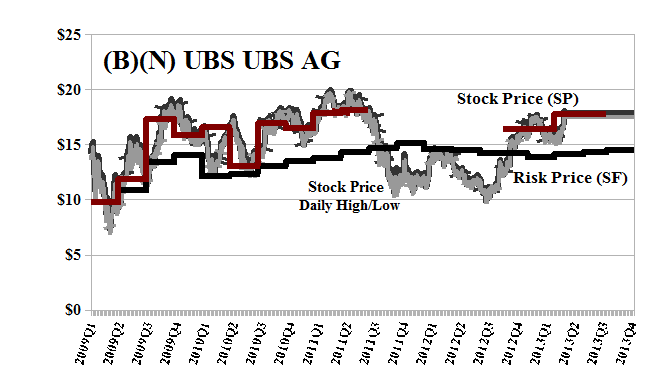

(B)(N) UBS Union Bank of Switzerland AG

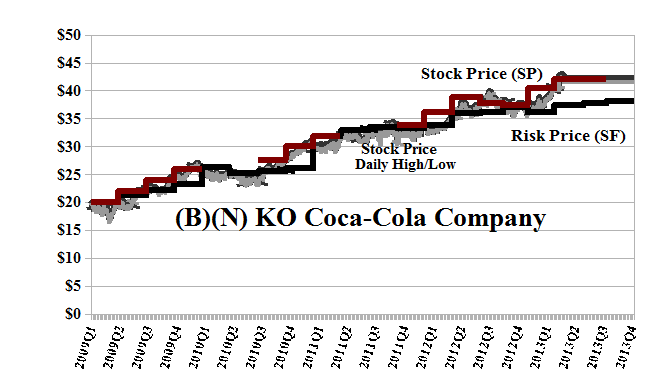

Drama. The Union Bank of Switzerland, with headquarters in the Bahnhofstrasse of Zurich, Switzerland, continuously since at least 1862, is one the largest and most fabled banks of the world, and we need to tell them how to make their stock price perform more like that of the Coca-Cola Company, another popular world-brand of the well-heeled for more than 100 hundred years, out of Atlanta, Georgia, and not so much like a gold mine in Zimbabwe (Reuters, May 2, 2013, UBS faces calls for break-up at investor meeting). Please Exhibit 1 and 2 below.

The bank has a shareholders equity of $50 billion and is responsible for, or “liable” for, customer deposits of twenty-six times as much ($1.3 trillion = 26 × $50 billion), but a stock price of $18 today and a market value of only $69 billion, which is just 40% above its net worth.

In contrast, the Coca-Cola Company has a shareholders equity of $32 billion and total liabilities of $56 billion, which is not even twice its shareholders equity ($56 billion = 1.7 × $32 billion), and only 1/3rd of its market value of $187 billion, which is more than 500% of its net worth. Of course, we don’t expect the bank to match its liabilities dollar for dollar – there’s depositor insurance for that and the Swiss government has helped out at least three times since 2008 – but to be good for only 4¢ on the $1 is an enormous responsibility for a bank that does not know what risk is, and surely no less a responsibility than that of every bottle of Coca-Cola – which is also a standard product like money – to its customers, and the FDA (U.S. Food and Drug Administration) which could and would shut them down with even one bad batch that made it into the market (please see The Independent UK, October 12, 2012, Swiss heads roll: the demise of UBS after a staggering 10,000 layoffs and the Financial Times UK, September 19, 2011, Scandal at UBS points to mix of failures).

So we recognize that the bank has cleaned house quite a bit – axing 10,000 employees out of 70,000 is much more than a decimation, and we haven’t seen one of those since treason in the ranks of ancient Rome – but the Risk Culture has not changed at all. It’s still “no risk – no reward” and because they’ve tightened up on the control of the risk factors, they’ve also tightened up on the reward possibilities, absent accidents or surprises, over which they have no control, by definition.

The bank needs to understand – to embrace – that an investment is just and only the purchase of risk, and like any other purchase that we might make, we ought to know the price of it; that is, we ought to know the price of risk, just as we ought to know the price of anything else that we might buy. Moreover – and this is the second point – the risk is not that we might not get excess returns, that is, returns above the rate of inflation, but that we might not get our money back and so obtain a real return that is less than zero and a pox upon us. And that’s what they need to guard against; volatility is not important to returns or to anyone but day-traders and market makers; the investor’s money needs to absolutely safe – 100% capital safety – guaranteed and to obtain a hopeful but not necessarily guaranteed rate of return above the rate of inflation; embrace the concept that we do not invest our money in order to have a better chance of losing it.

We also note that with a market value of only $69 billion and assets under management (AUM) of $1.3 trillion, the shareholders are paying only $1 for every $20 under management, which is grossly below the market rate of as much as $1 for $10 (please see our recent Posts, New Found Money and (B)(N) GS Gluskin Sheff & Associates Incorporated, April 2013) and that the bank could be trading at $36 instead of the current $18, and more comparable to $36 to $60 of years gone by in 2007 and early 2008, had the bank only had an appropriate risk technology that provably embraced the concept that we do not invest our money in order to have a better chance of losing it (sic).

Finally, we note that the bank is paying a dividend of $600 million per year to the shareholders for a current yield of 0.89% which looks a lot like the yield on government paper, in comparison to the Coca-Cola Company which currently pays a dividend of $5 billion (eight times as much) for a current yield of 2.67% which is at least comparable to the rate of inflation, notwithstanding that the stock price of the Coca-Cola Company has increased from $20 in 2009 to the current $40 (+100%) in contrast to the stock price of the bank, charitably, 0%, several times (please see Exhibit 1 and 2 below).

Exhibit 1: (B)(N) UBS UBS AG – Risk Price Chart

(B)(N) UBS UBS AG – May 2013

UBS AG is a global financial services provider and a major bank in Switzerland. It provides wealth management, investment banking, and asset management services.

(Please Click on the Chart to make it larger if required.)

The Wealth Management division provides financial services to high net worth individuals worldwide and offers investment management, estate planning, and corporate finance advice, as well as specific wealth management products and services. The Investment Bank division offers products and services in equities, fixed income, foreign exchange, and commodities to corporate and institutional clients, sovereign and government bodies, financial intermediaries, alternative asset managers, and its wealth management clients, and engages in sales, trading, and market-making activities across a range of securities and provides advisory and analytics services in capital markets. UBS AGs Global Asset Management division offers investment solutions to various asset classes comprising equities, fixed income, currencies, hedge funds, real estate, infrastructure, and private equity, and also provides professional services, including fund set-up, accounting, and reporting for traditional investment funds and alternative funds. The company’s Retail & Corporate Office offers financial products and services to retail, corporate, and institutional clients. UBS AG also provides treasury services.

Exhibit 2: (B)(N) KO Coca-Cola Company – Risk Price Chart

(B)(N) KO Coca-Cola Company – May 2013

Coca-Cola Co is a manufacturer, distributor and marketer of non-alcoholic beverage concentrates and syrups.

(Please Click on the Chart to make it larger if required.)

We only buy and hold the stock if the stock price appears to be above the price of risk (Red Line Stock Price (SP) above the Black Line Risk Price (SF)) and for no other reason.

Please see our recent Post, Bystanders & Collateral Damage, April 2013, for more information on the price of risk, and for a recent summary of what we’re buying and holding now, The Wall Street Put, April 2013.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.