(B)(N) HRX Heroux-Devtek Incorporated

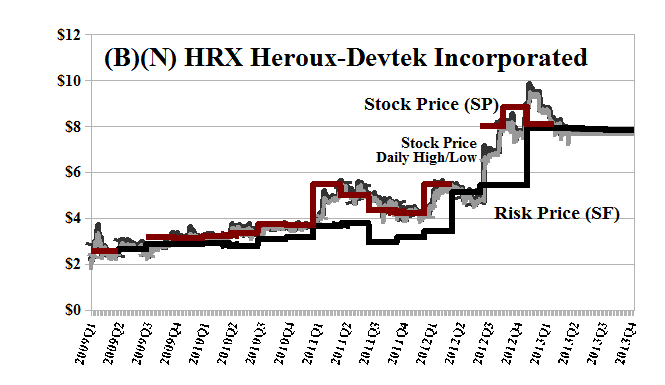

Deal Book. Heroux-Devtek is a relatively small company, situated in Longueuil, Quebec, Canada, on the beautiful south shore of the St. Lawrence River, and employs about 1,000 people, nearly 100 of whom specialize in the design and manufacture of aircraft landing gear, a specialization to which it returned after divesting its aero-structure and industrial products operations to Precision Castparts for $300 million late last year, which is more than its current market value of $245 million at $8 per share on just 32 million shares outstanding. Please see Exhibit 1 below.

Longueuil, Quebec, Canada. On the South Shore. “Labor et Concordia”

It doesn’t pay a regular stock dividend but distributed $5 per share to its shareholders in December for a payout of $160 million, or just half of the proceeds from the Precision Castparts deal.

About 15% of the stock is held by several mutual funds, and 50% of the stock is held by five institutional investors, Deans Knight Capital Management Limited (15%), Caisse De Depot Et Placement Du Quebec (14%), IG Investment Management Limited (12%), Natcan Investment Management Incorporated (10%), and Fiera Capital Corporation (4%), four of whom recently sold 600,000 shares between them, post-dividend, and undoubtedly contributed to the stock price volatility ( ![]() Morningstar, HRX Heroux-Devtek Incorporated).

Morningstar, HRX Heroux-Devtek Incorporated).

And in addition, the company has just been awarded a $50 million re-payable (one has to mention that when dealing with the government) loan through the Government of Canada’s Strategic Aerospace and Defence Initiative (SADI), which supports strategic industrial research and pre-competitive development projects in the aerospace, defence, space and security industries, to provide a direct line of support for Héroux-Devtek’s engineering efforts and research and development of new technologies for complete new landing gear systems. But why would it need a loan that increases its debt by 30% when if it just gave away three times as much? And a company like this should surely get a grant.

In our view, everybody here is doing their job except the Board of Directors – the company is selling and developing excellent products of extreme technical difficulty; the Government is promoting proven technology and its further development to benefit an entire region; and the shareholders are taking profits wherever they can.

And that’s the problem. The company needs to commit to a regular dividend, and keep its money, and manage its stock price, and that’s a Board issue (The Canadian Press, May 24, 2013, Restructured Heroux-Devtek shows reduced Q4 profit, revenue from core operations).

We’ve also owned the stock at various times (please see Exhibit 1 below; Red Line Stock Price (SP) above the Black Line Risk Price (SF), and for no other reason), but there’s no reason to hold it now absent the demonstration of some real commitment of the Board of Directors to manage the company as something other than a “dessert”.

Exhibit 1: (B)(N) HRX Heroux-Devtek Incorporated – Risk Price Chart

(B)(N) HRX Heroux-Devtek Incorporated

Héroux-Devtek Incorporated is a Canadian company specializing in the design, development, manufacture and repair and overhaul of landing gear systems and components for the Aerospace market.

(Please Click on the Chart to make it larger if required.)

The Corporation is the third largest landing gear company in the world, supplying both the commercial and military sectors of the Aerospace market with new landing gear systems and components, as well as aftermarket products and services. Approximately 70% of the Corporation’s sales are outside Canada, mainly in the United States. The company has been in business since 1942 and its head office is located in Longueuil, Québec with facilities in the Greater Montreal area (Longueuil, Laval and St-Hubert) and Kitchener and Toronto, Ontario; as well as Springfield and Cleveland, Ohio. Héroux-Devtek sells its products primarily to original equipment manufacturers, the US Air Force and the US Navy.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.