(B)(N) MNST Monster Beverage Corporation

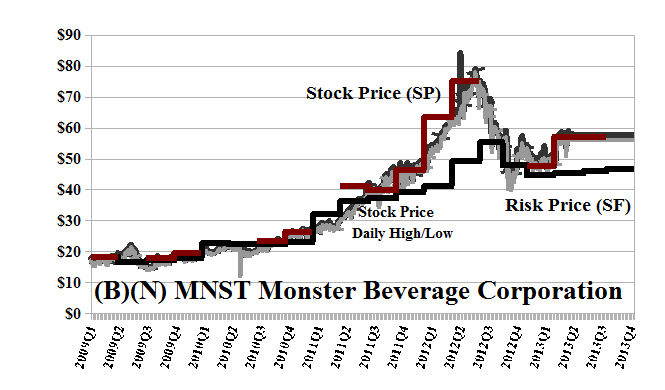

Drama. We took a ride on the Monster Beverage Corporation for one reason, and one reason only – its stock price was trading above the price of risk and we rode it from $40 in 2011 to $80 last year, in June 2012; and then we went for a coffee break, saved by our stop/loss at $70 (please see Exhibit 1 below).

Despite the fact that 75% of the shares and $7 billion of the market value (down from $9 billion in June of last year) is owned by institutions and mutual funds, we don’t know anything about this popular, tony, health-food, and energy-food market leader; neither does our accountant who sees a company with $1 billion in assets and negligible debt of $400 million, most of it in the inventory of $200 million; and sales of about $2 billion per year (which is about 4% of the Coca-Cola Company’s $50 billion) and a gross operating margin of 50% (MNST, May 17, 2013, Lack Of Cost Control And Demand Risk: The Story Of Monster Beverage Energy Drinks).

It’s eligible for the Perpetual Bond™ again at the current $56 above the Risk Price (SF) of $45 and rising (please see Exhibit 1 below) but it’s never paid a dividend and the stock price downside risk due to volatility is still minus ($10) per share so that we could be sold out at $46 or less unless the stock price steams up again.

It’s a big decision but we bought the June put at $55 for $1.65 and plunged for the short call at $63 for $0.65 so that for a net cost of holding the stock at $56 and the collar at $1.00 ($1.65 less $0.65), we can ride out the current health storms and further studies, and some issues of “if it’s that good, it must not be good for you” for between $55 and $63 for the next month (Reuters, March 22, 2013, Energy Drinks Linked to Adverse Health Effects).

Undoubtedly, some good news will rocket the stock, but the bad news, if any, will be just another lesson in stock market investing in things that we don’t know anything about; but we are willing to defer to our peers, who know everything and are voting with their money (or your money in the pension funds and mutual funds that own it).

Exhibit 1: (B)(N) MNST Monster Beverage Corporation – Risk Price Chart

(B)(N) MNST Monster Beverage Corporation

Monster Beverage Corporation through its subsidiaries, develops, markets, sells, and distributes beverages in the United States and internationally.

(Please Click on the Chart to make it larger if required.)

From the Company: Monster Beverage Corporation, through its subsidiaries, develops, markets, sells, and distributes alternative beverage category beverages in the United States and internationally. The companys Direct Store Delivery segment offers carbonated energy drinks, non-carbonated dairy based coffee plus energy drinks, carbonated energy drinks containing nitrous oxide, non-carbonated energy drinks with electrolytes, energy supplements, and ready-to-drink iced teas. This segment sells its products through a distributor network. Its Warehouse segment provides sodas, juice cocktails, energy drinks, fruit juice products and smoothies, aseptic juices, organic juices, fruit and coconut water juices, ready-to-drink lemonades, ready-to-drink lemonade plus tea drinks, powder drink mixes, vitamin enhanced flavored water, ready-to-drink aguas frescas, prebiotic and probiotic digestive wellness ready-to-drink beverages and powder drink mixes, and coconut waters. This segment markets its products primarily directly to retailers. The company distributes its products principally under the Monster Energy, Monster Rehab, Monster Energy Extra Strength Nitrous Technology, Java Monster, X-Presso Monster, Worx Energy, Peace Tea, Hansens, Hansens Natural Soda, Junior Juice, Blue Sky, Huberts, and Vidration brands. It serves full service beverage distributors, retail grocery and specialty chains, wholesalers, club stores, drug chains, mass merchandisers, convenience chains, health food distributors, food service customers, and the military. The company was formerly known as Hansen Natural Corporation and changed its name to Monster Beverage Corporation in January 2012. Monster Beverage Corporation was founded in 1985 and is based in Corona, California.

The Price of Risk

The calculated Risk Price (SF) is a provably effective estimate of the “price of risk” which is “the least stock price at which the company is likeable” (Goetze 2009) and “likeability” is determined by the demonstrated factors of “risk aversion” – we want to keep our money and obtain a hopeful return above the rate of inflation – and the properties of portfolios of such stocks.

Stock prices that are less than the price of risk can be said to be “bargain prices” but with the risk attached that the company might never get a higher price other than that due to ambient volatility or “surprise”; on the other hand, investors who are willing to pay the “full price” above the price of risk, and buy and hold the stock at those prices, must also be confident, and have reason to believe, that the company will produce those values, absent new information.

Please see our Posts, The Price of Risk, August 2012 and The Nash Equilibrium & Its Stock Price, October 2012, for more information on the theory.

To see what else “risk averse” investing can do for us, please see our recent Posts, The Wall Street Put, April 2013, and earlier Posts such as The Dow Transports, March 2013, or The Risk Adjusted Dow, March 2013, or The Canada Pension Bond, February 2013, and for a more colorful description of investment risk and the application of the “price of risk” to mergers & acquisitions, please see our Post, Bystanders & Collateral Damage, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

に関する考え方| |あなたは リンク交換?

LikeLike

Thank you! Best regards, Ernst.

LikeLike