(B)(N) BNS The Bank of Nova Scotia

Drama. “Wealth Management” appears to be a Really Big Deal for the banks, insurance companies, and financial planning firms of all sorts; we hear a lot about it and it seems to be their shortest path to great riches even though most of the “wealth” that they manage is said to have once belonged to their many, many, much poorer customers who are not getting any richer by all reports.

And the banks are usually willing to pay up to $1 for every $10 of new assets under management (AUM) that they might acquire by buying other “wealth management” firms. Please see The Canadian Press, May 28, 2013, Addition of ING Direct helps Scotiabank boost Q2 net income to $1.6 billion, and May 25, 2013, National Bank considering new acquisitions in Canadian wealth management, and our Post, New Found Money, April 2013.

Evaluating the Banks is also an art-form in the hands of the Basel Accords and the credit rating authorities; for example, Standard & Poor’s and Moody’s Investor Services raised some concerns last year for all the Canadian banks, citing the dangers of an increased “risk appetite” for higher yields, particularly in foreign lending (Reuters, December 14, 2012, Scotiabank questions S&P’s cut, citing international reach).

It’s confusing but we take note of it because the domestic mortgage lending experience in the U.S. just a decade ago, and well-regarded by the credit authorities at that time, certainly qualifies as a “foreign adventure” with consequences that are well-known and which we hope won’t be repeated at home. Please see our recent Post, Frontier Justice, May 2013, in which Paraguay has obtained better terms than the General Electric Company.

Fortunately, we don’t have to manage the banks. From our point of view, as investors, we have limited liabilities of no more than a zero stock price, and we’re only concerned about the stock price and the dividend yields, and we would be happy if the banks, as a business, simply managed their total assets for an investment return, that is, a non-negative real rate of return. But they fail grievously at that, and, therefore, really need the fees and loads that they charge on their “Wealth Management” of the depositors’ capital for which they are not responsible but can use to learn how to do this business.

For example, the Bank of Nova Scotia manages total assets of $740 billion, which is up +10% from $670 billion the year before, bolstered by acquisitions in the Wealth Management division, and their after tax income was $6.2 billion which is a less than a 1% return (93 basis points) on the total assets under management (AUM).

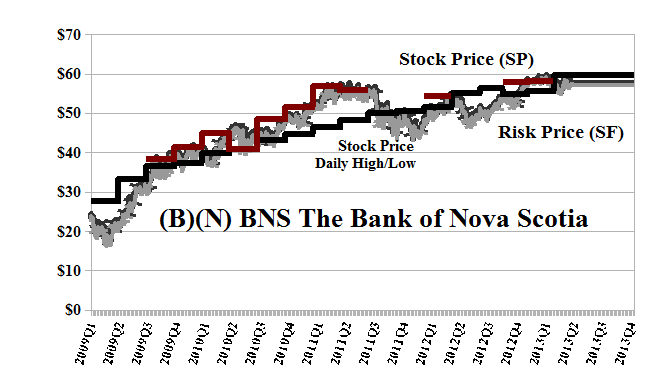

Our outlook as shareholders is much better; the bank has raised its dividend to $0.60 per share per quarter and expects to pay out $4 billion to its shareholders this year for an enormous current yield of 4% and the stock price is currently $60 and up from $57 since December for another +5% which we can expect to keep. Please see Exhibit 1 below.

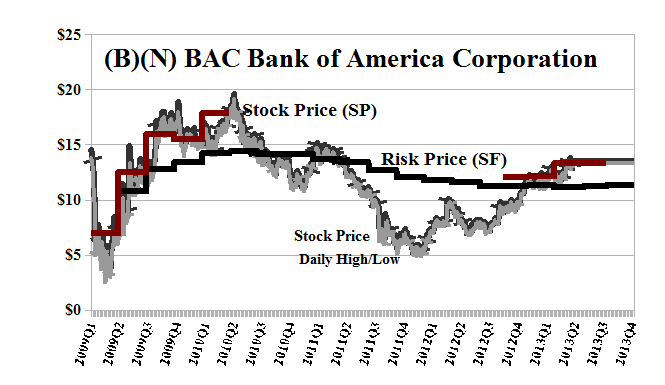

In contrast, the Bank of America has $2.2 trillion under management (its total assets) and earned $5 billion (including a tax credit of $700 million) for a return of 0.23% or 23 basis points; the expected dividend is $0.01 per share per quarter for a total payout of $433 million and a yield of 0.34% or 34 basis points. But the stock price is $13 and up from $11.50 in December for a gain of +12% or 1200 basis points. Please see Exhibit 2 below.

Both of the banks are eligible for inclusion in the Perpetual Bond™ (Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason) although the Bank of Nova Scotia at $59 is marginal with the current Risk Price (SF) of $60 and an estimated price volatility of minus (-$3) that might be expected in the next quarter.

Our downside estimate for the stock price of the Bank of America is minus (-$1.75) so that we would not be surprised by any price between the current $13 and $11 or $15 during the next several months. (For the details of that handy calculation, please see our Post, Popoviciu’s Volatility, September 2012.)

Exhibit 1: (B)(N) BNS Bank of Nova Scotia – Risk Price Chart

(B)(N) BNS Bank of Nova Scotia

Bank of Nova Scotia is a full-service financial institution, which operates its business in four major business lines: Canadian Banking, International Banking, Global Wealth Management and Scotia Capital.

(Please Click on the Chart to make it larger if required.)

Exhibit 2: (B)(N) BAC Bank of America – Risk Price Chart

(B)(N) BAC Bank of America Corporation – May 2013

Bank of America Corporation is a bank holding and a financial holding company, which through its subsidiaries, provides banking and non-banking financial services and products throughout the United States and in selected international markets.

(Please Click on the Chart to make it larger if required.)

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.