work for Maggie’s brother no more.

Well, he hands you a nickel,

He hands you a dime,

He asks you with a grin

If you’re havin’ a good time,

Then he fines you every time you slam the door.

I ain’t gonna work for Maggie’s brother no more.

I ain’t gonna work for Maggie’s pa no more.

No, I ain’t gonna work for Maggie’s pa no more.

Well, he puts his cigar

Out in your face just for kicks.

His bedroom window

It is made out of bricks.

The National Guard stands around his door.

Ah, I ain’t gonna work for Maggie’s pa no more.

I ain’t gonna work for Maggie’s ma no more.

No, I ain’t gonna work for Maggie’s ma no more.

Well, she talks to all the servants

About man and God and law.

Everybody says

She’s the brains behind pa.

She’s sixty-eight, but she says she’s fifty-four.

I ain’t gonna work for Maggie’s ma no more.

I ain’t gonna work on Maggie’s farm no more.

No, I ain’t gonna work on Maggie’s farm no more.

Well, I try my best

To be just like I am,

But everybody wants you

To be just like them.

They say “sing while you slave,” and I just get bored.

I ain’t gonna work on Maggie’s farm no more.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.