(B)(N) LYG Lloyds Banking Group PLC ADS

Drama. The British Exchequer has the “problem” of selling the 40% of the common stock that it owns in the Lloyds Banking Group as a result of saving the company from itself during the so-called “banking crisis” in 2008 and 2009. The bank should not to be confused with the specialist insurance group Lloyd’s of London which was also founded in 17th century and has a similarly illustrious history but a better present.

Lloyds Banking Group PLC

Simply Simon Simple “Tells Sid” 1986

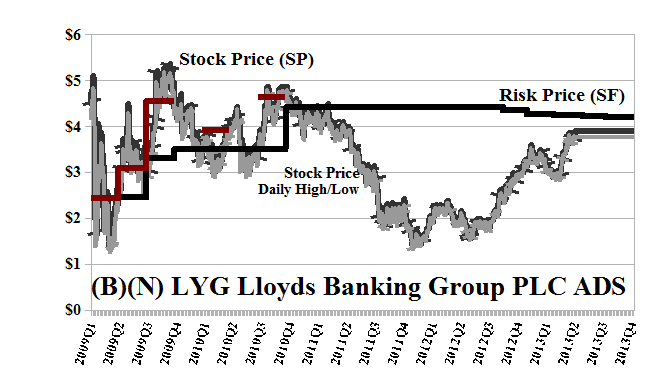

And it is quite a “problem” because the approximately 6.9 billion shares that it owns are worth about $27 billion at the current market price of $3.90 per share (please see Exhibit 1 below).

The alleged “think tank” Policy Exchange respected by the Finance Minister, Mr. Osborne, has suggested that the stock should simply be given away (rather than sold to the public as per the British Gas Corporation “implosion” known as “Tell Sid” in 1986) to the 40 to 45 million people who have national insurance numbers and (think some) it will be appreciated in the upcoming election year in 2015 and, of course, the Exchequer also owns 81% of the Royal Bank of Scotland (RBS) and will have a similar problem of unloading that interest of $70 billion in case the electorate needs to be simply reminded of the government charity during the election year.

We are, of course, riven with apoplexy and our preference is to simply toss the lot of them, politicians and think tank and all, on to the public dole simply because they are unemployable and have simply learned nothing in their entire life in the best schools of England.

The stock currently trades in New York as an ADS (American Depository Share), doesn’t pay a dividend, and isn’t worth anything unless someone is willing to buy it, and someone is because it trades an average of about 2 million shares a day.

There’s even an options market for it and the October put or call at $4 sells for about $0.45 and $0.35 per share, respectively. And that’s attractive. For $0.80 a share, today, we can only be wrong if the stock is still $4 in October but it’s still a gamble. The Lloyds bank has cut its losses to less than ($1 billion) last year, down from ($4 billion) in 2011, and anything can happen because, after all, it’s a bank and manages $1.5 trillion of its depositors’ money as well as a lot of their other wealth for which it is totally not responsible.

Our estimate of the demonstrated downside volatility in the stock price is only minus ($0.50) per share, but we are ready to be surprised in the current environment of government largesse and even more worthless money.

Exhibit 1: (B)(N) LYG Lloyds Banking Group PLC ADS – Risk Price Chart

(B)(N) LYG Lloyds Banking Group PLC ADS

Lloyds Banking Group PLC provides a wide range of banking and financial services. Its main business activities are retail, commercial and corporate banking, general insurance, and life, pensions and investment provision.

(Please Click on the Chart to make it larger if required.)

From the Company: Lloyds Banking Group plc provides banking and financial services to personal, commercial, and corporate customers in the United Kingdom and internationally. The company operates in four divisions: Retail; Commercial Banking; Wealth, Asset Finance, and International; and Insurance. The Retail division provides a range of retail financial service products, including current accounts, savings, personal loans, credit cards, and mortgages under the Lloyds TSB, Halifax, Bank of Scotland, and Cheltenham & Gloucester brands. It also distributes general insurance and bancassurance; and sells long-term savings, investment, and general insurance products. The Commercial Banking division provides banking and related services to business clients, from small and medium-sized enterprises to major corporate and financial institutions. The Wealth, Asset Finance, and International division offers private banking and asset management and asset finance; and operates international retail businesses. The Insurance division provides long-term savings, protection, and investment products through the bancassurance, intermediary, and direct channels of the Lloyds TSB, Halifax, Bank of Scotland, and Scottish Widows brands; and life, pensions, and investment products under the Heidelberger Leben and Clerical Medical brands. This division also offers general insurance to personal customers through the branch network, direct channels, and strategic corporate partners, as well as is involved in the brokerage of personal and commercial insurances. This division operates primarily under the Lloyds TSB, Halifax, and Bank of Scotland brands. The company was formerly known as Lloyds TSB Group plc and changed its name to Lloyds Banking Group plc in January 2009. Lloyds Banking Group plc was founded in 1985, has 93,000 employees, and is headquartered in London, the United Kingdom.

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks. Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™“

Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.Disclaimer Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.